Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

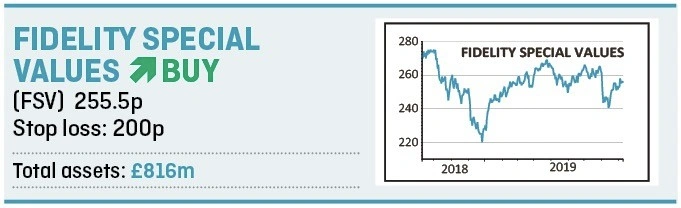

magazineBagging bargains with Fidelity Special Values

Cautious investors concerned about future stock market corrections might consider seeking shelter in a portfolio of domestic stocks that are already dirt cheap and primed for recovery.

Fidelity Special Values (FSV) pursues such an approach. Managed by Alex Wright, this fund should provide a margin of safety, as it aims to buy shares for less than their intrinsic worth, and also offers a compelling play on the re-rating potential of a deeply unloved UK market.

WHAT DOES FIDELITY SPECIAL VALUES DO?

Fidelity Special Values is an all-cap investment trust with a value-contrarian philosophy managed by the well-followed Wright. It seeks to achieve long term capital growth through investment in special situations, i.e. UK companies that Wright believes are undervalued or where the potential has not been recognised by the market.

He invests in unloved companies in out of favour sectors, but with the caveat that he wants to see a balance sheet that can withstand economic weakness and a valuation providing a margin of safety, which are held until their potential value is recognised by the wider market. A book of between 80 and 120 stocks provides both diversification and liquidity.

WHAT’S IN THE PORTFOLIO

Wright’s day job entails researching companies that offer some degree of downside protection but also ‘potential for a positive change to show them in a new light’. By investing when all the bad news is ‘in the price’, and no good news is expected, he looks to stack the odds in his favour.

With Wright willing to go against the grain, Fidelity Special Values offers exposure to two heavily-shorted stocks, defence equipment company Ultra Electronics (ULE) and educational publisher Pearson (PSON), firms with have had major issues in the past but, Wright believes, have more positive futures ahead of them.

Pearson’s profit warnings between 2015 and 2017 left many believing the company is in a prolonged structural downturn, yet Wright argues they are missing the enormous investment it has been making into digital education services and the positive effect this could have on the company.

Short-sellers have argued Ultra Electronics pursued aggressive accounting policies under its previous CEO, thus exaggerating profitability, and that the company can’t grow organically.

However, Wright likes its high-quality portfolio of defence assets and the shares have rallied since first half results which suggested these accounting policies can be unwound, key markets are improving and organic growth is returning.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.