Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat happens next with China’s currency devaluation?

WHAT HAS HAPPENED?

The state-directed Chinese yuan currency moved through the seven per dollar threshold on 5 August for the first time since the global financial crisis in 2008. This provoked the US Treasury department into accusing Beijing of currency manipulation as the trade war continues to rage between the two countries.

WHY DOES IT MATTER?

A weaker currency typically makes a country’s exports more attractive and the Trump administration has consistently complained that a cheaper yuan, or renminbi as it is also known, will give China an unfair advantage on trade.

Markets reacted badly to the development and although the situation has calmed somewhat, the People’s Bank of China (PBOC) set its official reference point for yuan weaker than seven for the third consecutive session on 12 August.

Meanwhile in the background bubbling tensions in Hong Kong are raising fears of a crackdown from mainland China on a global centre of commerce.

A devalued currency could also exacerbate the debt situation in China as it would make it more expensive for the country to pay back its foreign-denominated borrowings.

WHAT HAPPENED IN 2015?

The previous period of pronounced devaluation for the yuan came almost exactly four years ago. In 2015 this episode contributed to a major sell-off in global equity markets. In the preceding decade the yuan had appreciated by a third against the dollar before the PBOC surprised with three consecutive devaluations.

HOW MIGHT THE US RESPOND?

Trump has said the US could respond by devaluing its own currency but arguably this is not a credible threat, particularly as the dollar is often seen as a safe haven asset and therefore a beneficiary of market turmoil.

In addition, while the US Federal Reserve looks likely to cut interest rates further, typically something which would drive down a currency, this has already been factored in by the markets.

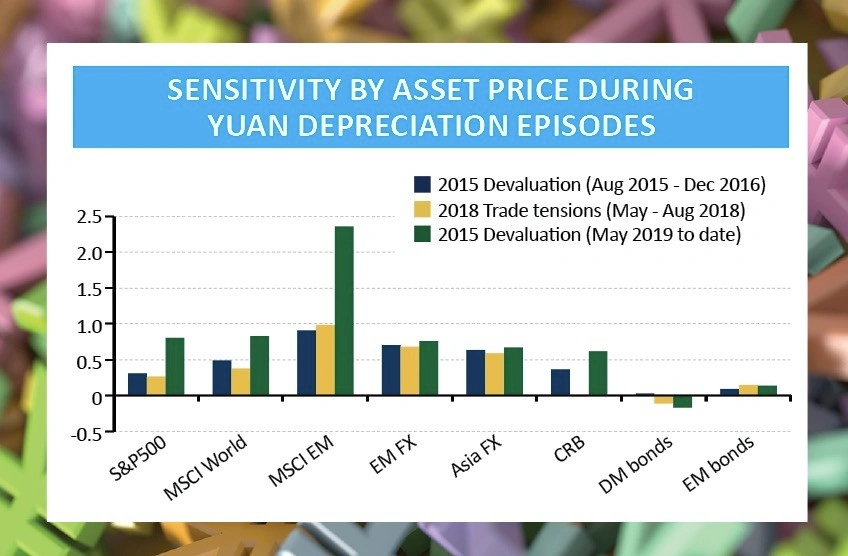

HOW DOES IT IMPACT GLOBAL MARKETS?

Any further devaluation of the yuan is likely to be bad news for most asset classes. As BoA Merrill Lynch forex strategist Adarsh Sinha comments: ‘Only developed market bonds depict negative sensitivity to [the yuan] - in other words the only asset class that benefits during [yuan] depreciation episodes.’

Gold prices may benefit from global attempts to debase currencies as the precious metal’s status as a traditional store of value becomes more highly prized. Gold recently hit a six-year high.

One risk is that attempts to manipulate currencies lower through lower interest rates will leave central banks with less room for manoeuvre if they need to act in the face of a more pronounced economic slowdown.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.