Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe DNA of the FTSE 350

If you are new to stock market investing you may still have heard of the FTSE 100. It frequently appears on TV news bulletins and in the papers, its relative direction up or down giving viewers/readers a steer as to how the UK economy is going and how optimistic, or not, investors feel about the nation’s prospects.

By contrast, the FTSE 350 the has a very low profile and seldom gets a mention at all.

WHAT IS THE FTSE 350?

You may already know that the FTSE 100 is a representation of the UK’s 100 largest companies by market value. It is an index designed to help the financial services industry create funds and other investment tools that track the index, and as a performance benchmark against which various investments can be measured.

The FTSE 350 is also an index benchmark but as well as including the UK’s 100 largest companies, it also includes the stock markets next 250 biggest firms, otherwise called the FTSE 250 index.

So the FTSE 350 is an amalgam of the tier one FTSE 100, and the second tier FTSE 250.

Companies in the FTSE 350 that you would certainly have heard of include BT (BT.A), Barclays (BARC), Royal Dutch Shell (RDSB) and Vodafone (VOD).

There’s also sports cars firm Aston Martin Lagonda (AML), Johnnie Walker whiskey maker Diageo (DGE), housebuilder Bellway (BWY) and Cineworld (CINE).

But there are loads more that are little known outside of industry and investment circles, many of them world class businesses.

This is the first of a multi-part series on the FTSE 350. next week we take a closer look at the consumer facing names on the index.

STRINGENT RULES

On the UK stock market there is a third tier below this, the FTSE Small Cap index. It is all other companies that pass the London Stock Exchange’s (LSE) stringent listing requirements, and is the third and final piece forming the FTSE All-Share index.

These rules include having a full listing on the LSE with sterling or euro denominated shares that can be traded on the exchange’s Electronic Trading Service. They must also meet strict tests on nationality, free float (stock owned by independent institutions or private investors), plus liquidity, which is a measure of how freely stock can change hands.

Unlike the FTSE 100 and 250, the FTSE Small Cap index does not have a fixed number of constituents, the number of small cap companies is fluid as companies merge or are taken over, delist or simply go to the wall, there are also initial public offerings (IPOs), which are new entrants to the market.

The FTSE Small Cap index counts 283 companies as members, according to recent FTSE Russell data (31 July).

MOVEMENT BETWEEN THE INDICIES

Qualification for entry into the FTSE 100, 250 and Small Cap depends on the value of a company, or its market capitalisation. The constituents are reviewed each quarter, on the Wednesday after the first Friday of the month in March, June, September and December, with a maximum of 10 companies potentially up for relegation from each list or promoted to it.

Companies qualify for the FTSE 100 if they rank among the top 90 UK-listed firms by market cap and conversely drop down to the FTSE 250 if they fall to position 111 or below on the night before the review takes place. Any companies that drop out of the FTSE 250 fall into the Small Cap index.

The most recent shake up in June 2019 saw seven companies promoted to the FTSE 350, another seven drop out and into the Small Cap index. Those moving up in the world included local utility bills payment service PayPoint (PAY), pubs group Marston’s (MARS) and Belfast-based digital services supplier and advisor Kainos (KNOS).

Falling out were troubled building contractor Kier (KIE), retirement services supplier Saga (SAGA), Southend airport-owner Stobart (STOB) plus four others.

BOTTOM LINE ON BENCHMARKING

As we have said previously, indicies like the FTSE 100 and FTSE 350 help provide a yardstick for investors to measure the relative performance of stocks and funds against.

For example, you might hear a fund say it has beaten the index during the past year. To understand this, if a fund delivers a 10% annual return, and the FTSE 100 (the benchmark in this example) increases 8% over the same time frame, the fund can say it has beaten the index by 25%.

It provides a guide to how well, or poorly, an investment has done over the fixed period. For example, mobile network giant Vodafone (VOD) is widely owned by investors because of its hefty dividends.

But its shares have done miserably this year, not least because it cut the payout back to 2009 levels. Vodafone shares have declined by about 3% in 2019 whereas the FTSE 100, of which Vodafone is a member, has risen by about 8%.

So in effect, Vodafone stock has underperformed the FTSE 100 by about 11% year to date.

IS FTSE 350 AN INDEX FLOP?

If we consider that providing a benchmark is one of the two core purposes of an index then it could be argued that the FTSE 350 is not terribly successful. Most UK-aimed funds will benchmark either against the FTSE 100 or, more often, versus the FTSE All-Share, with a smallish number of specialist mid-cap funds using the FTSE 250.

Very few bother to benchmark against the FTSE 350 and the reason is largely because of the fact that all FTSE indexes, or indices as they are sometimes called, are weighted by market capitalisation. This means that larger companies make more of a difference to each index than smaller companies in terms of performance.

For example, banking group HSBC (HSBA) is currently the largest company on the UK stock market with a market value of around £132.9bn, compared to the £2,267bn value of the FTSE 350 in total (based on FTSE Russell’s 31 July data). That gives it a FTSE 350 weighting of 5.86%.

By contrast, the smallest FTSE 350 firm, crowd funding business Funding Circle (FCH) has a market value of £368m, piddling in comparison to the wider FTSE 350, which makes its share price moves virtually irrelevant at an index level.

That weighting issue means that the entire Small Cap index is so small by comparison to the FTSE 350 that there is virtually nothing between the performance of the FTSE 350 and the FTSE All-Share. Hence funds benchmark against the FTSE All-Share.

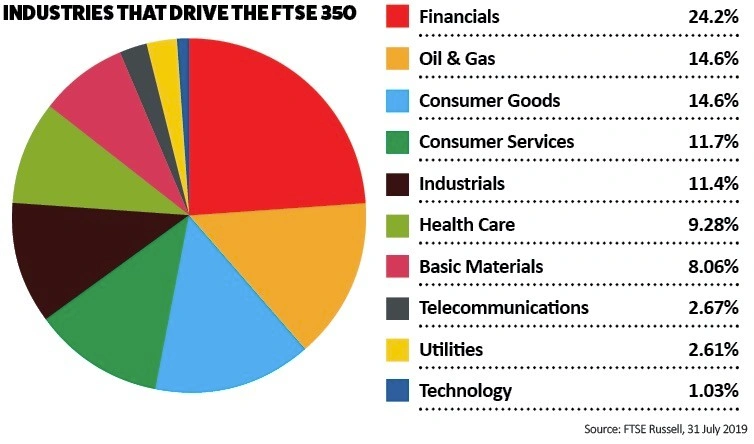

SECTORS WITH THE HEFTIEST PUNCH

While many of us tend to think of Britain as a larger service-based economy with a huge financial services industry, the UK stock market is no slouch in manufacturing, construction, engineering and, particularly, oil and mining.

FTSE indexes use Industrial Classification Benchmark (ICB) standards to breakdown industries into investment sectors, which is arguably more complex than it needs to be, from a private investor point of view.

The ICB uses a system of 10 industries partitioned into 19 super-sectors, which are further divided into 41 sectors, which then contain 114 subsectors.

Perhaps the most useful way to think of it is to take a big picture view, natural resources, business production, consumer products and services, with financial services probably straightforward enough.

That might suit retail investor but it would probably not be detailed enough for City institutions, but we can simplify the message.

FINANCIALS – 132 companies (24.2% FTSE 350 weighting)

Think the high street banks that we all know – Lloyds (LLOY), Barclays (BARC) and HSBC, big insurance companies like Aviva (AV.) and Legal & General (LGEN) personal loans and fund-raising firms like Amigo Loans (AMGO) and Funding Circle (FCH).

OIL & GAS – 10 (14.6%)

Says what it does on the tin, includes BP (BP.) and Shell plus eight other smaller companies.

CONSUMER GOODS – 31 (14.6%)

Unilever (ULVR), which makes much of the stuff on supermarket shelves, such as Domestos bleach, Persil washing power and Wall’s ice cream, finds its home here as do drinks manufacturers. But you might not realise that car makers (and parts suppliers), housebuilders and tobacco stocks are also included.

CONSUMER SERVICES – 61 (11.7%)

Includes big supermarkets like Tesco (TSCO) and Sainsbury (SBRY), while most high street and online retailers sit in this sector. Travel firms such as TUI (TUI) feature here, as do leisure enterprise, like Cineworld. Also includes media businesses such as broadcaster ITV (ITV) and advertising agency WPP (WPP).

INDUSTRIALS – 62 (11.4%)

Think aero-engine maker Rolls-Royce (RR.) or engineering firms like Renishaw (RSW) and steam and heating systems designer Spirax-Sarco (SPX). This sector also includes bus and train operators plus business services suppliers.

HEALTHCARE – 11 (9.3%)

Big pharmaceutical companies like AstraZeneca (AZN) and GlaxoSmithKline (GSK) dominate here. But there are also a handful of healthcare equipment manufacturers, such as Smith & Nephew (SN.), which makes prosthetic limbs and joints, plus private hospital operators like NMC Health (NMC).

BASIC MATERIALS – 20 (8.1%)

Natural resources that are not oil related, this is mainly made up of multi-billion pound gold, iron, copper and other material miners like Anglo American (AAL), BHP (BHP) and Rio Tinto (RIO). Also include paper-based packaging firms like DS Smith (SMDS), which makes those corrugated cardboard coverings that Amazon deliveries tend to arrive in.

TELECOMMUNICATIONS – 5 (2.7%)

Pretty self-explanatory, suppliers of services around phones, the internet and streaming TV sit here. Vodafone and BT are the real heavyweights, with TalkTalk (TALK) and Utility Warehouse operator Telecom Plus (TEP) other constituents.

UTILITIES – 8 (2.6%)

Utility energy suppliers like British Gas-owner Centrica or SSE (SSE) are joined by a handful of water network suppliers, like United Utilities (UU.), the UK’s largest by market value.

TECHNOLOGY – 11 (1.0%)

This is really software companies led by accounting and payroll platform provider Sage (SGE). IT infrastructure developer Micro Focus (MCRO) and engineering software provider AVEVA (AVV) are also prominent.

FTSE 350 ETF options

There are exchange-traded funds (ETFs) which track both the FTSE 100 and FTSE 250 benchmarks, so buying both would be one way of getting exposure to the FTSE 350 as a whole.

Most products are further distilled into a distribution version and an accumulation version.

Given that the FTSE 100 and FTSE 250 are not total return indices – that is, all dividends paid by index members are paid out in cash (distributed) rather than re-invested in the index (accumulated) – the truer comparison with the index is the distribution version.

There are 11 UCITS ETFs tracking the FSTE 100 which are ISA-friendly but for reasons of liquidity we are only interested in the two largest: the BlackRock’s iShares Core FTSE 100 (ISF) and the Vanguard FTSE 100 (VUKE).

Both are ‘full replication’ funds therefore they own the same stocks as the index and in the same proportions, and their performance over one year, three years and five years is virtually identical to that of the index and each other.

Their ongoing charge figures (OCF), which cover administration, audit, depositary, legal, registration and regulatory costs, are also virtually identical. Lastly, they both yield 4.44%, the same as the index as at the end of June.

There are even fewer FTSE 250 ETFs so again for simplicity and liquidity reasons we have narrowed it down to the two largest distribution versions, one by iShares and one by Vanguard.

Both invest in all 250 index constituents in the same proportion as the index therefore their performance and yield are virtually identical to the index. The only distinguishing feature between them is the lower charges at Vanguard.

How FTSE indexes emerged

The FTSE All-Share Index was originally called the FT Actuaries All-Share Index at its inception in 1962. The index was first enhanced in 1984 with the creation of the FTSE 100, the best-known and most closely followed of UK stock market indexes. More refinement followed in 1992 when the FTSE 250 was set-up to give investors an increasing number of options.

Funds and the FTSE 350

FTSE 100 and FTSE 250 ‘tracker’ funds and ETFs are a good place to start if you’re new to investing and looking to build a low-cost portfolio as a first step. However trackers can never beat the market as they are designed to track it minus a tiny amount for fees.

Another way to add risk is to pick a fund with a high ‘active share’ which means that it owns relatively few big index stocks, giving it the potential to outperform. Active share is shown as a percentage between 0 and 100: the less the fund looks like the index, the higher the percentage.

Most funds explain on their factsheet that due to the different composition of the fund versus the market, the fund’s performance is likely to be very different to the market. If you’re comfortable for your fund to zig when the market zags, then all well and good.

However there are no guarantees that funds with a high active share will outperform. Performance is largely a factor of the quality of investment decisions a fund manager makes not just how far they deviate from the index.

As Ryan Hughes, head of active portfolios at AJ Bell, points out, Woodford Equity Income Fund (BLRZQ62) had a very high active share at 98% but poor stock selection and lack of liquidity led to the fund under-performing and subsequently being suspended.

In contrast, the JPMorgan UK Equity Plus Fund (BW4Q9B1) only has an active share of 45% but it has comfortably beaten the FTSE All-Share over the last three years.

Statistically, an active share above 80% is considered as a good measure of ‘activeness’ although this depends on the structure of the underlying index. For example the average in the UK All Companies sector is 67%.

When looking at active share in the UK, a high active share nearly always points to a fund having more invested in medium and smaller companies which brings other risks advises Hughes.

His top picks, in descending order of active share, are:

Montanaro UK Income (BYSRYZ3): a high-conviction portfolio typically made up of 40 to 50 stocks, with an active share of 97%, invested mostly in small and mid-cap companies that offer an attractive dividend yield or potential for dividend growth.

Liontrust Special Situations (B57H4F1): a ‘sparkling performer’ according to Hughes, with an active share of 73% and a more equally-weighted approach than other funds (its top ten holdings are all 4% each of the fund).

Investec UK Alpha (B7LM4J0): has the lowest active share at 53% but over five years has beaten both the FTSE All-Share index and the sector by a comfortable margin.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.