Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTate & Lyle has got the right ingredients for growth

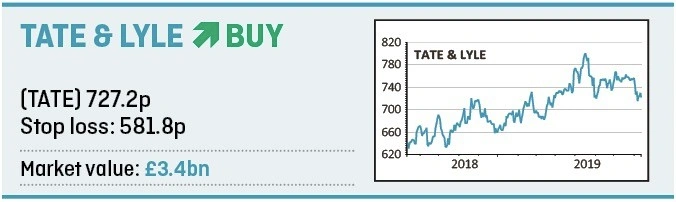

Investors should buy food producer Tate & Lyle (TATE) at 727.2p. We believe the market is underestimating the scope of its long-term margin potential, which could prove the catalyst for earnings upgrades.

WHAT DOES TATE & LYLE DO?

Tate & Lyle is a global provider of corn-based sweeteners and starch ingredients as well as sucralose zero-calorie sweetener. Following a testing few years of transformation towards a higher margin and more stable speciality ingredients supplier, Tate & Lyle is in a healthier position operationally.

Admittedly, the current geopolitical trade environment is unhelpful for US exporters into China, yet with the bulk of revenue generated in US dollars and the company reporting in sterling, the plunge in the pound should boost earnings as this dollar denominated revenue carries greater weight.

TASTY POTENTIAL

Encouragingly, full year results (23 May) came in ahead of consensus with pre-tax profit and earnings per share up 4% to £309m and 52p respectively, underpinned by a solid performance in the speciality Food & Beverage Solutions division.

Growth in North America was driven by share gains at larger food and beverage customers, further expansion into new channels like food service and own label and new business wins in targeted higher-growth sub-categories like health and nutrition.

Ingredients companies like Tate & Lyle and closest peer Ingredion are well placed to provide plant-based ingredients and solutions to customers, thereby profiting from growing consumer demand for plant-based proteins.

Elsewhere, Tate & Lyle demonstrated renewed momentum in the Sucralose division, despite moderately weaker pricing, although Primary Products volumes are under increasing pressure from lower sweetener volumes in a declining North American fizzy drinks market.

Shares sees potential for a re-rating as Food & Beverage Solutions profits grow. We also note that CEO Nick Hampton has done a good job in increasing free cash flow generation and lowering net debt. Tate & Lyle recently announced (5 Aug) the issuance of new debt in a refinancing move set to lower its interest bill by circa £7m per annum and provide extra dry powder for acquisitions.

Liberum Capital spies strong share price upside if Tate & Lyle can approach the margin levels of rival Ingredion in speciality ingredients.

And for the year to March 2020, Berenberg forecasts growth in earnings per share from 52p to 53p and a dividend hike from 29.4p to 30.3p, ahead of estimated earnings of 54p and a 31p payout in fiscal 2021.

Based on this year’s estimates, a prospective PE of 13.7 times looks undemanding given Tate & Lyle’s global growth opportunity and the shares also offer an attractive yield of 4.2%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.