Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

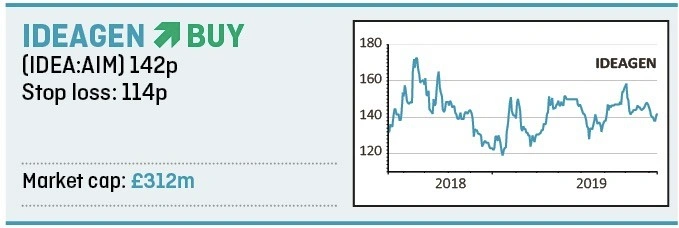

magazineIdeagen is a structural growth story with plenty of opportunity

If the 10-year run of global economic expansion really is winding down then it makes sense for investors to look for structural growth drivers and companies capable of pulling those levers even in a slowing global economy.

We believe that Ideagen (IDEA:AIM) is just the sort of stable growth company able to pep-up high single-digit to low double-digit organic growth with smart and sensibly priced acquisitions; it’s been doing just that for several years.

Nottinghamshire-based Ideagen provides a host of governance, risk and compliance information management software tools to what it calls ‘high consequence industries.’

The net of regulation red tape and compliance accountability is getting ever tighter around industries and organisations across the world and system and process failures can costs clients millions of dollars in fines, and potentially put lives at risk.

Clients span aviation, healthcare, defence and energy, banking/finance and complex manufacturing.

That’s an increasingly compelling sale once an organisation begins to grasp the significant financial and reputational damage potential of not having adequate systems in place. Blue-chip customers include BAE Systems (BA.), Emirates Airlines, Royal Dutch Shell (RDSB), the European Central Bank plus more than 150 hospitals in the UK and US, while Transport for London, GlaxoSmithKline (GSK) and Meggitt (MGGT) are new banner names.

OPERATING IN A FRAGMENTED MARKET

This is a $7bn a year-plus market yet it remains highly fragmented. Ideagen, which has been around since 1993, is changing that by acting as industry consolidator as well as driving consistent organic growth, currently running at about 8%.

The ongoing plan is to double in size every three years and it is now targeting its next growth push to a £100m revenues run-rate by full year 2022. Most recent full year results showed headline revenue of £46.7m and adjusted earnings before interest, tax, depreciation and amortisation (EBITDA) of £14.3m for the year to 30 April 2019 (up about 30% respectively).

Two-thirds of that business comes from recurring contracts so should be a reliable guide on which to base future growth prospects.

The UK and Europe remain important markets but Ideagen has been expanding in the US successfully and rapidly in recent years. It is now eying considerable new opportunities in the Far East, where it has already set-up offices in Kuala Lumpar and in China.

It is worth noting that profits are heavily adjusted for amortisation and depreciation, and that may not sit well with all investors. But Shares has found the leadership team to be sensible and largely conservative.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.