Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineGold shines as US stocks stumble

America’s headline S&P 500 stock index continues to swing around as bulls and bears grapple for supremacy – and while they are slugging it out gold is quietly doing the business for investors.

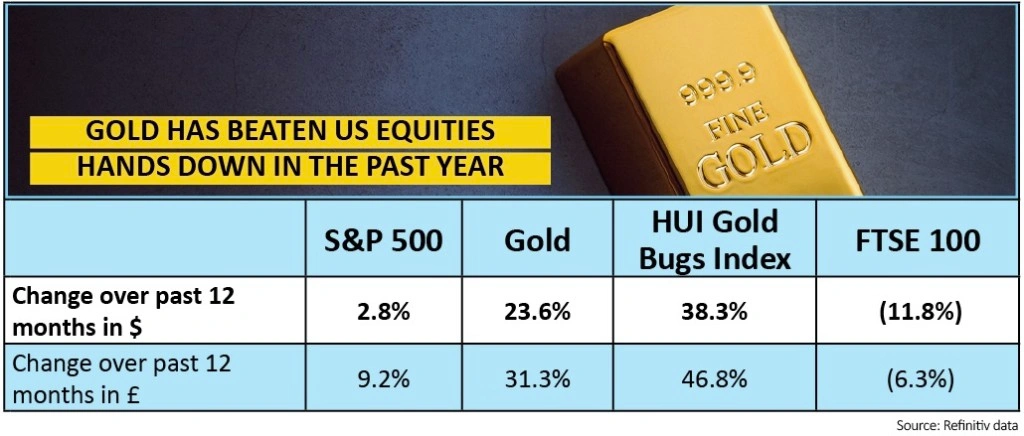

The S&P 500 is up by barely 2% over the past year, while gold is up by a nearly a quarter and a leading index of 15 gold miners is showing gains of nearly 40%.

Those figures are in dollars, so the capital gains for UK-based investors who will be looking at their returns in sterling are even better, thanks to the weakness of the pound. (See table below).

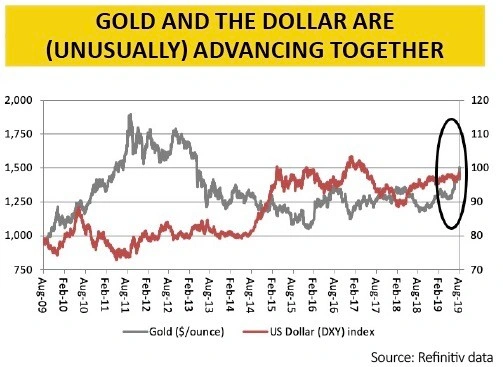

Gold’s latest gains are also particularly notable, because they are coming when the dollar is gaining too. The trade-weighted DXY (or ‘Dixie’) dollar index is trading near 98, despite a US Federal Reserve interest rate cut and the attempts of an irate president to talk (or tweet) down the buck.

Normally a rising dollar signals weakness in gold, as it makes the metal more expensive to buy. But they are gaining in tandem, which suggests that investors are nervous and may be looking for potential bolt-holes in preparation for more difficult times.

Tug of love

The S&P 500 may be trading near its all-time highs, set just above 3,000 mark in late July, but it is making heavy weather of forging decisive gains, as the benchmark is no higher than it was in mid-January 2018.

This due to a tug-of-war between supporters and sceptics of US stocks. Buyers believe that the US Federal Reserve’s move to cut interest rates will stoke further economic and corporate earnings growth. Sellers are countering that a downturn is coming, irrespective of Fed policy, with the result that American equities will be left looking expensive and overextended.

US equities are thus torn between these two schools of thought, especially as a 10-year upswing means the consensus view is that American stocks are still good place to be, thanks to the superior economic backdrop in the US, faith in corporate earnings prospects and the Fed’s switch from raising to cutting interest rates.

But the better price momentum is coming from gold, which was out in the cold at the start of the year after another dismal showing in 2018. The precious metal has finally cracked through the $1,350 to $1,360 an ounce range that had capped several advances over the past five years and smartly progressed to a six-year high above $1,500.

Loss of nerve

Investors’ enthusiasm for gold seems to be gathering for three reasons. Fresh interest rate cuts around the world mean there is less opportunity cost in owning the metal, which itself generates no yield, as returns on cash (and bonds) go lower once more

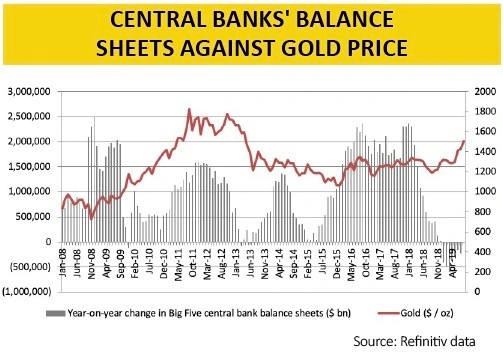

This year’s policy U-turn by central banks suggests that they are not quite as in control of the global economic situation as investors would like to think and fears of a downturn or recession mean investors are seeking out haven assets

With interest rates already so low, central banks may not have that much monetary ammunition left, meaning they may return to quantitative easing and more money creation, in the event of a recession.

Such policies could tempt investors to look for hard assets, such as precious metals, to protect their wealth, as happened during the early rounds of easing between 2009 and 2011.

As a result of the metal’s resurgence, gold miners are also enjoying a return to favour. The HUI Gold Bugs (Basket of Unhedged Gold Stocks) index contains 15 gold miners and rising gold prices are great news for them, especially if they are increasing production and managing their costs carefully.

The world’s biggest gold miner, by market capitalisation, is Colorado-headquartered Newmont Goldcorp, with its $32bn price tag (a fraction above Toronto-based Barrick Gold). Newmont Goldcorp’s all-in sustaining cost (AISC) figure, for example, was $1,016 an ounce in Q2 2019, so every $1 on the gold price above that mark will drop quickly through to the bottom line.

If gold keeps rising then the miners’ gearing into those price gains mean their profits should rise faster still, assuming costs are well managed.

Equally, the opposite also holds true – were gold prices to back, as investors regained confidence in central banks’ policies and the global economic outlook, then that could again pressure the miners’ profits and cash flows, to the detriment of their share prices.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.