Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat we can learn from oil’s latest sticky patch

Stock markets are generally rising high, especially in the US, but commodity prices are doing nothing of the sort with the occasional, supply-driven exception such as nickel or iron ore. Despite a robust spring rally, the Bloomberg Commodity index is down by around 5% from where it stood a year ago and Brent crude oil is 14% lower.

This could suggest that all may not be entirely well with the global economy, as you would expect to see raw material prices rise if activity and demand levels were high. That said, oil demand

is expected to hit a new all-time high in 2019, at a fraction under 100m barrels a day by the end of the year.

Oil’s latest sticky patch may be more related to supply than demand. If so, investors need not be too alarmed by weakness in the price of crude.

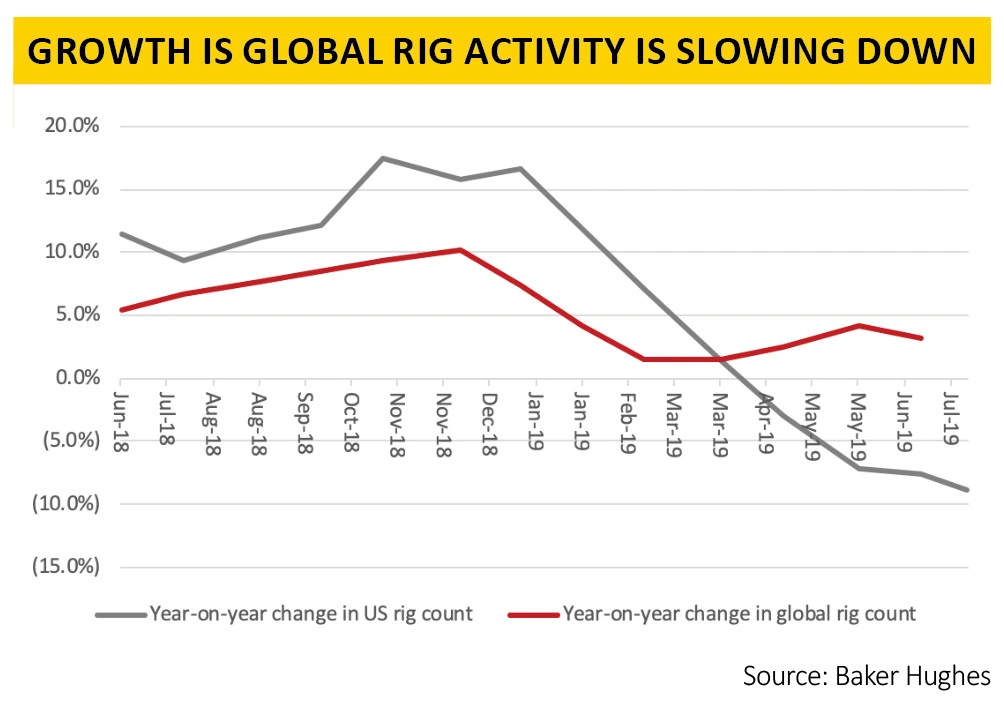

Rigs rolling over

Supply can be quickly gauged. On the face of it, oil’s latest wobble is curtailing fresh exploration work, as you would hope and expect. Data from Baker Hughes shows that the active US rig count is 9% lower than it was a year ago and the international count is 3% higher, as oil firms keep a close eye on their expenses and cash flow.

Further good news can be found in the form of falling American oil inventories. US stockpiles of crude are now 9% lower than they were a year ago.

This is despite a sustained increase in American oil and gas output from its onshore shale fields. Oil production is up by some 950,000 barrels a day, or 13%, over the past year.

This could be a key factor in capping the oil price, since this surge in output goes a long way to compensating for the 1.2m barrel a day production cut sanctioned by OPEC in Vienna last December and then again in June.

Yet growth in shale supply is relatively modest as the annual rate of increase was running at 1.9m barrels year-on-year in August 2018. Any further slowdown in shale growth could actually help oil – at least if OPEC and Russia maintain their current output discipline. Yet even with this deceleration in growth crude remains weak.

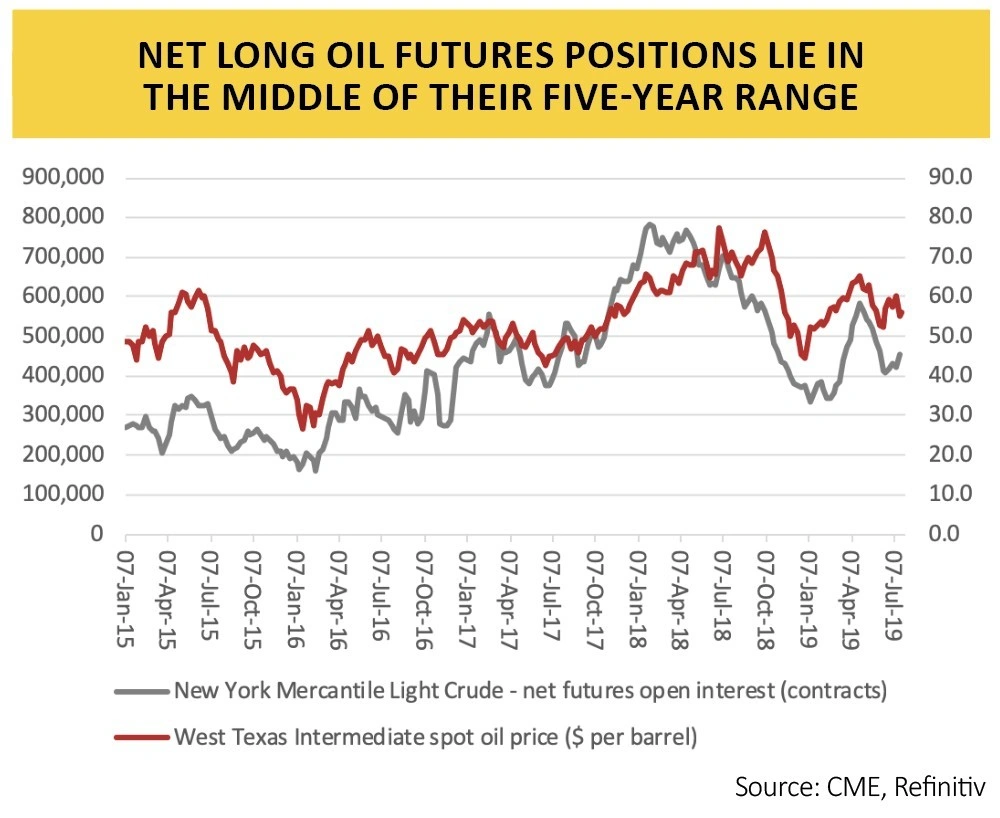

One further factor which may be at work is how financial speculators are positioned via the futures market. Each contract is worth 1,000 barrels of oil and the fund flows are huge, easily outstripping actual physical demand.

According to data from the CME, the amount by which the number of speculative ‘long’ (buy) contracts exceeded the number of ‘short’ (sell) contracts peaked at 784,290 in January 2018.

Once the crude price began to roll over, buyers ran for cover and sellers took over. Net long positions shrank to 332,714 contracts in January 2019 and oil hit bottom at the same time. In other words, as in all markets, running with the herd just gets oil traders badly trampled. They need to go against the crowd.

Buyers have begun to gather again, perhaps emboldened by the diplomatic stand-off between Washington and Tehran, a delicate affair in which the UK is now embroiled after the mutual seizure of oil tankers in Gibraltar and then the Straits of Hormuz. Net long positions have crept back to around 450,000 contracts.

Pump up the dividends

That sits in the middle of the range for the last five years, as if to say even the professionals don’t have a strong feel for where oil is going next, so it would take a brave investor to take a strong view at the moment.

The possible bad news is that oil’s weakness reflects soft demand. Annual oil consumption has only fallen twice since 2000 and that was in 2008 and 2009 when the global economy was on its knees.

The better news is that spikes in oil have tended to act as a brake on global economic activity, as per 1975, 1980, 1990, 2000 and 2007, while relatively stable prices have tended to be a good lubricant.

A quiet oil market is generally more helpful to financial markets overall than a noisy one and the best scenario for investors is more of what we have now, although history also suggests that periods of calm never last for too long.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.