Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCut-price stocks: 1/3 off

There’s a reason people queue up outside shops at dawn on 26 December, and it’s not just to get away from annoying relatives. We all love a bargain, picking up quality merchandise when it is on sale and often we only have a short window to play with.

A similar logic can apply to the stock market. Sometimes quality stocks can trade at knockdown prices but typically not for that long. After doing some number crunching and then putting its collective brainpower to work, the Shares team has identified five stocks worth buying now while they are marked down, some by more than a third.

Our quintet of cut-price stocks are soft drinks outfit A.G. Barr (BAG), oil company Cairn Energy (CNE), IT firm Craneware (CRW:AIM), posh mixers maker Fevertree Drinks (FEVR:AIM) and prospective potash producer Sirius Minerals (SXX).

All were trading at a 10% or more discount to their 200-day moving average when we screened the market for opportunities. A moving average is something which helps you see the wider trend in a share price and smooth out the impact of short-term volatility.

WHY HAVE THE SHARES FALLEN?

Share prices can fall for all sorts of reasons. At times of market panic, selling can be both disproportionate and indiscriminate.

We took advantage of this situation when we added electronic equipment manufacturer Halma (HLMA) to our Great Ideas portfolio following widespread selling in October 2018.

We recognised nothing had ultimately changed about what was an extremely good business and recommending buying at £12.62. As we write the shares trade at £20.11, representing a significant gain on our entry price. We would not necessarily expect all of our ideas to generate returns on this scale but double-digit gains in a year are a realistic possibility if sentiment towards our list of names in this article shifts.

Buying stocks at an apparent discount doesn’t always work and we don’t always get it right. The same week we flagged Halma, we also highlighted the potential in ticketing technology firm Accesso (ACSO:AIM) and its shares continued to fall.

Investors need to remain alive to changes to the investment case, whether these are driven by internal developments or external developments.

QUALITY CONTROL IS NEEDED

Simply screening for cut-price stocks doesn’t necessarily mean each one on the list is worth buying. For example, one name appearing on our latest screening exercise is healthcare provider NMC Health (NMC) and there are valid reasons for the decline in its shares.

Founded in 1975, NMC is the largest healthcare provider in the United Arab Emirates and owns and operates over 200 hospitals across more than 15 countries, treating more than 8.5m patients every year.

Its shares are down 44% from their peak in August 2018 and there has been an increase in the ‘short interest’ since late 2018, meaning that hedge funds and other investors are placing bets that the shares will fall further in value.

Data from shorttracker.co.uk show that the percentage of the company’s shares being used for short selling has risen from 0.5% in November 2018 to 4.73% on 20 July this year.

The negative stance seems to be driven by the acquisitive nature of the company’s strategy and suspicions it has grown too fast and that acquisitions are masking poor organic growth. Investment bank Jefferies has also raised concerns around corporate governance, opaque accounting and supply chain finance.

Up until last year investors seemed happy to chase the share price up to £41, which moved further than the fundamentals, thus increasing the valuation of the business. This created a virtuous cycle whereby the company could buy companies trading on lower multiples than itself and announce that the purchase was instantly ‘earnings enhancing’ for shareholders.

As the stocks has fallen more than the fundamentals and the shares have become cheaper, the dynamics of ‘accretive growth’ may be more difficult to achieve.

WHY HAS THE SHARE PRICE BEEN WEAK?

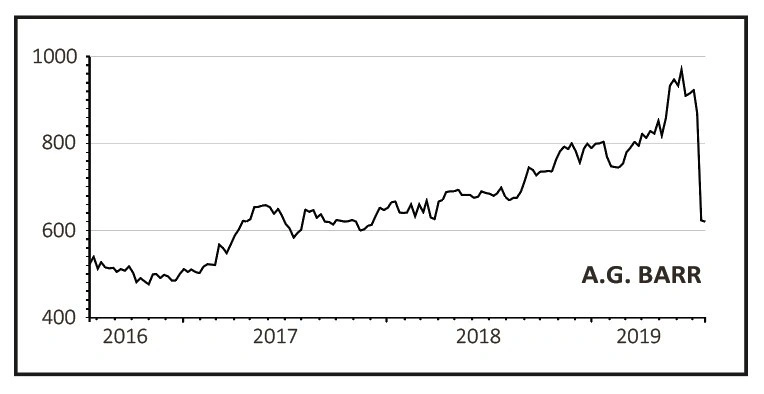

A near-40% share price plunge from June’s 975p peak at soft drinks group A.G. Barr (BAG) presents a buying opportunity for long-term investors looking for a typically dependable, defensive and growing portfolio compounder.

We remain bullish on the long-term earnings potential of Glasgow-headquartered A.G. Barr, whose competitive advantage lies in a portfolio of differentiated soft drinks brands spearheaded by iconic Scottish tipple IRN-BRU, as well as Strathmore, Rubicon and cocktail mixers name Funkin.

A.G. Barr, which recently took a minority stake in non-alcoholic spirits brand STRYYK, also benefits from well-invested manufacturing assets and is highly cash generative, progressive dividend paying and able to fund supportive share buybacks.

Its shares slumped on a punishing profit warning (16 Jul) blamed on a strategy shift from a heavy focus on driving volume last year to prioritising value now. Also at play were disappointing spring and early summer weather, most notably in Scotland and the north of England, as well as challenges around its Rockstar energy and Rubicon juice drinks.

Against a prior year comparative boosted by 2018’s summer heatwave, A.G. Barr expects sales for the 26 weeks to 27 July in the region of £123m, roughly a 10% year-on-year decline. Due to operational gearing, investors can expect full year profits to drop by up to 20%.

WHAT COULD SPARK A RE-RATING?

We believe this profit setback is temporary, mindful of A.G. Barr’s otherwise strong track record on execution and delivery.

Current balmy weather offers a positive catalyst for A.G. Barr, already seeing positive indications of consumer acceptance of higher IRN-BRU prices.

Reassuringly, management has addressed the Rockstar and Rubicon issues with a mixture of new product development and recipe improvements which could boost the second half performance. And remember, AG. Barr has scope for soft drink distribution wins, boasts a strong balance sheet and, given a largely UK sales profile, Brexit looks less of an issue for the FTSE 250 firm than for internationally-focused beverage rivals.

For the year to January 2020, Shore Capital now forecasts adjusted pre-tax profit of £36.1m (2019: £45.2m), with profit rebuilding to £37.2m and £38.4m in 2021 and 2022 respectively.

Following this year’s material downgrade and based on estimated earnings per share of 25.6p and a 17.1p dividend, A.G. Barr remains optically expensive on a prospective price-to-earnings ratio of 24.2-times with a modest 2.8% yield. Yet we believe the shares merit a premium rating and this pullback presents a compelling new entry point for patient investors.

WHY HAS THE SHARE PRICE BEEN WEAK?

WHY HAS THE SHARE PRICE BEEN WEAK?

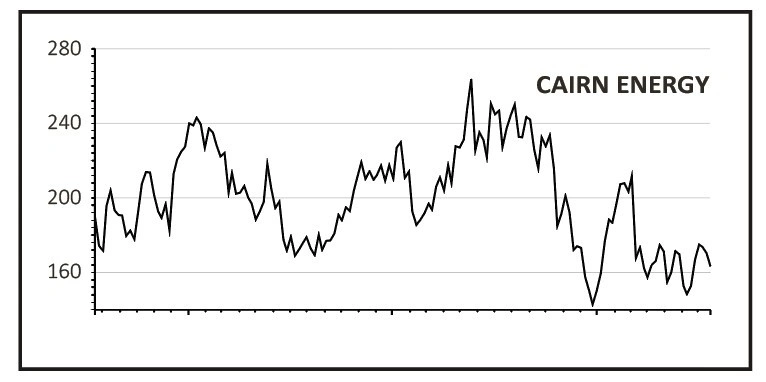

Beyond the oil price volatility which has hit most of the wider sector there have been several company-specific issues weighing on Cairn’s share price. Key has been a hold-up in arbitration proceedings over a long-running Indian tax dispute, where Cairn is seeking $1.4bn in compensation.

A reserves downgrade for its Kraken field in the North Sea earlier this year did little to help sentiment, particularly as write-offs associated with both these setbacks saw the company post a $1.27bn net loss in March. More recently the company announced a disappointing result from its Lynghaug well in Norway.

There has also been a slight delay in the final investment decision on its highly prized SNE development in Senegal. Funding this project might require bringing in an additional partner and selling down some of its current 40% stake.

WHAT COULD SPARK A RE-RATING?

If the first part of 2019 has seen a run of a bad news then there are reasons to feel more positive about the remainder of the year and with the shares trading close to multi-year lows Cairn could enjoy a significant second-half bump.

A price-to-earnings ratio of 16.8-times is higher than you might imagine given the recent bad news, yet this rating reflects the company’s continuing investment in development and exploration assets.

Encouragingly the balance sheet is in rude health, with $66m of cash at the last count and just $85m drawn from a $575m reserves-based lending facility.

In terms of specific catalysts for the share price, a multi-well drilling campaign in Mexico targeting upwards of 500m barrels of oil equivalent could have a significant positive impact on the share price in the event of success.

In order to get the market back on side, Cairn needs to deliver strong operational performance and ultimately production from its North Sea oil fields Catcher and Kraken, and this is likely to be in focus when the company announces its first-half year results on 10 September.

Deliberations on the Indian tax case are not likely to conclude until the end of the year but a successful outcome could be worth as much as 190p per share. However, expecting India to abide by any ruling in the company’s favour might be wishful thinking. At least Cairn is protected from any unfavourable decision which would be ring-fenced to the Indian interests.

WHY HAS THE SHARE PRICE BEEN WEAK?

WHY HAS THE SHARE PRICE BEEN WEAK?

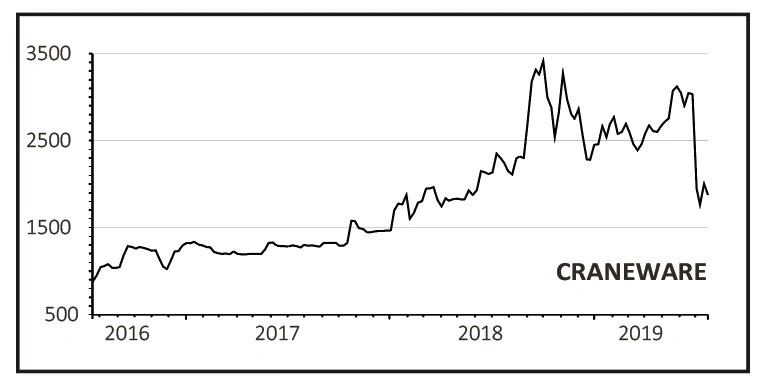

Made-in-Britain Craneware (CRW:AIM) shows that even the best of companies sometimes get caught up in temporary logjams. In June the billing and healthcare analytics software supplier revealed a sharp slowdown in sales, meaning it would miss full year expectations.

Where the market had been anticipating revenue and adjusted EBITDA (earnings before interest, tax, depreciation and amortisation) of $79.5m and $25.6m respectively, the company actually reported $71.1m and $23.8m. Importantly, growth metrics will miss the near-20% expected, posting 6% and 10% instead.

At the core of the issue is Trisus Health Intelligence, Craneware’s recently launched cloud-based analytics platform. Developed over many months, it combines the best of the firm’s core price, cost and compliance features with new financial, operational and clinical data tools.

This new, even more feature-rich platform is more complex and getting its US hospital customers to understand its power to slash costs, drive new revenue streams and speed up administration takes that bit longer.

Management is clear that there is nothing in worries about market share losses or intensifying competition, flagging unchanged renewal levels alongside ‘a significant and growing pipeline’.

WHAT COULD SPARK A RE-RATING?

Demonstrating this situation is temporary will obviously be vital in getting the share price going again, and Craneware certainly has a hard-earned reputation for operational excellence to lean on.

That the company dominates its niche, earns only recurring revenues on average five-year contracts, and enjoys an entrenched competitive position at the top of its industry, makes a quick return to more exciting growth very likely.

Craneware already supplies its software analytics tools to almost a third of the hospitals in the US. It uses automation to highlight operational and financial risks, plus identify new income opportunities to healthcare management. The company estimates that it can help an average 350-bed hospital tap an extra $22m a year of revenue.

The financial health of all US hospitals is already faced with challenges as the healthcare system across the pond transitions to a value-based approach. That the Trump administration continues to implement regulations on pricing transparency will only intensify the pressure, and support Craneware’s long-term value-cycle strategy and place it as a key trusted hospitals technology partner.

The long-run opportunity justifies the 2020 price-to-earnings multiple of 34-times, and we believe Craneware is a core growth holding for the long-run.

WHY HAS THE SHARE PRICE BEEN WEAK?

WHY HAS THE SHARE PRICE BEEN WEAK?

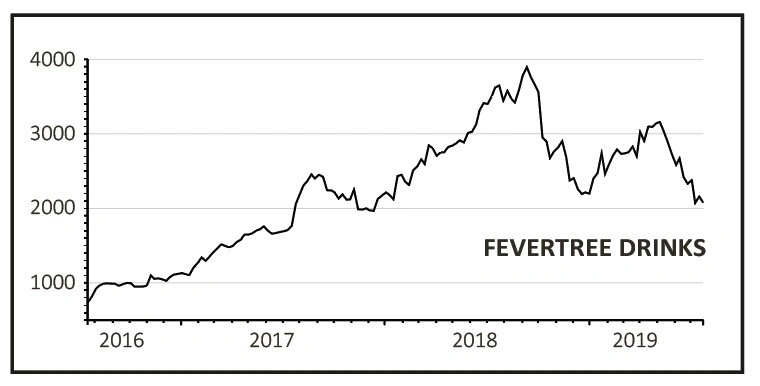

Shares in upmarket mixer brand Fevertree Drinks (FEVR:AIM) have been on something of a rollercoaster. Having started the year at roughly £22, they raced up to £32 by the end of May only to give back all their gains in the past two months.

Investors have gone through a whole range of emotions, from optimism and euphoria to disappointment and despondency.

When the long-awaited first-half results were released last week, revealing that sales growth had slowed to 13% and earnings growth had slowed to just 7%, many holders capitulated and sold out.

The shares lost almost 10% on the day of the announcement, the second time this year that they have been heavily punished for not meeting expectations.

In common with other drinks companies Fevertree had a blow-out start to the summer last year thanks to a combination of hot weather and big sporting events which boosted UK sales.

This year the summer has got off to a soggy start, and with no major events to celebrate. Sales have been steady but growth is well below last year’s levels.

Ironically the first-half results came out as much of the UK was experiencing its hottest July ever so it is quite possible that the third quarter will see a strong rebound in consumption but we won’t know for some time.

The UK still represents roughly half of group sales so a slowdown to 5% growth in the first-half has acted as a major drag on the numbers.

WHAT COULD SPARK A RE-RATING?

The major growth driver for Fevertree going forward is the US market, where it had shown reasonable growth for 10 years via its agent but decided 18 months ago to take a much more hands-on approach and manage it directly.

The step-change occurred last summer when the group signed an exclusive on-trade distribution deal with SGWS, the largest North American wine and spirits distributor.

Given the size of the US market (estimated to be 16 times the size of the UK mixer market) and the increasing trend towards premium drinks and mixers, even a small increase in its current 11% market share would mean a significant increase in sales and earnings over time.

According to S&P Global Intelligence, pre-tax profit is forecast to rise from roughly £75m last year to £106m in three years, bringing the price-to-earnings (PE) ratio down from 41-times to 28-times.

Yes, the shares command a premium rating but we believe the company continues to have a very strong outlook with scope to deliver large earnings growth for years to come.

Current share price weakness may even spur takeover interest from trade players such as Diageo (DGE) and Unilever (ULVR), or private equity.

WHY HAS THE SHARE PRICE BEEN WEAK?

Potash miner Sirius Minerals (SXX) needs a lot of cash if it is to turn its potentially money-spinning polyhalite mine in North Yorkshire into a reality.

The FTSE 250 firm has moved a step closer to that reality after it felt confident enough to launch a $500m bond, part of its efforts to raise $3.8bn so it can carry on with building the mine.

Investment bank JP Morgan has agreed to stump up a $2.5bn overdraft if Sirius gets investors to take on the $500m bond. Combined with $400m in convertible bond sales and $425m raised via issuing new shares, Sirius will have the cash it needs if it can get the latest bond money.

But what has got investors so annoyed with the company is the $425m it raised from new shares, which it bagged by offering them at 15p a share – a significant discount to the 21.9p the shares closed at the day before the placing.

In addition, the cost to build the mine has consistently gone up in the last few years, with Sirius asking for more cash every time.

Having sat at 45p three years ago, its shares are now trading at much lower levels despite the project being more advanced.

WHAT COULD SPARK A RE-RATING?

If it gets the bond money that would effectively eliminate the financing risk with regards to the project.

And analysts covering the stock believe it’s highly likely Sirius will get this cash, meaning the shares could be in for a major re-rating, with Shore Capital analyst Yuen Low saying it is the ‘key to effectively unlocking Sirius’s vast potential’.

Despite the mine being years from production, Sirius has already secured several offtake deals – which is what led JP Morgan agreeing to lend it a huge chunk of the cash – with more in the pipeline, evidence both of the demand for a product whose market does not yet exist, and customers’ belief that Sirius will get this

off the ground.

It started a roadshow for the bond last week, with the bond pricing on 6 August and the deal closing on 9 August.

Once the finance is in place, investors will start to focus more on the opportunity for Sirius as a supplier of multi-nutrient fertiliser and how it can help to improve crop yields around the world.

Despite the potential to be a major employer in the UK and for the shares to re-rate dramatically, investors should not lose sight of the fact that this is a higher-risk investment. There are geological, project execution and market risks to consider, as well as the pressure on Sirius to operate the mine profitably and be able to pay down its sizeable debt.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.