Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy Wizz Air wants to lower fares but increase extras

He made his name as the man who brought Pringles to Hungary.

Now Wizz Air (WIZZ) co-founder and chief executive Jozsef Varadi is once again trying to create waves in Eastern Europe.

The Budapest-based airline has expanded significantly as passengers across the region take advantage of the cheaper cost of travelling, and its boss is on a mission to carry on making air fares lower.

FOCUS ON LOWERING FARES

‘I am invested in lowering fares. It enables us to stimulate the marketplace and get more people interested in flying,’ Varadi tells Shares.

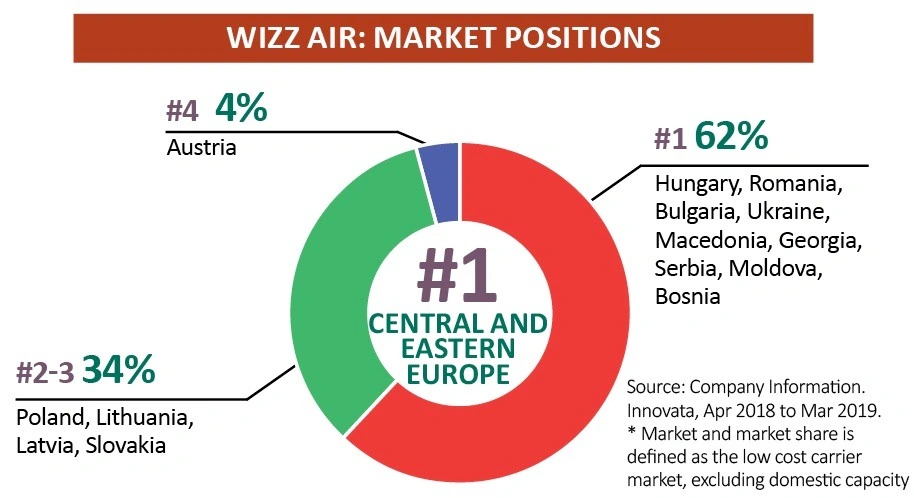

The leading budget airline in Central and Eastern Europe, Wizz Air has upwards of 100 aircraft and operates out of 25 airports.

The company has a particularly young fleet of aircraft which has benefits in terms of reliability and fuel efficiency.

For Wizz Air, lowering fares makes sound business sense given that unlike its more Western Europe-focused rivals, Ryanair (RYA) and EasyJet (EZJ), its main customer base is from Central and Eastern Europe.

Incomes are growing fast in the region, and more people than ever in these countries are wanting to travel and see more of the continent.

But salaries are still not up to the levels of Western Europeans, so the lower the fares the more people who can travel.

And once these people get richer, the more they can then spend on other services with Wizz Air.

‘Central and Eastern Europe is a market that continues to grow twice as much as Western Europe in terms of GDP. So that creates more income as people in the region get richer, and we benefit from that,’ Varadi explains.

The company recently opened in new markets such as Georgia, Israel and Ukraine. It doesn’t yet have the scale of Ryanair or EasyJet, but is growing faster than its competitors, something which is reflected in the divergent tale of their respective share prices.

While it encountered turbulence earlier this year, at £36.04 Wizz Air’s share price is marginally ahead of where it was a year ago. Ryanair on the other hand has seen its share price drop by a third, and EasyJet by around 40%.

Wizz Air’s full-year results to 31 March this year were generally ahead of forecast, with a 6% increase in profit to €291.6m and a 19.6% rise in revenue to €2.3bn.

Ryanair saw profit fall 29% to €1.02bn in its full-year results, which it blamed on lower fares, on revenue of €7.56bn, while in its last full-year results to 30 September 2018, EasyJet recorded a 13% rise in pre-tax profit to £578m, on revenue of £5.9bn.

ANCILLARY REVENUE IS KEY

A key part of Wizz Air’s business strategy is driving ancillary revenue. While this part of the company’s income has drawn praise from shareholders and some of the wider market, it has drawn anger from consumer champions.

Wizz Air has reduced carry-on luggage to just one handbag-sized item, something which has left many passengers in for a nasty shock at the airport.

Airlines such as Wizz Air say this is to speed up boarding, but critics suspect it’s just another ploy to increase revenue.

Regardless, from a business perspective the reasons why Wizz Air and its boss are so focused on ancillary revenue are clear.

After all, ticket prices typically fluctuate depending on market response, whereas the price of the other services the airline provides remains relatively stable.

The more money it can bring in through checked bags, individual seat assignments, hotel commissions, etc, the less it will be impacted by issues such as higher fuel prices, which has caused issues for a lot of airlines.

RISING ABOVE THE COMPETITION

Varadi says Wizz Air makes more ancillary revenue than any other airline in the world – 43% of its total revenue versus 26% from Ryanair and 19.5% from EasyJet.

Ryanair has a stated aim to get 30% of its money from ancillary revenue by 2020, while EasyJet hasn’t set a target.

The aim, Varadi states, is for Wizz Air to ‘cross the 50% line’.

‘Ancillary revenues have been a big focus for us. They tend to be more stable,’ he says.

The risk is that this status alienates prospective fliers and undermines the company’s strong competitive position.

NEW AIRCRAFT INCOMING

What also marks out Wizz Air from its competitors, at least in Varadi’s view, is the new aircraft – the Airbus A321neo – it has ordered.

Having picked out Ryanair as his main rival, the Wizz Air boss sees the A321neo as the reason why the airline can get its unit cost below that of its Irish counterpart.

The Wizz Air boss believes the higher number of seats the airline can cram into the A321neo, plus its better fuel efficiency, means his company will be able to get its unit costs below that of its peer.

He says: ‘These savings enable us to offset cost issues like volatile fares, labour cost pressures and rises in the fuel price. I don’t think [other airlines] have those levers to be able to stabilise costs.’

SHARES SAYS:

Wizz Air is an attractive business and investment bank Berenberg notes that it generates a higher return on capital than Ryanair (16% versus c9%, respectively) and has better long-term growth prospects.

However, airlines can be volatile investments and they operate in a highly competitive market. The trick is to buy the shares when sentiment is very weak towards the sector and the share prices have been beaten up.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.