Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazinePershing Square guru Bill Ackman is enjoying his best ever year

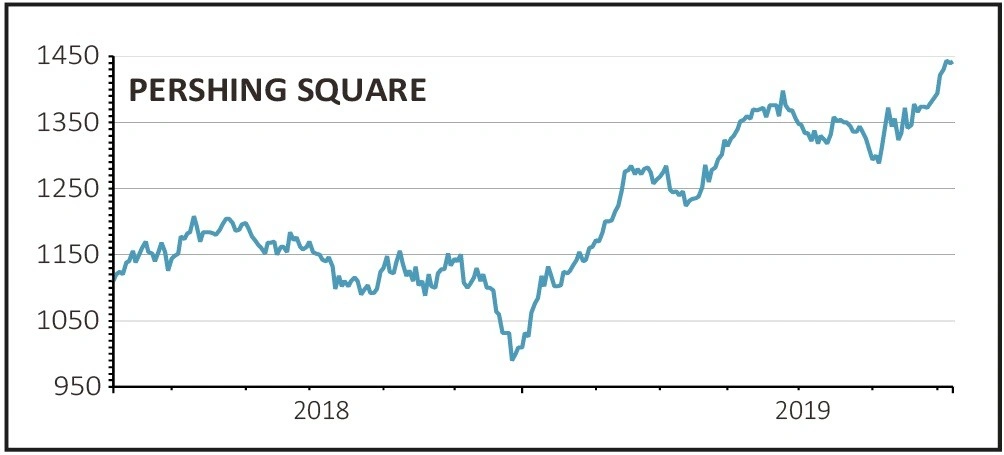

PERSHING SQUARE HOLDINGS (PSH) £14.42

Gain to date: 7.9%

Original entry point: Buy at £13.36, 16 May 2019

Our bullish call on Bill Ackman-managed Pershing Square (PSH) looks well-timed with the shares already up 7.9%.

Last month (19 Jun), Pershing Square announced a bumper $100m share buyback of its shares on the London Stock Exchange and Euronext Amsterdam and the positive news flow continued with the performance report for June.

Pershing Square’s 8% monthly gain means the fund’s NAV rose by a stunning 45.3% in the first half of 2019, dramatically outperforming the S&P 500.

An investment trust that makes concentrated investments in North American-domiciled large caps, we feel Pershing Square’s excessive discount to net asset value (NAV) fails to reflect the quality of the underlying portfolio managed by Wall Street billionaire Ackman’s Pershing Square Capital Management.

The activist investor puts money to work in companies that generate relatively predictable, growing free cash flows with ‘formidable barriers to entry and a compelling value proposition’.

Pershing Square’s recent success reflects the outperformance of the likes of tacos-to-burritos chain Chipotle Mexican Grill and coffee chain mega-cap Starbucks among others.

SHARES SAYS: Bill Ackman is having his best year ever, which means Pershing Square’s massive 25.6% discount to NAV is anomalous. We remain excited by the quality and potential of the concentrated underlying portfolio.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.