Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBoris vs Corbyn: How the changing political landscape could affect your wealth

Britain’s new prime minister will be announced on 23 July. Boris Johnson is widely considered to be the favourite and Jeremy Hunt the underdog. Whichever candidate wins they face a baptism of fire as the 31 October Brexit deadline looms large on the horizon.

Johnson has made bold statements to the effect of Brexit or bust come Halloween. Hunt has been more circumspect, albeit playing to his audience by underlining his no-deal over a no Brexit position.

Brits have been trapped in a minefield of uncertainty for three years and the end is not necessarily close. This leaves investors still facing many tricky questions on the UK economy, the prospects for share prices and investment incomes, plus a whole host of other investment issues.

So whatever your personal views on the best candidate for number 10, whether you think Brexit deal or no-deal (if it comes) will act as a boost or brake to the UK economy, or if a

general election is years away or just around the corner with labour’s Jeremy Corbyn in the running as a future PM, this feature looks at six issues facing savers and investors.

PLAYING TO THE CROWD

The final decision on who takes up residence in Number 10 later this month will be made by the 125,000 or so Conservative Party members.

Building wider popularity is also important for the longer-term. Both Boris Johnson and Jeremy Hunt have made various pledges to cut taxes for consumers and business, boost public sector funding and pay. We’ve also had pledges to bolster investment in key industries, such as fishing, farming, housing and defence, and increase private investor allowances.

Whether those promises become policies down the line is another matter, with even Chancellor Philip Hammond warning against what he views as ‘reckless promises’.

31 OCTOBER IS LOOMING

‘Taking recent comments from the leadership contenders at face value, we think there is a reasonable chance that a new Eurosceptic leader will attempt to push for a no-deal Brexit if they are unable to rework the deal before the end of October,’ say economists at investment bank ING.

John Curtice, professor of political science at Strathclyde University, argues there is little chance of any Conservative prime minister delivering on a promise to leave the EU without a deal on the current exit date of 31 October.

‘Any prime minister who pushed for no-deal would see their government collapse in the autumn and risk a general election where there would be a significant chance that Labour would end up in government before the end of the year,’ adds Curtice.

James Smith, ING’s development markets economist, says a general election is the most likely scenario out of the ones his team have considered, ‘but a more pragmatic approach certainly shouldn’t be ruled out either’. His team puts the probabilities of a general election before the end of 2019 at about one-in-three.

‘While the legislative options may be limited, there is one obvious way that parliament could block no-deal, and that’s to try and force a general election,’ say ING’s experts.

This could be sparked by Corbyn calling for a motion of ‘no confidence’, and it wouldn’t take many Conservative MPs to back it.

‘Several moderate Conservative lawmakers have hinted they would be prepared to collapse their own government if that was the only way of stopping no-deal,’ adds ING.

Six key issues facing savers and investors

1. A POTENTIAL CORBYN-LED GOVERNMENT

Many recent polls across the UK’s electoral system suggest Boris Johnson could hypothetically secure an absolute majority for the party at the next election. But that outcome comes with several caveats, not least that electoral calculators can be relatively crude.

A failure to live up to promises of achieving Brexit by October would undoubtedly give leverage to the Brexit Party and likely cost Johnson dearly.

‘A lot would also depend on Labour’s Brexit position – so far Corbyn has been reluctant to back a second referendum. But polls suggest that if he is to become prime minister, he would need to join forces with several other political parties (The SNP and Lib Dems certainly), almost all of which would set a second referendum as their price for a coalition arrangement with Labour.

Since those comments were made, Corbyn challenged the next Tory leader to hold another referendum before taking Britain out of the EU.

That makes it judicious for investors to start taking seriously the possibility of a change of government.

There is the likelihood that income taxes above the current 45% for higher earners would be on the cards under Labour. And capital gains tax would almost certainly come under the spotlight, with neither prospect likely to go down well with many investors.

Deal or no-deal, impact on UK share prices

DEAL

Pick up in GDP growth – Positive

Appreciation of the pound – Negative

NO-DEAL

Depreciation of the pound – Positive

Economic slowdown – Negative

Source: Capital Economics

2. PROSPECTS FOR UK STOCK MARKETS

You don’t need Jon Snow’s Swingometer to tell you that Boris Johnson could be seen as the better bet for UK investors than Jeremy Corbyn. We say that from a neutral standpoint as Shares does not take sides with politics.

With Johnson, many people would view his victory as a path to less tax rather than tax hikes, pro-business rather than anti-enterprise, and reduced pressure on the public purse, not more.

The prospects of the UK stock market will be tied in with economic prosperity but the possibility of large scale re-nationalisation presents a particularly hot potato for investors.

Possible plans to take some industries out of private ownership and put back in the hand of a Labour government remain loose at present, although they are a clear risk if you’re a shareholder in one of the affected companies.

The most likely targets include many of the UK’s utility suppliers – gas, electricity, water, the railways and postal services – while even BT (BT.A) could be marked for renationalisation, if recent speculation is to be believed.

There has been some chatter that Labour could buy back assets at less than their current market value. But who knows how it would fund such renationalisation efforts.

The biggest likely impact of a widespread Labour-led renationalisation campaign would be the potential message it sends out to the wider world, and Britain’s reputation as a safe and fair destination for overseas investment.

More volatility in the UK stock market is anticipated in the short-term regardless of domestic issues given the global nature of many of our largest companies.

Somewhere in the region of 70% to 75% of revenue earned by FTSE 100 companies comes from overseas which makes things like global growth and the impact of trade tensions just as important, if not more so, to UK share prices as to the person in number 10.

3. GILTS AND GOLD

A Corbyn government post the next general election has the potential to send Gilt (UK government bond) yields soaring (and prices falling), according to experts at Kames Capital. Markets fear the worst over spending and nationalisation plans, but that outcome is far from clear.

The recent rally in global bond markets has pushed out expectations of higher UK rates, with some experts predicting a 25 basis point cut if a no-deal Brexit comes to pass.

‘As outlined in insufficient detail, the Labour Party’s spending and nationalisation policies could end up with a few extra hundred billion of debt on the Bank of England’s balance sheet,’ says Adrian Hull, head of fixed income at Kames Capital.

The Bank of England already has £425bn of Gilts but these were purchased from the market in return for cash for investment elsewhere, according to Hull. ‘The Labour Party has spending plans that will be materially beyond that of the current budgetary balances, and further debt is likely to be issued (or created at the Bank) due to nationalisation programmes.’

Gold is seen as a sensible asset to own when the future is gloomy or unpredictable, and it’s worth noting gold recently hit a seven-year high.

4. THE POUND IN YOUR POCKET

Sterling moves up and down depending on the attractiveness of the UK economy but there are so many moving parts that it becomes a very complex topic.

In the short-term Brexit remains the driving force behind sterling and there is little doubt that a no-deal outcome would hurt the pound. ‘A no-deal Brexit could potentially hurt the euro as well, but by nowhere near the same level,’ adds Investec foreign exchange dealer Chris Brand.

Make UK, which represents 20,000 UK manufacturers, has said it would be ‘the height of economic lunacy’ to take the UK out of the EU without a deal in place.

But while the UK’s future relationship with the EU dominates the UK debate, currencies move for a variety of reasons. ‘While Brexit will be an obvious focus, future relationships with potential trade partners will also be important,’ says Brand. ‘Johnson, for example, might not be liked by the EU, but he would be liked by US President Donald Trump.’

It is tricky to assess a Corbyn government’s impact on sterling but the likelihood would be further weakness in the short-term with investors likely to anticipate a period of economic instability, but trying to predict the pound’s trajectory into an already opaque future is a fool’s errand.

All the more reason to take the longer view on investment markets and not be too swayed but near-term political uncertainty.

Some experts anticipate the pound to rally at some point but more important is that UK investors are globally oriented, and unencumbered by home-country biases even if returns and performance are usually referenced in sterling.

Brexit possible outcomes and chances

Parliament forces a general election 35%

Parliament stops a no-deal by passing a confidence motion. General election takes place in late November or early December

Revamped deal 25%

To avoid a general election at all costs, pro-Brexit MPs reluctantly back a tweaked

deal given there’s a Brexiteer prime minister in place for next stage of trade talks

Second referendum 15%

Parliament may struggle to force a ‘People’s vote’, but cannot fully rule out the prime minister triggering one as the ‘least worst’ option versus a general election

No‑deal 20%

If the EU rejects a further Article 50 extension or a new leader pushes for a hard Brexit, parliament may lack the legislative tools to stop it

Revoke Article 50 5%

Parliament may prefer this option over a no-deal exit, but like a second referendum, MPs could lack legislative tools to force the new prime minister’s hand

Source: ING

5. DIVERSIFICATION, THE FIRST RULE OF INVESTING

Diversification is designed to cap exposure to the threat of setbacks or failure at any one company or country. It is a tried and tested way to cope with the uncertainty inherent in life, politics and the stock market.

It can be achieved in all sorts of ways but is perhaps easiest to manage through a good selection of funds that give investors exposure to equities and stock markets around the world, non-equity assets such as bonds, property and currencies, and even holding cash at times.

There is actually an inherent diversification built in to the FTSE 100 because of the overseas income its constituents generate, so it makes little sense to base investment views on the UK in isolation.

For example, between 2014 and 2015 the UK and US economies both grew at around 2.6% per year, according to Ben Kumar, investment manager at Seven Investment Management, while interest rates and inflation were similar. But those two years were bad for oil prices, which fell by more than 60%.

‘From an economic standpoint, oil is marginal to both the US and the UK economies. Yet in those two years the US equity market rose 11% while the UK equity market fell 8%,’ he explains.

Kumar’s analysis says that the near‑20% difference in performance between the two indices had little to do with the economies of the two countries, and far more to do with how certain sectors have a large influence on stock markets.

‘Oil companies make up nearly a third of the FTSE 100 and fell by about 30% between 2014 and 2015 and this pulled the overall market right down. American energy and materials companies felt the same pain, but because they make up less than 10% of the US stock market the impact was less severe,’ he explains.

‘Many assume one’s asset positioning should be defensive during times of heightened geopolitical conflict,’ says Kleinwort Hambros’ Kamal. ‘History teaches a different lesson, with geopolitics rarely impacting equity markets over the medium to long term of five to 10 years.’

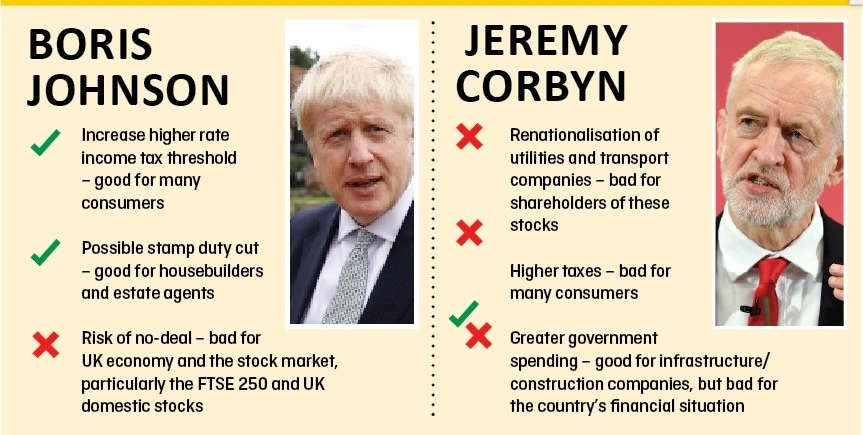

6. HOW COULD BORIS OR CORBYN CHANGE OUR PERSONAL FINANCES?

Boris Johnson

He wants to hand a £9bn tax boost to 4m higher earners by raising the 40% higher-rate tax threshold from £50,000 to £80,000. This could benefit the top 10% of earners to the tune of almost £2,500 a year.

Pensioners enjoying high incomes could be the big winners as they won’t be affected by Johnson’s plan to raise the National Insurance ceiling to help pay for the measure.

Johnson has signalled his intention to raise the level at which NI payments kick in. The IFS believes every £1,000 increase in the level would cost about £3bn a year.

Johnson is rumoured to be in favour of scrapping stamp duty on homes worth less than £500,000. This would represent a major giveaway of up to £10,000 for first-time buyers and £15,000 for other property buyers.

Jeremy Corbyn

Labour has set out plans to bring the 45% income tax threshold down to £80,000 and introduce a new 50% rate for those earning over £123,000.

Shadow Chancellor John McDonnell is eyeing a ‘wealth tax’ which could look to seize 20% of the assets of the richest 10%.

Further changes to retirement savings incentives could be on the cards, presumably focused squarely on higher and additional-rate taxpayers.

Labour is expected to freeze planned increases in the state pension age beyond 66 and look at ways to develop a flexible system which takes account of life expectancy variations.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.