Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy we remain bullish on Tesco

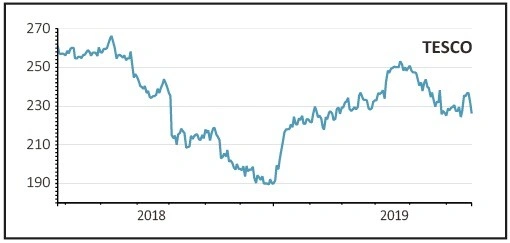

TESCO (TSCO) 226p

Loss to date: 4.6%

Original entry point: Buy at 236.9p, 23 May 2019

Tesco (TSCO) shares have lagged the FTSE 100 since May but we are sticking with our call after the first quarter trading update (13 Jun) and the recent capital markets day (18 Jun).

Despite a tough comparison with last summer, Tesco still managed to increase turnover by more than the market in the first quarter with a particularly strong performance in fresh food. Also the Booker acquisition is delivering growth as planned.

The comparison with 2018 will remain hard in the second quarter given that grocery sales are backward-looking and last summer’s boost was still being felt in the numbers until October.

However, Tesco is focused on keeping hold of its customers, raising its revenue and trimming costs so that its margins and cash generation improve.

As well as working with its suppliers, it has a global sourcing alliance for household products with France’s Carrefour which reduces costs considerably.

Other ways to improve profits include smaller local stores, the Jack’s own-brand range and own stores, increasing use of technology including cashless payment and less expensive but more effective marketing.

SHARES SAYS: Grocery sales are growing steadily and Tesco is the undisputed market leader. Investors are worried about tough comparisons with last year but the company is already planning for next year. Buy.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.