Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe price is right: Royal Mail shares are now a bargain

Are you feeling brave and are happy to make a contrarian call? Royal Mail (RMG) looks like a very interesting ‘buy’ at the current price, albeit recognising this is a high-risk investment.

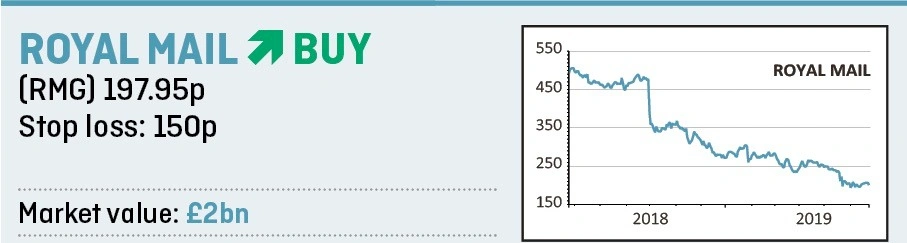

Shares in Royal Mail have fallen by 69% in the past year or so on worries about its shrinking legacy business. They now trade on 0.45 times tangible book value, the lowest in the London Main Market.

We think investors are being too sceptical because the company is now at an inflection point where the growth in UK parcels more than offsets declining volumes in UK letters.

In addition we find it noteworthy that company directors have spent more than £1m of their own money to buy shares since the company outlined its future strategy on 22 May.

Earlier this year analysts had been expecting a dividend cut, and we’ve subsequently had that confirmed by the company. It is now guiding for 15p per share (previous year: 25p) with possible additional payouts in future years with substantial excess cash flow.

Even if there aren’t any supplemental payouts, the base level provides a yield of 7.6% at current prices, not insubstantial in a low interest rate world.

Royal Mail is targeting an improvement in UK productivity of 15% to 18% out to 2023-24. This should result in an improvement in operating margins to 4%-plus by 2021-22 and 5%-plus by 2023-24, compared with 3.9% today.

The company is making changes to production through a redesign of the Royal Mail network, with parcels automation increasing dramatically from 12% to 80%.

While supporting growth and automation changes, management want to keep a tight control of extra capital expenditures. They are aiming to spend £400 to 500m cumulatively over the next five years.

If the forecast operational improvements materialise, the incremental return on that expenditure will be an impressive 38%.

The jewel in the crown for the company is its Global Logistics Services (GLS) division, one of Europe’s leading ground-based parcel networks. It has built its revenues from €300m a decade ago to €3.3bn today, a compound annual growth rate (CAGR) of 25%.

E-commerce growth continues to be the driving force, which has seen the size of the cross-border parcels market increase in value to more than $60bn. Royal Mail is targeting €4.5bn revenue for GLS by 2023-24, a CAGR of 6.4% per year.

Even if the company achieves half of its goals, it should be enough to change the negative sentiment towards the shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.