Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMicro-cap funds caught up in Brexit and Woodford liquidity fallout

Many micro-cap funds are struggling as investors shun the very bottom part of the UK stock market. Weaker sentiment towards illiquid stocks in the wake of the Woodford fund suspension also doesn’t help matters.

The fund managers targeting this space remain confident there is value to be generated from buying select smaller companies. They look for valuation anomalies where stocks trade at a discount to intrinsic worth. A successful micro-cap investment can produce significant returns – but success doesn’t always come overnight.

Many micro-cap funds invest in stocks which are cheap because they’ve experienced financial or operational problems and where the fund manager sees a potential solution. Patience is therefore needed if you are going to invest in this space.

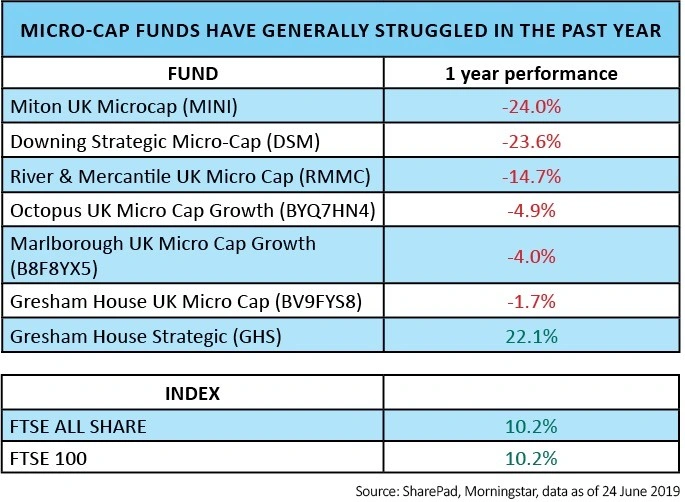

WHY ARE MICRO-CAPS OUT OF FAVOUR?

Micro-caps can suffer from very little trading on the market and so liquidity can be a major problem.

A lack of analyst coverage on very small companies means a lot of stocks are drifting downwards as mainstream investors are simply unaware of a lot of the names. This is the opposite situation to large cap stocks where the benchmark FTSE 100 index has risen by 10% in value this year.

Miton’s Nick Greenwood and Charlotte Cuthbertson, who run Miton Global Opportunities (MIGO), say another key reason why micro-caps are out of favour is structural.

Consolidating fund management groups have become so big (managing bigger pots of money) that companies worth less than £150m no longer ‘move the needle’ for portfolios, leaving micro caps out in the cold in terms of valuations.

And because the big fund management groups won’t buy them, their valuations keep falling, which means larger competitors can swoop in and buy them on the cheap.

THE BREXIT FACTOR

Gervais Williams, who manages Miton UK Microcap Trust (MINI) and LF Miton UK Smaller Companies (B8JWZP2) alongside Martin Turner, says many investors are shunning UK stocks because of Brexit fears.

‘This trend has been even more adverse within UK micro caps,’ he adds. ‘As Brexit has become ever closer in 2019, investors have been particularly reluctant to increase their UK micro-cap holdings.

‘Once the shape of Brexit is known, we believe there will be renewed capital allocation given the UK valuation differential. If this is accompanied by an appreciation of sterling, then companies with significant domestic exposure will be better placed. For both of these reasons we believe that UK micro caps are well placed going forward.’

WOODFORD GATING FALLOUT

The suspension of LF Woodford Equity Income Fund (BLRZQ73) – in order to give fund manager Neil Woodford time to sell his illiquid holdings – has put the spotlight on liquidity.

It has reminded investors that they cannot always sell their investments exactly when they want to. It has also served to remind investors that investment funds come with liquidity risks. That’s served to widen the discount to net asset value on several investment trusts targeting the micro-cap space.

Williams says: ‘Unfortunately, there is some terminology ambiguity here in the stock market which is really unhelpful. Specifically, the term “illiquid” can extend from private, unlisted heavily loss-making stocks where their valuation is somewhat subjective, to small, publicly listed companies that are profitable, cash-generative with a valuation that is determined by shareholder transactions.

‘The danger is that anxieties about private loss-making companies may end up adversely influencing investor behaviour regarding micro-cap and small cap listed companies, which subsequently impedes their ability to raise capital and drive up future UK productivity, employment growth and tax take.’

OPEN-ENDED FUNDS

The Woodford debacle has reignited the debate about illiquid stocks being better suited to a closed-end fund structure, so the fund manager isn’t forced to conduct a fire-sale of assets when investors want to take their money out.

However, Williams takes the view that a well-managed portfolio of small and micro-cap companies can operate well within an open-ended fund structure.

Judith MacKenzie, manager of investment trust Downing Strategic Micro-Cap (DSM), says the Woodford scenario points to a more pertinent point. ‘I think the size of some funds has become a detractor from ability to actively fund manage, particularly smaller cap positions,’ she says.

MacKenzie prefers to run concentrated portfolios and have a limit on how much money is being managed. She targets 25 to 30 positions in a portfolio with circa £30m to £50m funds under management. ‘I’d get very nervous managing liquidity in a fund bigger than that investing in this space.’

BUCKING THE NEGATIVE TREND

One of the better performers in the micro-cap funds space recently is Gresham House Strategic (GHS:AIM), run by Graham Bird who applies private equity style techniques to construct a high conviction, concentrated portfolio with value characteristics.

It is currently trading on a 14.3% discount to net asset value despite having delivered 22.1% share price gains over the past year.

Gresham House Strategic is also one of a number of micro-cap trusts that sit in the portfolio of Miton Global Opportunities, an investment trust which invests in other funds.

Relevant trusts in the Miton portfolio including Downing Strategic Micro-Cap, River & Mercantile UK Micro Cap (RMMC) and Henderson Opportunities Trust (HOT), the latter not specifically badged as a micro-cap fund but still offering exposure to the theme.

The managers of Miton Global Opportunities have been taking advantage of double-digit discounts to NAV on the grounds that the out-of-favour micro-cap asset class is set for a re-rating.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.