Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineInvestors get a second bite of the cherry after Carnival lowers guidance

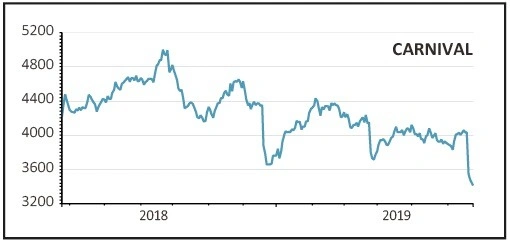

Carnival (CCL) £34.24

Loss to date: 12.7%

Original entry point: Buy at £39.35, 13 June 2019

We reiterate our buy stance on Carnival (CCL), following a fall in the shares in reaction to the company lowering its full year guidance for earnings per share by 3% to 5% to between $4.25 and $4.35.

The bulk of the downgrade was down to propulsion issues at Carnival Vista, and a change to the US government’s policy towards Cuba, both one-off issues which reduced revenue yields.

There was also a small impact from capacity increases in Germany and economic deterioration in France, although these were partly offset by lower fuel consumption and favourable foreign exchange movements. It should be noted that the second quarter results were ahead of prior guidance.

A change to annual earnings guidance of this magnitude does not hugely impact longer term earnings potential. For some perspective, it is always useful to keep in mind that equities are long duration assets, discounting 20 to 30 years of future earnings.

Analyst Greg Johnson of Shore Capital points out that Carnival’s enterprise value-to-berth is currently less than $170,000. He says: ‘A value of under $170,000 per berth has only previously been seen during periods of extreme stress, notably during the Gulf War, the Financial Crisis and the sinking of the Concordia.’

SHARES SAYS: Disappointing but certainly no reason to abandon the trade. Stay positive.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.