Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFirst-time investor: how to plan and what to buy

Taking your first steps with investing needn’t be a frightening experience if you know what’s involved.

We’ve created a step-by-step guide covering all the main points you need to think about, including whether investing is actually right for you.

Our guide also includes pointers for spotting the products most suitable to your needs, how much you might be able to make, and classic mistakes to avoid.

1. WHY SHOULD I INVEST?

Most people want to invest to make more money than they’d get from putting cash in a bank or building society account. But that doesn’t mean investing is right for everyone.

Investing involves taking higher risks in order to obtain higher rewards. Investing in shares, in particular, comes with much greater risks than putting cash in the bank.

You can lose money with shares, potentially everything if the business goes bust. In contrast, cash in the bank is protected up to £85,000 per financial institution – under the Financial Services Compensation Scheme – and the only real threat to cash is the impact of inflation eating away at the true value of your money. Rising inflation means goods costs more and so each £1 you have will buy you less.

IS INVESTING RIGHT FOR YOU?

You should only invest money you can afford to lose. Anyone with a nervous disposition may not be suited to investing, nor someone who is reliant on their money not dropping in value over a specific time.

If you’re still happy to proceed, you need to address these three points: your investment goals, time horizon and risk appetite.

An investment goal might be having a pot of money to pay for a house deposit, a holiday of a lifetime, a loft conversion or to supplement your pension in retirement.

The time horizon really matters as the longer you have to invest, the more time your money can be put to use in the markets. By reinvesting any dividend payments you own more fund units or shares and enjoy compounding benefits. Effectively you’re receiving interest on the interest that’s been paid.

Short time horizons come with the risk of a market correction and so you may not have enough time for the value of your investments to recover before you need to access the money.

WHY RISK APPETITE MATTERS

Risk appetite will help when deciding which investments to make. If you have a low appetite for risk you may prefer to invest in bonds rather than shares. You can invest directly or through funds holding that asset class. If you have a higher appetite for risk, you may want to look at shares, funds investing in shares, or potentially high-yield bonds.

The world of shares could even be split into different levels of risk such as medium risk for supermarkets or higher risk for oil producers or airlines.

The other thing to consider is whether you need to take a certain level of risk in order to hit a financial goal. If you need to make 10% a year for three years to hit a goal, for example, then a low appetite for risk would leave you in a pickle. You would either need to invest in higher risk products to realistically hit the goal, extend your investment period so as to only need a lower return each year, or reduce your goal.

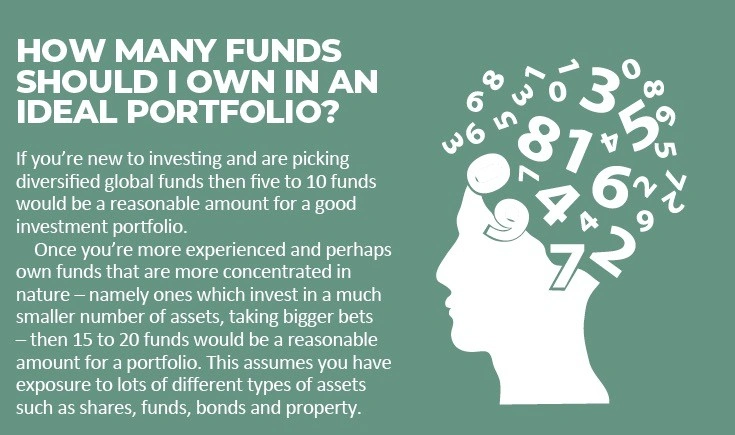

How many funds should I own in an ideal portfolio?

If you’re new to investing and are picking diversified global funds then five to 10 funds would be a reasonable amount for a good investment portfolio.

Once you’re more experienced and perhaps own funds that are more concentrated in nature – namely ones which invest in a much smaller number of assets, taking bigger bets – then 15 to 20 funds would be a reasonable amount for a portfolio. This assumes you have exposure to lots of different types of assets such as shares, funds, bonds and property.

2. HOW MUCH CAN I MAKE?

It is important to set appropriate expectations for potential investment returns. If you’ve only ever come across people talking about investing in films such as Trading Places and The Wolf of Wall Street, you may think 100% gains each year are normal. Sadly, they are not.

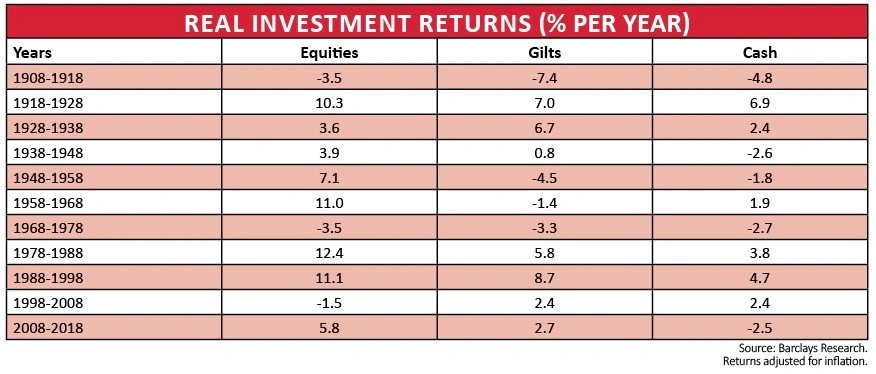

UK shares have achieved 4.7% average return each year over the past 50 years when adjusting for inflation, which is known as ‘real returns’. This is according to a study by Barclays. So if inflation were running at the Bank of England’s 2% target, you could feasibly make 6.7% return in a year on an unadjusted basis.

This figure is just an average and it is important to understand that some years you can make more – and some a lot less. For example, the inflation-adjusted return on UK shares was -3.5% a year between 1968 and 1978, finds Barclays, so you would have lost money. The following decade was much better with 12.4% annual inflation-adjusted returns.

Have a look at the table to see how shares have compared with government bonds (gilts) and cash over certain periods. UK government bonds are considered low-risk products because no-one thinks the government will default on the debt and fail to pay back your money. The returns from gilts have generally been better than cash, but not always by much.

If you’re buying a fund, make sure you understand the different types of asset classes in its portfolio. For example, some funds only contain equities which is another word for stocks and shares – in this case it would be feasible to expect similar returns to owning individual company shares.

Other funds may contain assets such as shares, bonds and property and so the returns may not be as high as a share-only fund as it contains a mixture of higher and lower-risk assets.

3. HOW MUCH DOES IT COST TO INVEST AND IS THERE A MINIMUM AMOUNT?

In general it costs about £10 to buy or sell an exchange-traded fund (ETF), an investment trust (a type of fund) or a stock. You typically have to pay an annual or quarterly fee to the company you use to make investments, such as AJ Bell Youinvest, Barclays Stockbrokers, Interactive Investor or The Share Centre.

In AJ Bell Youinvest’s case, it charges £9.95 to buy or sell in its ISA and then 0.25% of the value of the shares, gilts, investment trusts or exchange-traded funds (ETFs) in your account, capped at £7.50 per quarter. Funds classified as unit trusts or Oeics are cheaper to buy and sell, at £1.50, and ongoing charges are tiered depending on how much money you have invested. A portfolio of unit trust and/or oeic funds worth less than £250,000 in value would attract a 0.25% annual fee.

You may ask if there is a minimum amount of money needed to invest. While investment platforms may let you put a very small amount of money in a fund or buy a single share worth 50p, you must consider the impact of charges on the overall cost.

There is no point buying a share for 50p when the dealing cost is nearly 20 times this amount. You are better off feeding cash into your ISA or other investment account until it becomes a decent chunk whereby the dealing cost would only be a fraction of the overall transaction.

For example, saving up £400 is a more reasonable amount to buy shares or a tracker fund.

The rough £10 dealing fee would represent 2.5% of the investment which isn’t too bad if you are thinking about holding the shares or tracker fund for many years. But clearly the higher the amount you invest, the lower the percentage the transaction costs represent.

HOW TO CUT COSTS

One way to reduce your costs is to use the regular investing services offered by most investment platforms which can cost as little as £1.50 for all asset classes including ETFs and shares.

Your order is pooled once a month with other investors’ orders which helps to keep the overall transaction cost low. The downside is that you don’t get to choose the day in which the order is made.

Before you splash the cash, you must first consider how much you can really afford to invest. We recommend you create a monthly household budget so you know how much money is coming in, such as from your salary, and how much your bills cost. Then you can see how much is left for casual spending and investing.

Make sure you pay off any large borrowings in the form of personal loans or credit cards first before investing, particularly if they come with large interest rates.

4. WHICH TYPE OF ACCOUNT SHOULD I CHOOSE?

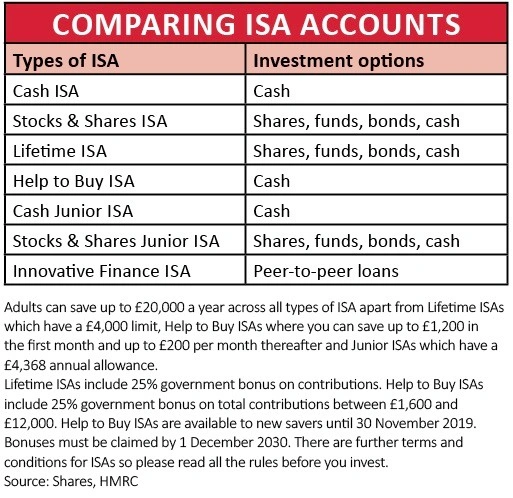

ISAs should be your first consideration as these offer tax benefits and generally don’t have the same access restrictions you get with pensions, although the latter do come with tax relief.

One exception is a Lifetime ISA which imposes a 25% penalty if you are withdrawing money for reasons excluding buying your first home, terminal illness or reaching the age of 60.

All capital gains – the extra money you make when an investment goes up in value – and dividend payments are free of capital gains tax or income tax for everything held inside an ISA wrapper.

A dealing account should only be used if you’ve used up your annual ISA allowance which is currently £20,000. Here capital gains and dividends are subject to tax, although you do get certain allowances each year.

The other option is a SIPP which stands for ‘self-invested personal pension’. Here you can run your own pension pot and benefit from tax relief.

5. WHAT SHOULD I PUT MY MONEY INTO?

Anyone new to investing should consider funds first. Here you benefit from instant diversification so if something goes wrong with one of the holdings in a fund, the other holdings should act as a cushion and prevent a large amount of damage to your wealth.

Owning just a handful of individual company shares puts you at risk of significant wealth destruction if something goes wrong with one or more of them.

Going down the funds route may mean you give up some of the potential returns you could get from having individual stocks, but that’s not a bad price to pay if it means you smooth out the ups and downs from the market.

Your choices include passive funds such as ETFs which are low cost and track different indices. For example, you can get an exchange-traded fund which moves in line with the FTSE 100, an index of the 100 biggest stocks on the London Stock Exchange. If the FTSE 100 moves up by 2% in value, so does your ETF.

Passive funds come in various forms including ones tracking certain geographies; others can include specific sectors or styles such as dividend-paying assets.

Another option is an active fund where all the decisions about what is bought and sold are made by a fund manager.

Active funds come in all different shapes and sizes and cover the investment trust, unit trust and Oeic world. Some place big bets with concentrated portfolios, often only containing 20 stocks. Others offer much broader exposure such as through a portfolio of 100 or more stocks.

RETURNS COME IN TWO FORMS

You can make money in two ways with investing. One is through capital gains which is your investment rising in value. The other is through dividends.

Many funds give you the choice of buying an ‘inc’ or ‘acc’ version of their product. You buy the ‘inc’ version if you want to collect any dividend payments as cash or the ‘acc’ version if you want to roll-up any dividends into owning more units or shares in the fund.

The frequency of dividend payments varies from fund to fund. Not all funds pay them, but those that do have historically paid out twice a year. More recently frequencies have increased to quarterly or even monthly for some funds. Please note that investments do have the right to cut or suspend dividends, so you must appreciate they aren’t guaranteed forms of income.

Once you’ve built up experience with investing, it is only natural to want to buy individual company shares. When you feel comfortable taking this step make sure you do thorough research and don’t overpay for something.

Just remember that large companies such as those in the FTSE 100 aren’t guaranteed to make you money.

Even the biggest businesses experience problems or go out of favour with investors. There are no guarantees that funds will make you rich, either. You can still lose money from them if the fund manager has made the wrong selections or the market you are tracking goes into decline.

Classic first-time investor mistakes

Buying what’s deemed to be ‘hot’ such as crypto-currencies or cannabis stocks

Buying small stocks hyped by people on social media and underappreciating they are very high risk

Not having enough patience and trading in and out of stocks or funds, thereby incurring lots of dealing costs

Investing too small an amount so the overall transaction is dominated by dealing costs

Not taking advantage of tax benefits – i.e. failing to use an ISA and using a dealing account instead

Investing cash that’s subsequently needed to pay bills

FIVE FUNDS FOR FIRST-TIME INVESTORS

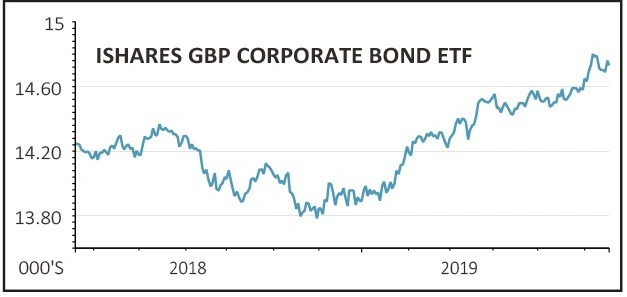

iShares GBP Corporate Bond ETF (SLXX)

You may have been told by a friend or family to start your investing journey by putting money into government bonds. We think high quality corporate bonds might be a better place to start as the returns could be a bit better for only taking a small amount of extra risk.

The iShares passive exchange-traded fund tracks an index of bonds issued by high quality companies. Buying a bond effectively means loaning someone money in exchange for receiving regular interest payments over a fixed period of time.

When bonds mature you get your initial money back, assuming you bought at par value which is the price at which the bonds were first issued. If you bought above par then you would get back slightly less at maturity, or a bit more if you bought below par.

The iShares product currently invests in a range of bonds including some issued by banking group Barclays (BARC) and supermarket giant Walmart.

BNY Mellon Global Income (B7S9KM9)

This is a great place to start if you’re looking to invest in high quality companies around the world. The fund, which used to be called Newton Global Income, has stakes in such companies as soft drinks giant PepsiCo and technology conglomerate Cisco Systems.

Although this is an income fund, currently yielding 3.1%, you can buy a specific version of the fund if you want to use dividend payments to enhance the value of your holding in the fund. Buy the ‘acc’ version – which has the code B7S9KM9 – and the fund will do all the reinvestment for you.

The alternative is to buy the ‘inc’ version – which has the code B8BQG48 – and receive dividends as cash payments every three months.

Anyone who has time on their side and doesn’t need the income should really buy the ‘acc’ version to enjoy the benefits of compounding over time.

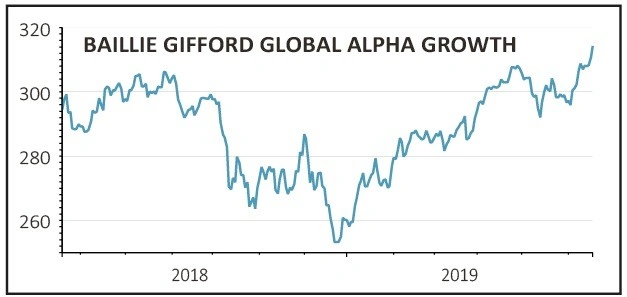

Baillie Gifford Global Alpha Growth (B61DJ02)

Many people would seek to buy the most popular fund on the market, believing it to be a favourite among a lot of investors because of its skills and performance.

Fundsmith Equity (B41YBW7) is arguably the most popular at the moment, but we believe the Baillie Gifford fund could be a better choice for a first-time investor for several reasons.

It is cheaper and more diversified than Fundsmith and also smaller in terms of the assets under management and therefore more nimble. It invests in companies which it believes offer above-average profit growth including life insurer Prudential (PRU) and payments network MasterCard.

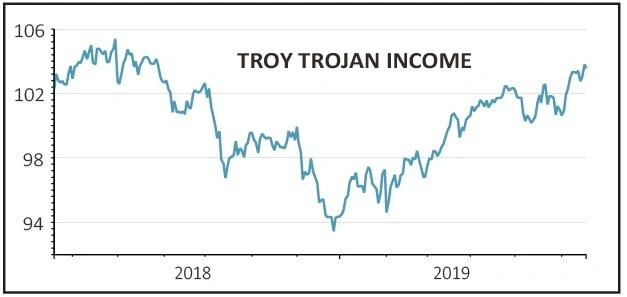

Troy Trojan Income (BZ6CQ17)

This is an actively-managed fund with a focus on capital preservation. Don’t be fooled into thinking the fund doesn’t want to make money for you.

Its slow and steady approach has certainly been good over the years with the fund having generating 11.85% annualised returns over the past decade.

Its strategy is to be careful with how money is allocated and to not take wild bets on potentially iffy companies.

The fund invests in UK-listed stocks such as oil producer Royal Dutch Shell (RDSB), catering group Compass (CPG) and credit agency Experian (EXPN).

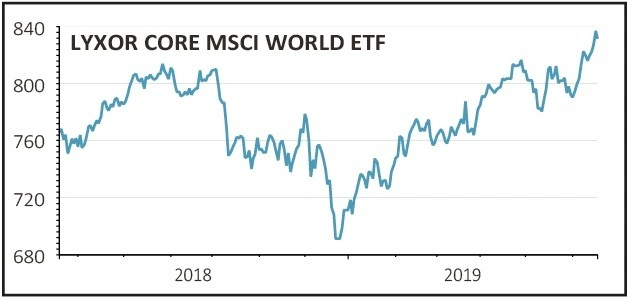

Lyxor Core MSCI World ETF (LCWL)

This is a passive exchange-traded fund and the ideal first investment as it provides exposure to a diverse range of companies around the world for a very low annual cost of 0.12%.

It tracks the MSCI World index which is a basket of more than 1,600 stocks trading on 23 different developed market countries. Among the names in the index are Microsoft, Apple, Johnson & Johnson and Nestle.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.