Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineUnderstanding the different investment fund charges

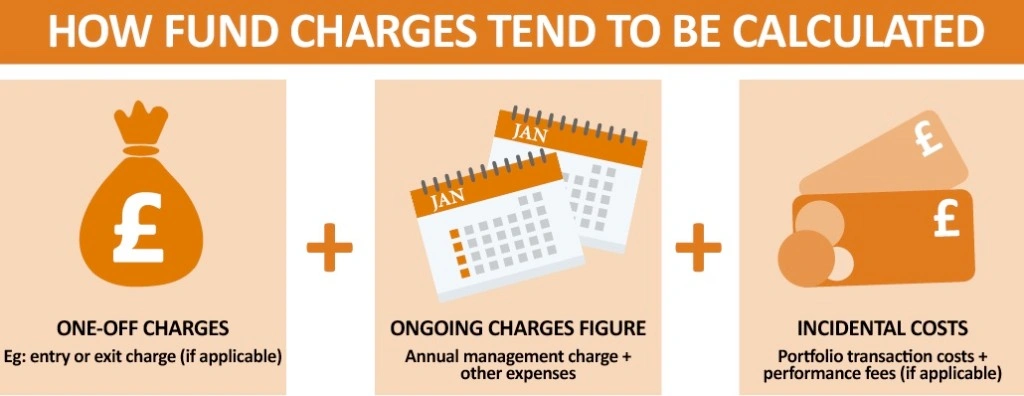

Funds are obliged by the regulator to display their ongoing charges figure (OCF) to give investors a clear picture of the total costs they will pay for buying, selling and holding units in a fund.

The lion’s share of the OCF is related to fees paid to the fund manager. This is to compensate the manager for providing stock selection, portfolio construction and risk management.

Actively managed equity fund fees typically range from 75 basis points (0.75%) to 250 basis points (2.5%) per year, although you can get cheaper ones. Bond funds can be cheaper still.

The second largest part of the OCF is the administration fee. The administrator plays an important role in managing a fund, as they do the work which links the trading in the fund to the valuation of the assets and keeping unit holder records.

Fund managers are not permitted to handle client money directly; all the buying and selling decisions in the fund are transacted through an authorised broker who then liaises with the administrator in order to settle the trades.

Administrators provide a daily or monthly valuation of the assets in the fund, keep the register of fund holders, calculate performance fees and provide safe custody of the assets.

HOW MUCH DOES THE ADMINISTRATOR GET?

The administrator usually charges the fund based on a percentage of the assets under management or AUM.

A typical rate might start at 0.25% on the first £100m, with a sliding scale applied for higher amounts. For the very large funds with billions of pounds worth of assets, the manager will negotiate a maximum administration fee.

Many people assume that the larger funds have the lowest administration fees. Analysis by AJ Bell finds little evidence that this is true.

The administrator receives higher fees when the fund’s assets grow, while it may not do any extra work to earn the higher fees.

OTHER FEES TO CONSIDER

The third element of the OCF is swallowed up by fees related to regulation, such as auditing fees, independent directors’ fees and stock exchange listing fees. These could be around five basis points (0.05%) for a fund that has £100m in assets.

It doesn’t stop there. If you buy your fund units through a platform, and let’s face it, most retail investors do, you will also pay a platform fee. The FCA, a regulator, wants funds to include the distribution costs into the OCF but that doesn’t always happen.

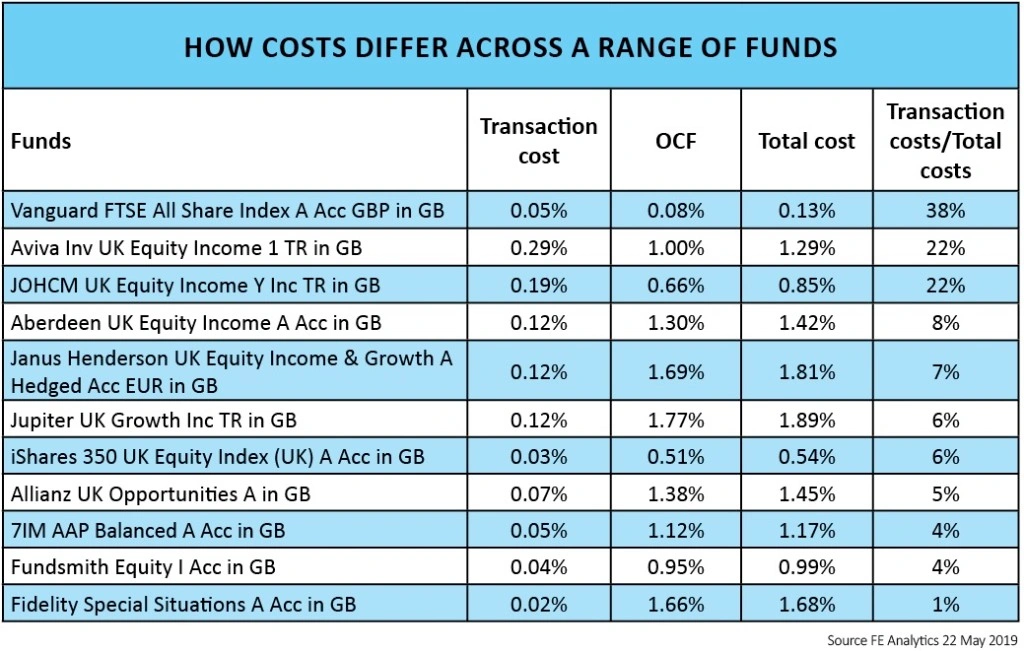

TRANSACTION COSTS

Transaction costs of buying and selling portfolio holdings are not included in the OCF.

For a large FTSE name, dealing costs average around eight basis points (0.08%). There is also a spread between buying and selling prices of around six basis points (0.06%).

Total dealing costs can vary enormously from fund to fund, depending on how often the fund manager chops and changes the portfolio.

HELPING INVESTORS

Research by an FCA-sponsored team suggests that simply providing consumers with information does not guarantee that they will use it in their decision-making. However, clearly presenting understandable and engaging information in a prominent way can increase the effectiveness of disclosures.

Investors should carefully look at the charges and ask the manager if it is not clear, so that they can make informed decisions.

The most effective way to get investors to incorporate charges into their decisions is to take a leaf out of the tobacco industry and clearly label warnings.

There could also be more work done around transaction costs and how these relate to different styles of management. For example, some managers have a buy and hold strategy with low transaction costs while others have more of a trading approach.

Both of these strategies are fine – and higher costs can be justifiable if the manager and their approach generates superior results.

There is some evidence to suggest that funds with the lowest fees tend to outperform funds with high fees. But you should not assume that all low-fee funds are the best.

Greater compliance with the rules should lead to more transparency and hopefully better outcomes for investors. Ultimately it’s about investors being able to identify value for money rather than pure lowest cost.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.