Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy criticism of Burford Capital is unfair

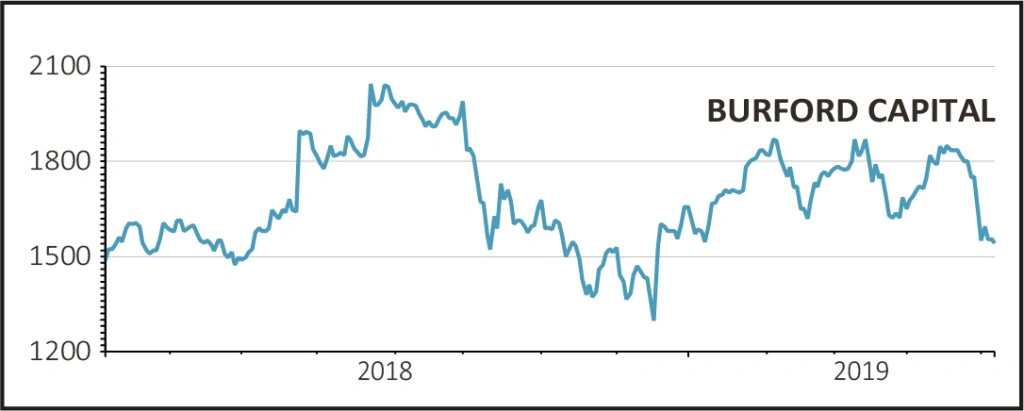

Burford Capital (BUR:AIM) £15.50

Loss to date: 1%

Original entry point: £15.62 (25 Oct 2018)

It has been a trying time recently for Burford Capital (BUR:AIM) after analysts at broking firm Canaccord Genuity cut their earnings forecasts and their target for the stock.

The broker has challenged Burford’s claimed 85% return on invested capital (ROIC) and argues that future returns may be lower than the market expects. It also suggests that the firm may need to raise more capital.

Therefore, it argues, the current valuation doesn’t reflect the risks involved in owning the stock and it has cut its target price from £15.43

to £11.96.

On the day the broker published its note

(30 April) the shares lost 118p or nearly 7% of their value to £16.35, and since publication the shares are down over 200p or 11.5% to £15.50.

NO QUESTION OVER THE GROWTH

Litigation finance is a highly attractive business which continues to grow quickly and Burford has successfully built itself a market-leading position.

In its first year of business almost a decade ago, it received 131 enquiries for funding. Last year it received 1,470 enquiries for funding, so there is no lack of demand.

However income can be very ‘lumpy’ as investments take between 18 months and two years on average to come to fruition.

Over half of the enquiries that entered Burford’s underwriting pipeline last year were related to cases where the estimated damage claim was over $100m. Typically the bigger and more complex a case, the longer it takes to settle.

By its own admission, Burford is now more like an investment bank for the law business than a litigation funder. Last year it committed $1.3bn of funding, more than three times the amount it invested in 2016, as well as launching a $1bn ‘strategic capital relationship’ with one of the world’s biggest sovereign wealth funds.

QUESTIONS OVER THE RETURNS

Canaccord argues that Burford’s claimed 85% ROIC is misleading and it believes the ‘real’ return on concluded investments is 51%. It believes that going forward the company should reference the lower number in all of its reporting.

The broker has cut its 2019 and 2020 earnings forecasts by 18% and has questioned whether Burford will be self-funding by the end of the year or whether it will need to raise more capital, diluting returns for shareholders.

In Burford’s defence, the company complies fully with IFRS accounting and it is the accepted norm to assume a fair value for the portion of investment which is ongoing while cases are pending final settlement.

SHARES SAYS: Take advantage of the pullback to buy more shares.

DISCLAIMER: The author owns shares in Burford Capital

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.