Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy Ankara and Buenos Aires remain important to global portfolios

Last summer, many analysts were wondering whether Turkey was about to pull the rug from under global financial markets. Ankara’s currency, the lira, was in free fall as the economy over-heated and found itself over-reliant on foreign capital for funding, via a large current account deficit.

A stronger dollar, fuelled by higher US interest rates, was draining away liquidity and the reluctance of President Recep Tayyip Erdogan to follow what was seen as orthodox policy in the West – namely to jack up interest rates – was making matters worse.

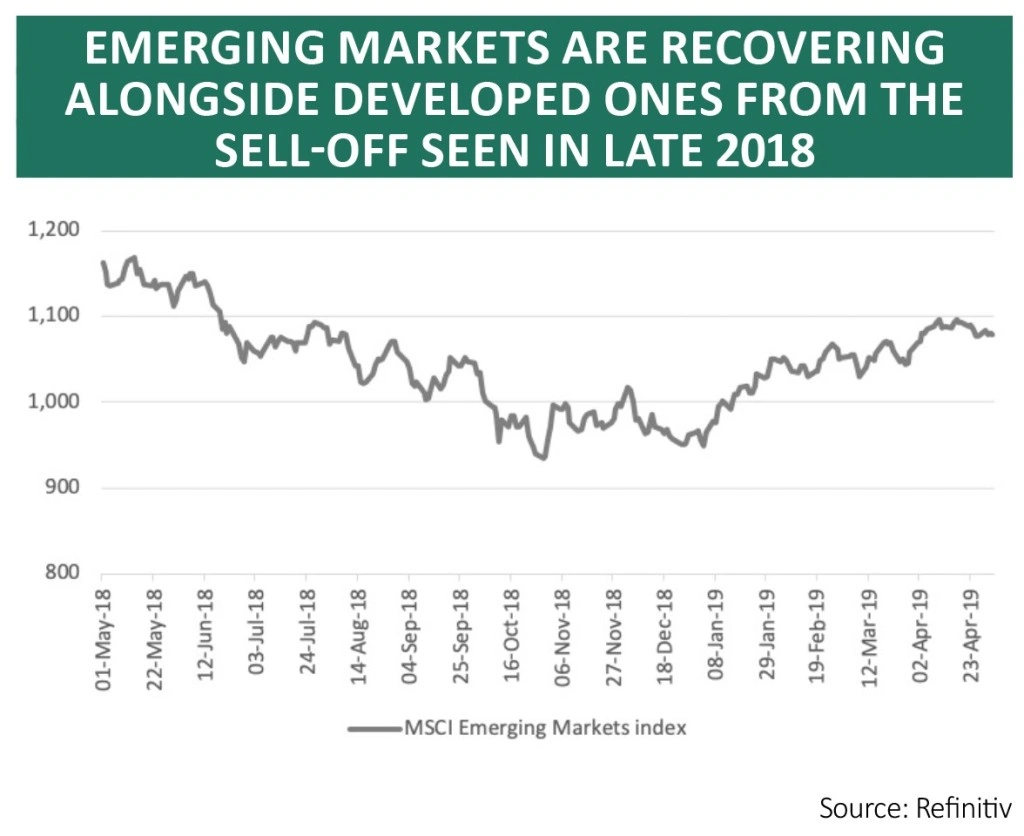

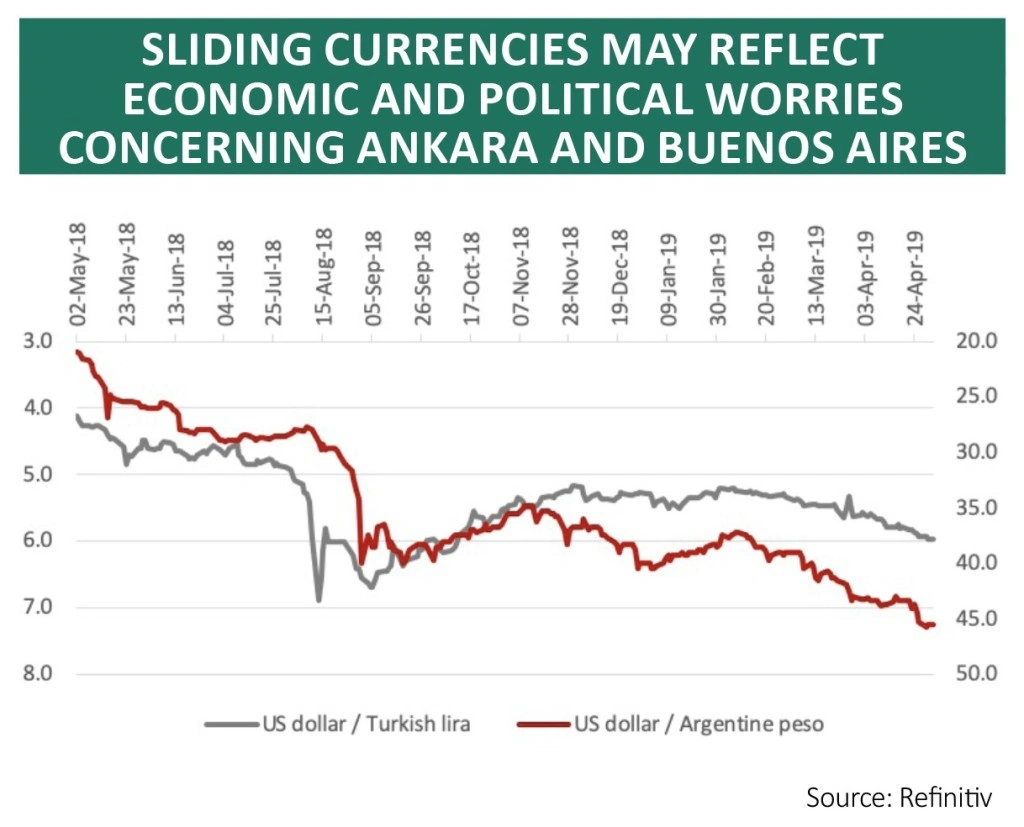

Yet last winter’s wider market panic is seemingly becoming a distant memory. As this summer approaches Turkey seems to barely warrant a mention, even though inflation is still near 20%, the lira trades 10% lower against the dollar compared to January and the economy is in recession, thanks in part to the prevailing 24% interest rate which the Central Bank of Turkey is using to defend its currency.

The weak economic outlook is having a political impact, too, with President Erdogan’s Justice and Development Party (AKP) losing ground in this year’s local elections (which may explain why he was less than keen on those lofty interest rates).

The opposition CHP party won five of the country’s six major cities, although a contested ballot in Istanbul is about to be re-run.

Another election which may require more of investors’ attention is the one due to be fought in Argentina in October. An inflation rate of more than 50% and a near-halving of the peso’s worth from nearly 23 to the dollar to barely 45 are pouring the pressure on right-wing President Mauricio Macri and giving impetus to the opposition’s campaign, spearheaded by his left-wing predecessor Cristina Fernandez de Kirchner, whose policies are blamed by many economists for the country’s current woes.

SMALL EARTHQUAKES, NO-ONE INJURED

Yet it is easy to see why some economists and strategists are arguing that any upset in Ankara and Buenos Aires are just local difficulties that should not unduly influence the performance of investors’ portfolios.

Turkey is a small part of the emerging markets indices. It represents just 0.7% of the assets of Vanguard FTSE Emerging Markets ETF (VFEM), which tracks the performance of 1,083 individual emerging market equities.

Argentina is not even classified as an emerging market, but a frontier one and the Buenos Aires exchange provides just 14% of the assets of New York-listed exchange-traded fund iShares MSCI Frontier 100 ETF – which tracks the MSCI Frontier Markets 100 index.

No other emerging markets have anything like the same inflation problems as these two locations, with most leading emerging markets nations coming in at 5% or below.

Even after his embarrassment in the local elections, President Erdogan looks unassailable after constitutional changes and the AKP’s crushing general election win of 2018.

And while Macri could be unseated – especially as he appears to be reaching for the desperation (and surely discredited) measure of price controls to try and fix inflation – global markets have witnessed the arrival of left-wing governments in Argentina before without being unduly concerned.

ACTION REPLAY

Equally there remains the risk that such a view is complacent. An economic crisis and currency slide in Malaysia in 1997 went on to have global implications in 1998, as the FTSE All-Share and FTSE All-World stock indices both fell sharply as ripple effects led to a devaluation in Russia and the meltdown (and subsequent bail-out) of the Long-Term Capital Management hedge fund.

Contagion is possible. Losses in one market can lead to fund redemptions or the search for liquidity from others. That is why all correlations go to one during financial crises and any fund manager brave enough to have argued two years ago that it would be different this time in Argentina under Macri is getting their deserved reward.

Buyers of the country’s 100-year bond, issued in 2017, have seen the paper slide to barely 73 cents on the dollar, to add their currency losses.

It remains to be seen whether Turkey or Argentina’s problems remain local or go global but attention should be paid, not least as there remains the risk that a worldwide trend gives emerging market assets pause for thought.

Even though the US Federal Reserve is putting interest rate rises on hold, the dollar, as benchmarked by the trade-weighted DXY or ‘Dixie’ index, keeps rising, thanks to the (relative) strength of America’s economy.

And keen students of market history will know that a bouncy buck can hurt emerging markets – especially those that have lots of overseas debt, like Turkey and Argentina, to pluck just two names out of the air.

The MSCI Emerging Markets equity index may be trading some 15% below its January 2018 high with good reason after all.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.