Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe rise of market power and what it means for investors

In November last year we examined the issue of ‘skew’ in markets and suggested one explanation for the outsized contribution of a few stocks to the market’s overall return might be their outsized returns on capital compared with the market average.

We said at the time that a few firms – notably Amazon, Google and Microsoft – had used their technology to create dominant market positions with no ‘trickle-down’ benefit for their competitors.

This market power enables them to raise prices to consumers while limiting increases in salaries for their workers and turn more of their revenue into profit, for the benefit of shareholders.

The economic implications of this concentration of market power is a hot topic of discussion among policymakers and regulators, and while the debate hasn’t hit the mainstream yet it’s important for investors to grasp the concepts involved.

WHY DOES MARKET POWER MATTER?

In its April World Economic Outlook, the International Monetary Fund (IMF) looked at the evidence for the existence of market power and its potential consequences.

It found that since the year 2000 market power has clearly increased in advanced economies, but not yet in emerging ones; and that the increase has been ‘fairly widespread across industries but concentrated among a small fraction of firms’.

It also found that while the macroeconomic effects so far have been small, ‘further increases in the market power of these already-powerful firms could weaken investment, deter innovation, reduce labour share incomes and make it more difficult for monetary policies to stabilise output’.

The IMF examined whether market power was responsible for what it called ‘worrisome’ current economic trends. These include the low level of corporate investment despite low interest rates; the growing gap between returns on capital and those on safe assets like government bonds; the growing gap between financial and productive wealth; falling productivity; and growing income inequality due to the falling share of income going to workers.

While other factors may explain some of these negative trends, it found that increased market power has contributed to all of them. The question is, what has caused it and what is the appropriate response?

SURVIVAL OF THE FITTEST

For policymakers and regulators, the key issue is whether the dominance of a small group of companies is the result of anti-competitive market regulations and weak anti-trust enforcement, or whether it is a case of ‘winner takes most’ as more productive and innovative firms take market share from weak competitors.

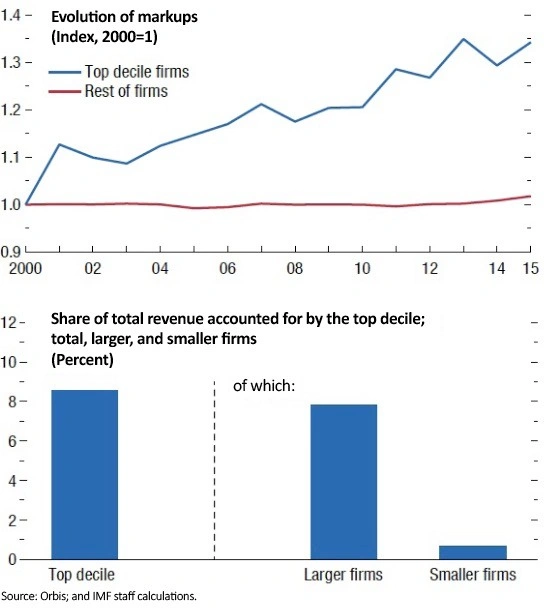

The IMF found that in advanced economies concentration of market power led to average price mark-ups of 8% from 2000 to 2015, with the most pronounced price rises in non-manufacturing industries in the US.

Most of the mark-ups were generated by a small number of large firms which had higher than average productivity, were ‘more likely to invest in intangible assets such as patents and software’ and gained market share at the expense of firms with low mark-ups and lower productivity.

This would suggest that markets have fundamentally changed since 2000 allowing the most innovative and productive firms, with high levels of intangible assets such as technology, customer databases, technical and managerial skill and network effects, to increase their market share to the point of dominance.

In other words market power isn’t necessarily the result of less competition. Jeffrey Meli, head of research at Barclays, suggests that if anything more open markets have intensified competition which ‘has tilted the playing field, allowing the most productive firms to capture sales from their less efficient rivals’ and forced the least efficient out of the market altogether.

A key aspect of the ‘winner takes most’ narrative is that even small competitive advantages can lead to an increase in market power. New forms of technology, slightly more efficient supply chains and more streamlined processes can all add to a firm’s market power.

WHAT DOES IT MEAN FOR INVESTORS?

For investors who have backed Amazon, Google and Microsoft – firms with seemingly unassailable market power – the returns have been outstanding. However, as concern over the reach of these corporate giants grows among policymakers and regulators, the risks are increasing in tandem (read this discussion about the rise of regulatory scrutiny).

The IMF suggests that ‘with mounting risks of adverse growth and income distribution effects from rising corporate power, policymakers should keep future market competition strong’. It suggests cutting barriers to entry in trade and services and allowing lagging firms to catch up on technology.

It also warns that mergers and acquisitions (M&A) typically result in ‘significantly higher mark-ups’ and that structural reforms are needed to prevent dominant firms from ‘entrenching their positions by erecting barriers to entry’.

All of which sounds like a call for more, not less, supervision of firms with dominant market power and greater scrutiny of M&A deals going forward.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.