Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazinePlanning for a 100-year life

When am I going to die? This question, while slightly morbid, is essential when devising a retirement income plan.

In a recent survey of savers who had entered drawdown – keeping their pension pot invested while taking an income – since April 2015, respondents aged 55 to 59 on average thought they would live for 21 more years.

In fact, according to official projections from the Office for National Statistics (ONS) a healthy 55-year-old man has an

average life expectancy of 85 – meaning those in the 55 to 59 cohort are underestimating life expectancy by up to nine years.

A 55-year-old woman can expect to live a further 33 years on average.

But what is the likelihood of living beyond this point? ONS analysis suggests a 55-year-old man has a one in four probability of reaching 93 and a 6% chance of celebrating their 100th birthday.

The equivalent woman has a 1 in 4 chance of reaching 95 and a 10% chance of celebrating her centenary.

If long-term life expectancy improvements continue, younger generations will become increasingly likely to reach three figures.

So how do you prepare for a 100-year life?

MAKING YOUR PENSION LAST TO AGE 100

The surest way to make your pension last a lifetime is to buy an inflation-protected annuity – an insurance product which pays a guaranteed income for life.

If you’re going to go down this route, shopping around for the best rate – and making sure your provider knows of any health conditions which might impact on your life expectancy – is essential.

However, a combination of poor rates driven by record-low gilt yields – which insurers use to price annuities – and inflexibility has seen sales plummet, with most savers now opting to keep their pension invested through drawdown.

The extent to which a withdrawal strategy in drawdown is sustainable will depend on a number of things including overall investment returns, the timing of those returns and inflation.

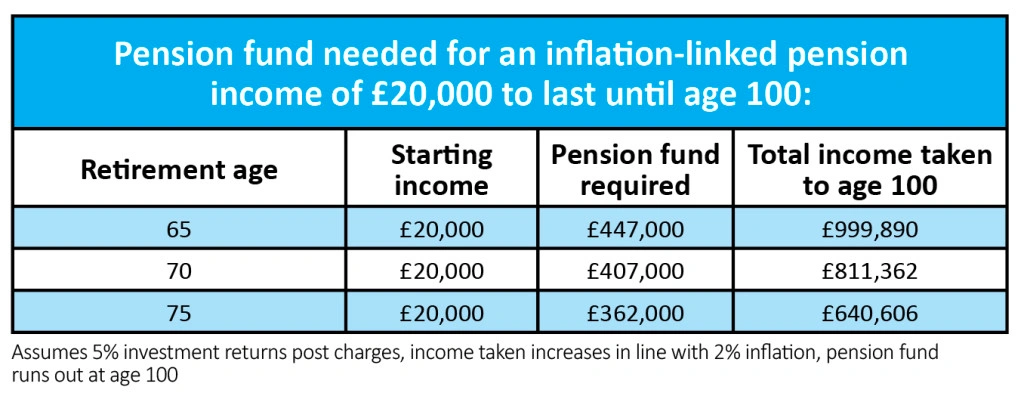

If someone wants to retire today on a UK average salary of £28,000, they can expect around £8,000 from their state pension (based on the flat-rate amount), so will need to be aiming to generate £20,000 from their private pension pot.

If we assume 5% annual investment growth, a 65-year-old would need a pension fund of £447,000 to be able to withdraw £20,000 a year, inflation-linked at 2% a year and still see their pension last until age 100. If growth was lower the pot would need to be bigger.

However, if they delay retirement five years to age 70 the size of pension fund needed to reach age 100 would reduce to £407,000.

SAVING LEVELS REQUIRED

The best way to ensure a comfortable retirement is to start saving early and often. To save the £447,000 required for an average salary in retirement from age 65 to 100, a 25-year-old would need to put away £235 a month.

Delaying by 10 years to start saving at age 35 sees the monthly saving figure almost double to £428 and if you wait until age 45 it is a whopping £859 a month.

If these amounts sound unrealistic it’s still worth saving what you can, making the most of the bonus of pension tax relief and the matched employer contribution through automatic enrolment.

You also need to think carefully about the investment risk you want to take. Younger investors in particular should be able to take more risk than their older counterparts, giving their fund the chance to grow over time. In addition, high charges can have a seriously detrimental impact on your retirement over the long-term, so shopping around is absolutely critical.

If people get this bit right and build a decent pension pot in the first place, it becomes much easier to make that pot last – even over a lengthy retirement.

Five top tips to ensure you don’t run out of money in retirement

1. Set a reasonable income target – 4% of your initial fund value, with income increasing in line with inflation, is a decent starting point for a healthy 65-year-old. You might be able to take more than this if you retire later (or have other income sources), and less if you retire earlier

2. Make a budget and stick to it. This will help ensure you stick to your spending limits during retirement

3. Shop around the market and keep costs as low as possible. This will help ensure your fund isn’t eaten up by unnecessary charges

4. Get all your pensions in one place if you can (but be careful not to lose any valuable guarantees in the process). Savers often lose track of pensions during their lifetime, potentially leaving them facing an income shortfall in retirement

5. Review your funds, provider and withdrawal strategy regularly (at least once a year). If your funds have performed well you might be able to increase your withdrawals. Equally, if they’ve struggled you might need to think about cutting back your income

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.