Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy you should NOT hitch a lift with the Uber IPO

It is one of the most eagerly awaited stock market listings ever but investors are already being warned off investing in the initial public offering (IPO) of ride-hailing colossus Uber.

‘This is one public offering investors should stay away from,’ says Ben Barringer, equity research analyst at investment manager Quilter Cheviot.

Uber unveiled its IPO prospectus last week including plans to potentially raise up to $10bn. That would imply a $90bn to $100bn price tag on the business making it the eighth biggest US IPO ever.

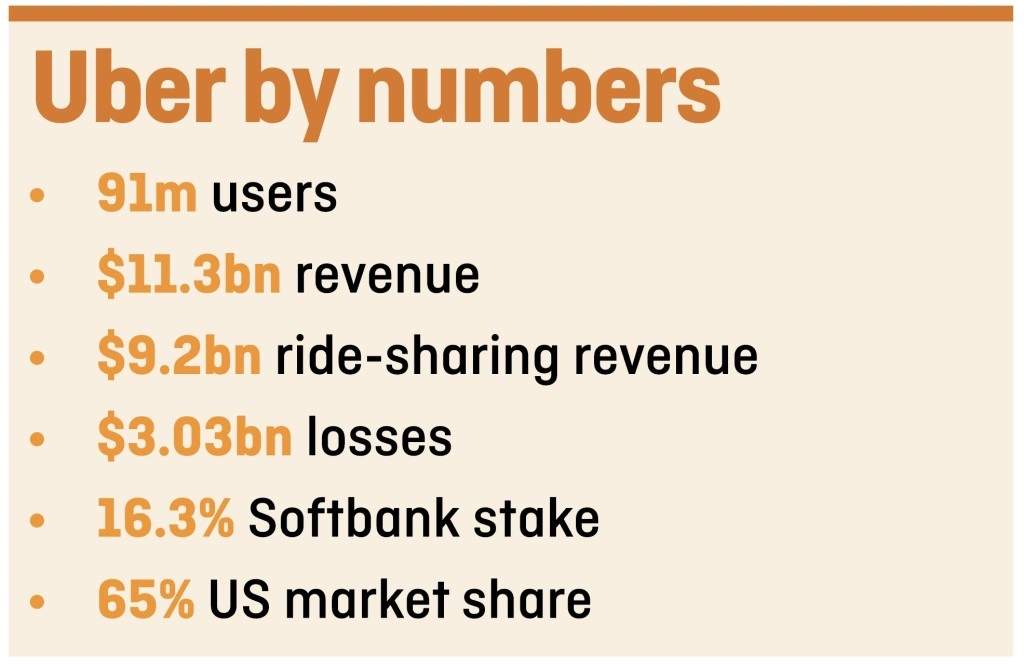

But sceptics have been quick to dig beneath the IPO fanfare and home in on the company’s slowing growth and startling admission that it may never make a profit. Last year saw the previously secretive Uber run up a $3.03bn loss from operations and ate through $2.1bn of cash from revenue of $11.3bn. Revenue was up 42% on 2017 but showed a sharp slowdown on the 106% hike in the previous year.

Uber published its IPO prospectus just two weeks after US ride-sharing rival Lyft became the first online taxi firm to go public on Nasdaq. While global operator Uber is vastly larger than US-only Lyft, the dismal start of Lyft’s stock does not augur well. Lyft’s shares have slumped 22% from their $72 debut.

Operators like Uber and Lyft can benefit from the network effect, a virtuous circle where more consumers using these services attract more drivers to serve them, which attracts more ride-sharing users.

But fierce competition limits their ability to raise prices while drivers are putting the pressure on over pay rates, and can just switch to a rival app if they are not satisfied. The gig economy is also coming under increasing scrutiny from regulators, giving Uber and its rivals even less room to manoeuvre.

Expansion into new areas such as food delivery (Uber Eats) and goods shipments (Uber Freight) are also competitive markets.

In Uber’s favour are large stakes in several overseas rivals in territories where it has chosen to abandon its own operations, such as Yandex in Russia (38%), Didi Chuxing in China (15.4%) and Grab (23.2%) across parts of south- east Asia.

The future of Uber, and the ride-sharing economy, is increasingly banking on self-driving technology, which would allow operators to phase out their largest costs; drivers. While much of the technology already exists, the legal framework and consumer appetite remains years away because of ongoing safety concerns.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.