Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat a blockbuster US deal can tell us about the oil price

On 12 April US oil company Chevron made a $33bn swoop for Anadarko. As well as heralding a possible wave of mergers and acquisitions in the energy sector, the prospective deal also provides some insight into how the industry (or at least Chevron’s board) are currently viewing the oil price.

Chevron is paying a 39% premium for Anadarko based on its closing price before the transaction was announced. This generous offer could reflect the complementary nature of Anadarko’s portfolio, which like Chevron’s includes material exposure to US shale alongside global deepwater exploration and liquefied natural gas.

However, broker Cantor Fitzgerald says the promised synergies from the deal could ‘rapidly disappear’ if the oil price was to retreat back to $50 per barrel.

It comments: ‘This looks to be a good deal for all parties, albeit at a fairly punchy valuation suggesting that Chevron management are confident that crude prices will hold up – although some may argue Chevron was under pressure to do a deal after losing out on BHP’s (BHP) shale assets to BP (BP.) last year.’

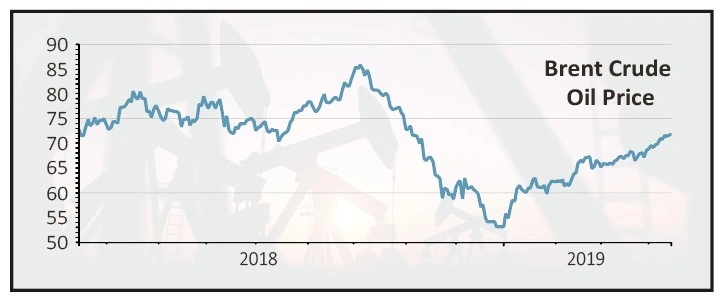

Oil executives are not always the most astute predictors of future movements in oil prices, but Chevron’s board are not alone in expecting crude to enjoy an upwards trajectory.

This is despite oil already moving from around $55 per barrel to more than $70 per barrel so far in 2019 amid looser monetary policy in the US and disruptions to supply from the escalating conflict in Libya.

COULD THERE BE A BIG SPIKE IN OIL PRICES?

The commodities strategy team at Bank of America Merrill Lynch believe the chances of a big spike in oil prices are not being priced in by the market.

‘In short, OPEC+ supply is falling sharply, global oil demand is still healthy and US shale does not have enough time to respond to the rising oil price environment as we head into the summer driving peak,’ they observe.

‘Importantly, global oil consumption is supported by relatively strong consumer sentiment and expansive services PMIs (purchasing

managers’ indices) around the globe, and in spite of falling business sentiment and contracting manufacturing PMIs.’

They note that against this backdrop, inventories of the refined products derived from crude oil in developed economies are relatively light and this also coincides with the looming introduction of new emissions regulations for the shipping industry which could overwhelm demand for fuels with a lower sulphur content.

This creates an interesting backdrop to OPEC’s next meeting on 25 June in Vienna and whether the Saudi Arabian-dominated oil producers’ cartel considers upping output quotas.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.