Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineJD Sports, IWG, Galliford Try and other news

The Easter holidays have seen plenty of news from retailers for investors to keep tabs on. Chiming with a British Retail Consortium report which suggested March’s better weather encouraged higher footfall on the high street, most of the updates from the space have been broadly positive.

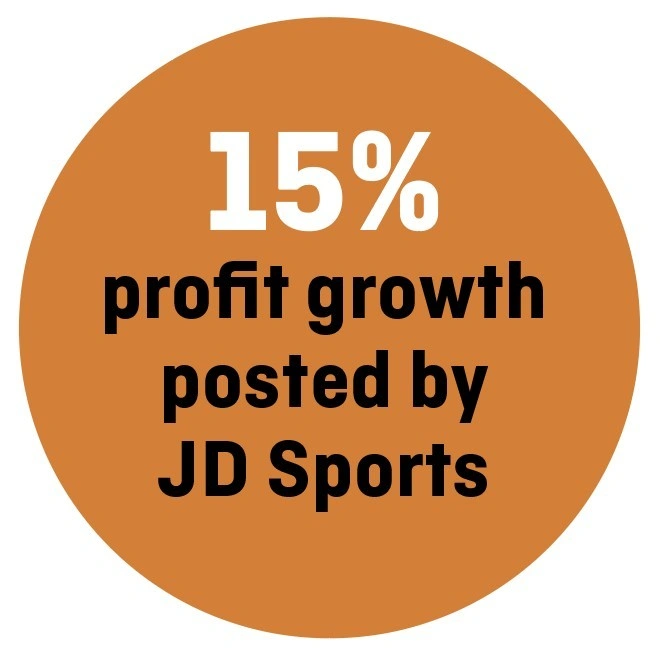

Sector star JD Sports (JD.) delivered yet another solid set of full year results on 16 April. Adjusted pre-tax profit surged 15.5% to £355.2m and positive recent trading was flagged, including in its US Finish Line business acquired in 2018. This helped drive the shares to 12-month highs of 560p.

The company appears to really ‘get’ the people who shop in its stores, tapping into the boom in demand from this youthful demographic for ‘athleisure’ gear which can be worn for everything from gym trips to socialising.

Another retail outfit which really understands its customers is fantasy miniatures and table-top games seller Games Workshop (GAW). The firm behind the Warhammer brand said on 12 April that trading had been good since an update in January, triggering a new rally in the share price.

Newsagent WH Smith (SMWH) also delivered the goods as a strong performance from its Travel division supported a journey to the vicinity of record share price levels above £22 last seen in December 2017.

Travel saw like-for-like sales jump 3% over the period as WH Smith benefited from a captive audience at train stations, airports and motorway service stations.

In other news flexible office space provider IWG (IWG) agreed to sell its Japanese operations to TKP Corporation for £320m with a franchise agreement, sending its shares up by nearly 15%.

Investment bank Berenberg comments: ‘We view this as a very positive step for IWG. While a transaction to this end had been flagged by the company, we were sceptical of IWG’s ability to sell one of its businesses for such a high multiple (15 times earnings compared to a group valuation of seven times) at the same time as shifting to a franchising business model.

‘From here, the question is clearly whether this is a one-off sale of one of the company’s higher quality assets, or indicative of what IWG will be able to achieve across its portfolio.’

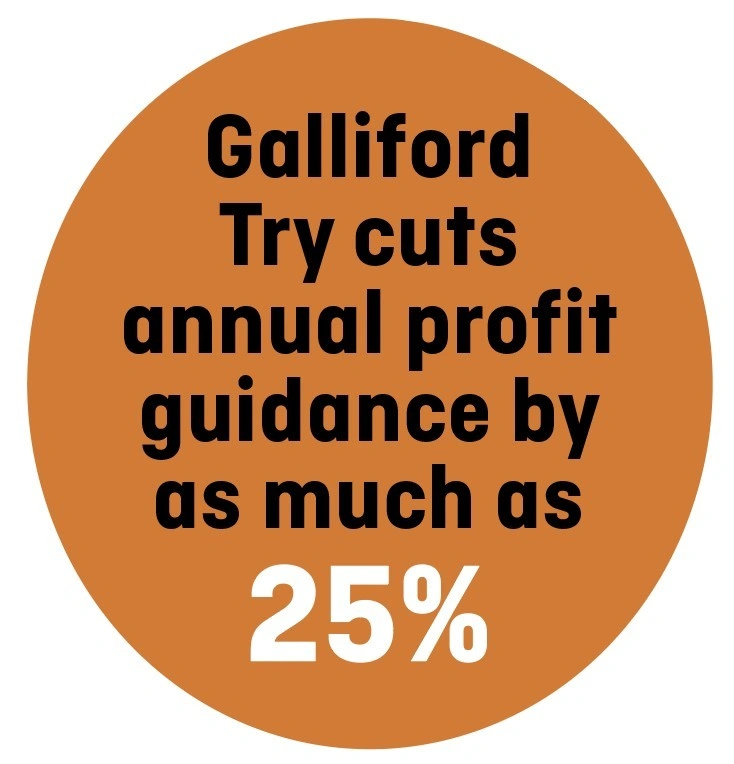

On 16 April Galliford Try (GFRD) saw its shares slump 20% as it issued a profit warning, saying annual profit would be £30m to £40m lower than the forecast £156m as it downsizes its construction arm amid spiralling costs on some projects.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.