Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHigher or lower: how to play the volatile pound

‘It’s tough to make predictions, especially about the future,’ as they say. Variations of this quotation have previously been attributed to physicist Nils Bohr, writer Mark Twain, movie mogul Sam Goldwyn and baseball player Yogi Berra, yet the identity of the originator is less important that its implication, which feels very relevant for today’s financial markets.

The swings in the pound neatly encapsulate these volatile times. Since the initial collapse in sterling in response to the outcome of the Brexit referendum in June 2016 it has been a roller-coaster ride.

‘Cable’, the market nickname for the pound/dollar exchange rate, was close to par value in August 2017 at $1.08, the lowest since as far back as Reuters Eikon data goes (1989).

The most recent rally in sterling through March has now been curtailed by the latest ‘Brextension’, which again kicks the decision can down the road, probably until October.

UK businesses and investors are left wondering what to do and how to plan amid this prolonged uncertainty.

STERLING CONUNDRUM

The obvious, if simplistic way to square this circle is through tracker funds, using FTSE 100 or FTSE 250 indices as hedges against weaker or stronger sterling swings ahead.

Many investors grasp the idea of the FTSE 100 as a sort of instant UK diversifier. That thinking is based on upwards of 70% of earnings imported from overseas. The FTSE 250 is also not quite the domestically-facing index it is often cracked up to be, with about half of its earnings coming from abroad.

Concentrating on earnings and where they come from is an alternative hedging idea posited by Liberum analysts Andrew Coury and Mark James.

‘UK stocks remain cheap versus historical levels,’ they say, having run the price to earnings (PE) numbers. According to their calculations, based on Datastream data, the FTSE 100 sits on a PE multiple of 13.5, a modest discount to the FTSE 250’s 13.7, both below medium range averages of between 15 and 16-times.

Dividend yields back up the view that UK stock markets remain inexpensive, the FTSE 100’s close to 10 year highs at 4.7%.

A BETTER WAY

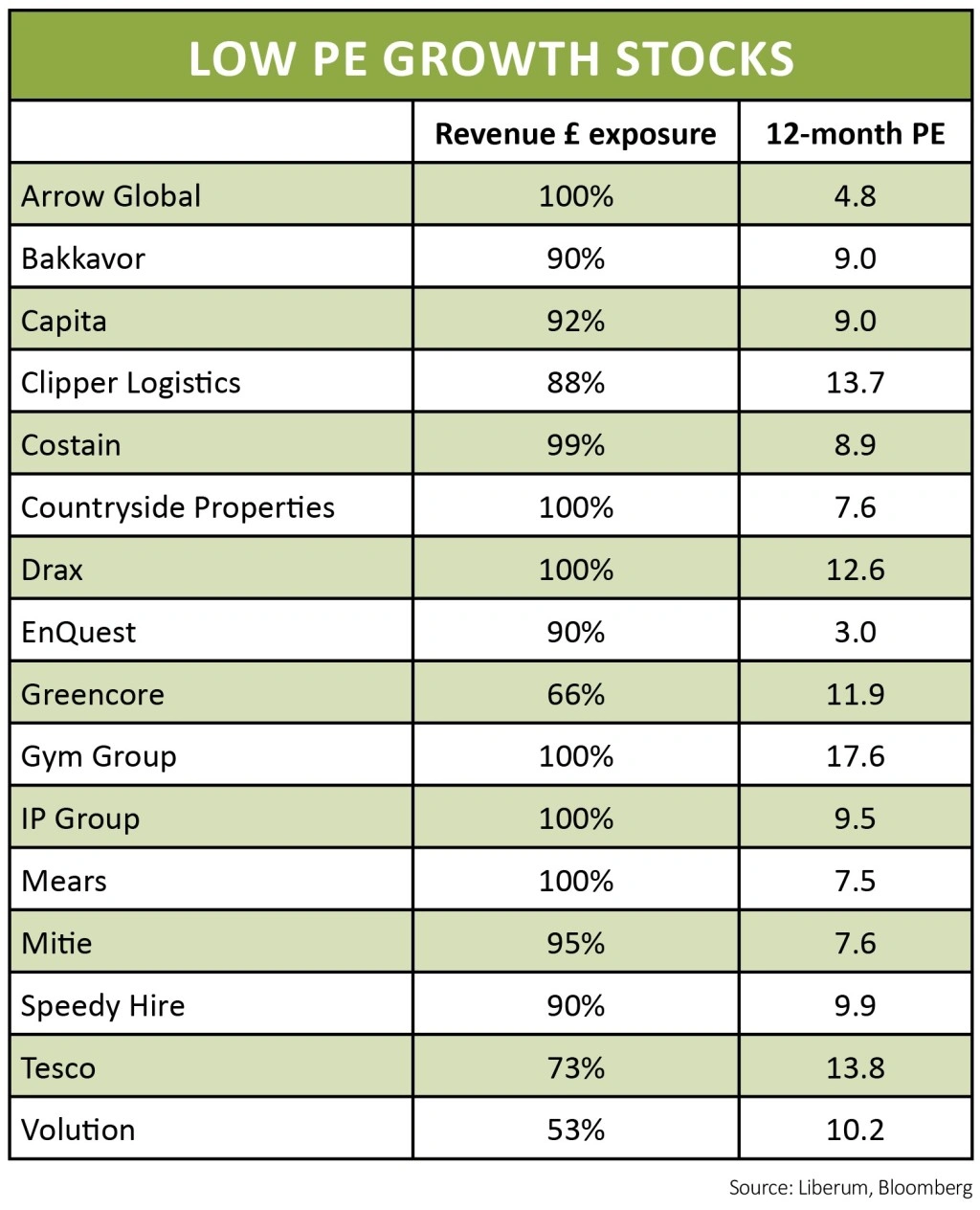

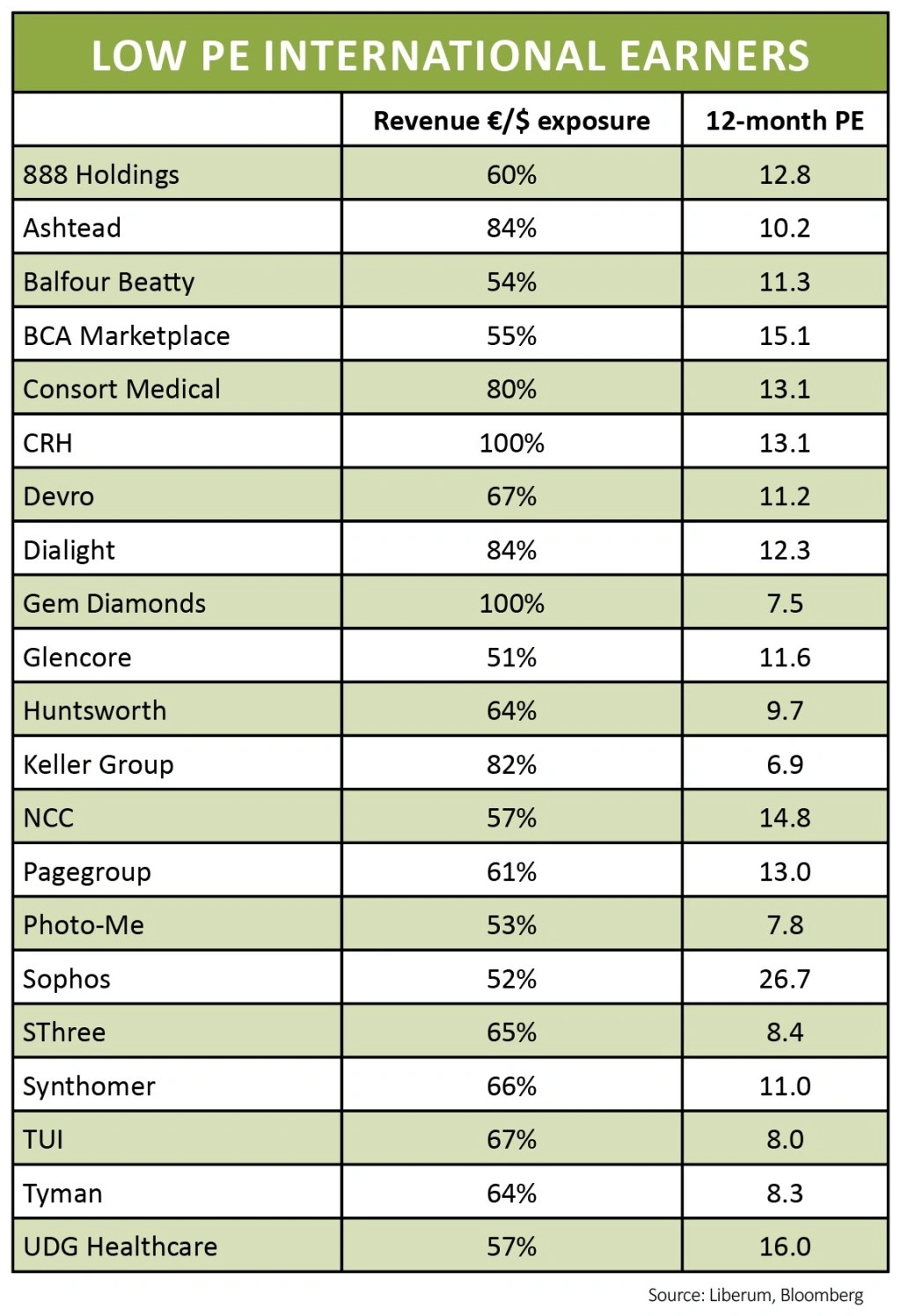

Coury and James ran the numbers across the FTSE 350 universe on the basis of two different scenarios. First, they looked for domestically focused businesses most likely to perform well if there is a rally in sterling. They then screened for stocks with large international earnings that could be bolstered by further plunges in the pound.

The searches were refined further by demanding that stocks featured would be inexpensive, financially robust and expected to grow.

To ensure this that set criteria that demanded a minimum of 3% expected earnings growth, a net debt to EBITDA (earnings before interest, tax, depreciations and amortisation) multiple no higher than two-times, plus a current 12-month forward PE discount of at least 10% versus their five-year average.

Some of the qualifying stocks remain firm buys in the eyes of Liberum. Recruiter SThree (STHR), diamond miner Gem Diamonds (GEMD) and power plant supplier Ashtead (AHT) are among the international earners favoured.

From the UK domestics list, supermarket leader Tesco (TSCO) has been performing well lately, while Liberum sees further share price upside at low-cost gyms operator Gym Group (GYM) and Volution (FAN), the ventilation equipment manufacturer.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.