Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBehind the screen with Ocean Outdoor

Sci-fi fans may remember the early noughties release Minority Report. One of the elements of the imagined world of the film was personalised advertising with digital billboards responding to the individuals passing them at that moment.

This scenario no longer belongs to the world of science fiction. Digital outdoor advertising specialist Ocean Outdoor (OOUT) has developed vehicle detection technology which will trigger a relevant message to be deployed when a specific audience is in front of the screen.

MORE THAN JUST A BILLBOARD

A BMW driver, for example, might expect to see a marketing message linked to that brand as they drove past, while the company’s facial detection technology can serve advertisements to consumers based on gender, age, even down to markers such as eye wear and mood.

The £325m market cap, and the wider outdoor or out-of-home (OOH) advertising industry, have clearly moved a long way from a guy with a ladder pasting a poster to a wall.

More than 90% of Ocean Outdoor’s business is digital. Having formed in 2004, two years later the company secured a screen at the IMAX cinema in London’s Waterloo and now has a contract for the two Westfield shopping centres in the capital as well as other iconic locations across the UK. Many of us will probably have glanced at one of its screens.

The firm was acquired by listed investment fund Ocelot Partners in March 2018, which subsequently renamed itself as Ocean Outdoor. The shares emerged from a long suspension in January 2019 to resume their listing on the London Stock Exchange’s Main Market.

Ocelot ostensibly bought the business as a vehicle to make acquisitions in the sector. In June 2018 the company bought Scotland’s leading OOH play Forrest Media and Netherlands OOH outfits Ngage Media and Interbest were snapped up in March 2019.

It is currently number four in the UK market behind JCDecaux, Global and Clear Channel but is a leading player in digital OOH.

THE MODEL

So how exactly does the company make its money? Ocean Outdoor’s chief operating officer and chief financial officer Stephen Joseph explains the model is ‘one half property development and operations with the other half selling and marketing the advertising space’.

In effect, the property side locate and secure sites in attractive locations. Sometimes Ocean Outdoor will own the screen and on other occasions, notably at Westfield, the screen is built by Ocean’s effective landlord as part of a development or redevelopment of a site.

Ocean then pays rent or a share of profit to the owner of the relevant site, which could be a corporate entity or a local council.

Retaining the contracts for these sites is crucial to the business and losing a location such as Westfield could be highly damaging.

While the company does not disclose specific renewal dates chief executive Tim Bleakley points out to Shares that contracts typically have a duration of between seven and 10 years and that its key locations have more than five years left to run. Renewal rates have also historically been robust.

With the locations secured, the sales and marketing side then sells the inventory. This could be an arrangement covering a couple of weeks, a day, an hour or can even be sold by impression.

A PROFITABLE BUSINESS

Full year results for 2018 announced last month showed how this model feeds into the company’s numbers. Billings, i.e. the money it is paid by advertisers, were up 13.7%

year-on-year to £87.8m. Revenue, or how much of this Ocean gets to keep, was up 15.2% to £62.2m.

Earnings before interest, tax, depreciation and amortisation (EBITDA) ticked up 4.7% to £20m with the EBITDA margin coming in at 32.2%. Operating cash flow totalled £17.9m and the company announced a $25m share buyback.

Most of Ocean Outdoor’s inventory is bought on behalf of clients by big media agencies in the same way as TV advertising space, for example. Around 10% is sold directly, typically to smaller, regional advertisers.

The digital nature of its outdoor assets means its inventory is compatible with programmatic or automated buying of ads, as is the case with online advertising.

And Bleakley notes that one of the advantages outdoor advertising has over web-based adverts is that the risk of a company’s brands being presented alongside extreme content is mitigated.

WHAT ARE THE MAIN RISKS?

Like any advertising business, the company is sensitive to what is happening in the economy. However, the group could continue to do well if digital OOH takes a greater share of the overall advertising dollar.

Bleakley says the strategy remains centred on three tenets, namely organic growth, continued investment in technology and acquisitions – with £160.5m on the balance sheet still to deploy as at the

end of 2018.

The focus on M&A is another risk for prospective investors to weigh as the company could buy the wrong businesses, and whatever it acquires, the digital focus is likely to be diluted in the short-term with most operators in this market having a heavier bias to traditional OOH.

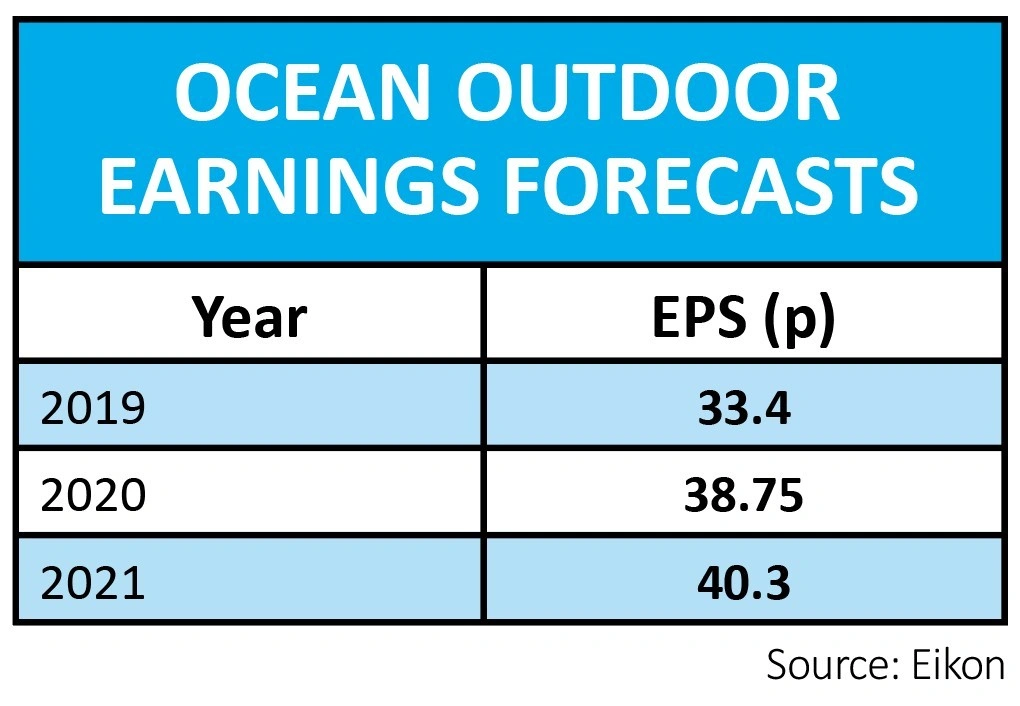

SHARES SAYS: We think this is an interesting story and trading at $7.80 the shares do not look overly expensive, particularly when you factor in the cash on the balance sheet. Based on Numis’ forecasts the shares trade on an EV (enterprise value)/EBITDA ratio of 6.9-times against an average according to SharePad of 10.6 times for the wider media sector.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.