Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat happens when you buy a share

While potential investors are often focused on what they should invest in, they can overlook a vital aspect: how do I actually buy a share?

Anyone looking to make their own investment should open a dealing account, ISA or SIPP (self-invested personal pension) through an investment platform or a stockbroker.

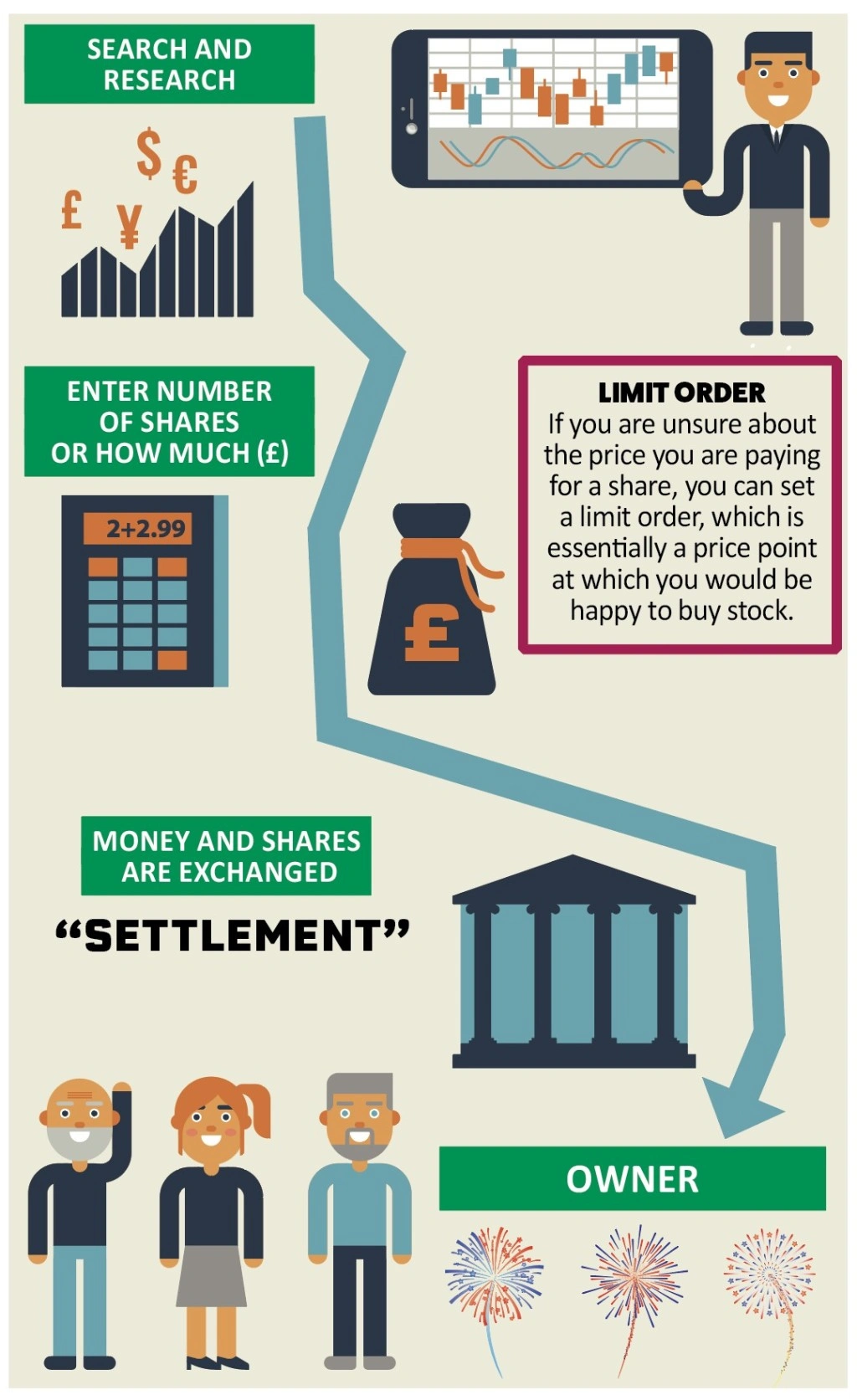

HOW DO I BUY A SHARE?

Once you have opened an account, you can search for the company, investment trust or exchange-traded fund you are interested in. The same process would apply to investing in unit trusts and OEIC funds.

Before dealing, you should be able to find essential information on your investment platform such as a company’s financial and dividend history, details of an investment trust’s holdings or the index being tracked by an ETF. You can also find this information and more from financial websites such as Morningstar and Shares own website.

To buy a share, you either enter the number of shares you want or the monetary amount you would like to spend. The latter option will figure out how many shares you can buy at the current price. You should be able to specify whether you want dealing charges included or excluded as part of this figure.

There is no recommended amount of shares you should buy in a company, although you should bear in mind the dealing costs you can incur. It would not make sense to buy one share costing 500p, for example, as you could pay twice that amount as a transaction fee.

It is important to understand the distinction between the bid and offer price. The former is the price you’ll achieve if you sell (i.e. what a market maker will bid for your shares), the latter represents the purchase price (i.e. the price that a market maker will offer you). We will discuss the bid and offer prices and the typical spread between them in a future article.

BUYING WITH A DELAY

If you are unsure about the price you are paying for a share, you can set a limit order, which is essentially a price point at which you would be happy to buy stock.

For example, if Company X is currently priced at 100p and you wanted to buy at a cheaper price, you can specify 90p as your limit. Should the shares hit this price, an instruction is automatically sent to buy the stock at the best available price.

There is a catch as limit orders are often only valid for a short period, such as up to 90 days, so you may need to put through another order if it does not go through during this period.

Once you have entered all the information on a normal trade, you will be presented with a countdown. This is a quote for a price that is only guaranteed for 15 seconds due to the fast-moving nature of the market.

If the quote expires, you need to request another, which could be higher or lower than the previous price offered.

WHEN WILL I OWN THE SHARES?

AJ Bell’s head of operations Mark Gillan explains what happens when you have committed to a trade.

‘After you have entered your order, the money and shares need to be exchanged in the marketplace. This process is known as “settlement”,’ he says.

‘Settlement takes a number of days, depending on the type of investment – for standard shares, settlement takes two working days, but for investment funds, settlement can take three working days or more.’

As Gillan explains, the date you enter your order is known as the ‘trade date’, and the date that the money and shares change hands is known as ‘settlement date’. The difference between these dates is often known as the ‘settlement cycle’.

You will often see abbreviations such as ‘T+1’ and ‘T+2’ used – this refers to the days between trade and settlement date (for example, T+1 means the trade will settle on the first working day after trade date).

On settlement date, you will become the beneficial owner of the shares. This is also the day that you become a shareholder of record and therefore entitled to any dividends.

HOW YOU HOLD YOUR SHARES

There are three possible options in terms of how you hold your shares: you can take them in the form of paper certificates; use your broker’s nominee account to create an electronic record in Crest (the UK’s central depository for non-paper based shareholding) or have your own Crest account which is known as Crest personal membership.

The choice you make can have a bearing on how you receive information about your investments. This is because if you have your own Crest account or share certificate your name will be on the share register of the company you’re invested in. Nominee accounts instead see the broker’s name entered on the register.

Most of us will see our shares held in the name of their platform’s nominee company, where they are ringfenced and should be protected from creditors if your broker or investment platform was to go bust.

Nominee account holders will have to go through their investment platform if they want to vote at or attend an EGM or AGM.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Could Unilever turn the tables on Kraft Heinz?

- Doubts raised on OneSavings Bank and Charter Court merger

- Superdry, Kier, Domino’s and other news

- What Norway’s oil investment U-turn means for UK investors

- Raft of negative economic data fuels global growth concerns

- Airline sector gets tough on shareholders to keep flying post-Brexit