Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWatch out! Avoid these 10 ISA mistakes now

There are many reasons to use an ISA for saving and investing but it can be easy to overlook various benefits that come with the tax-efficient wrapper or making inefficient decisions with how you manage your money. This article explains 10 ISA mistakes to avoid so you make better financial decisions in the future.

1 – Forgetting to use your whole family’s allowances

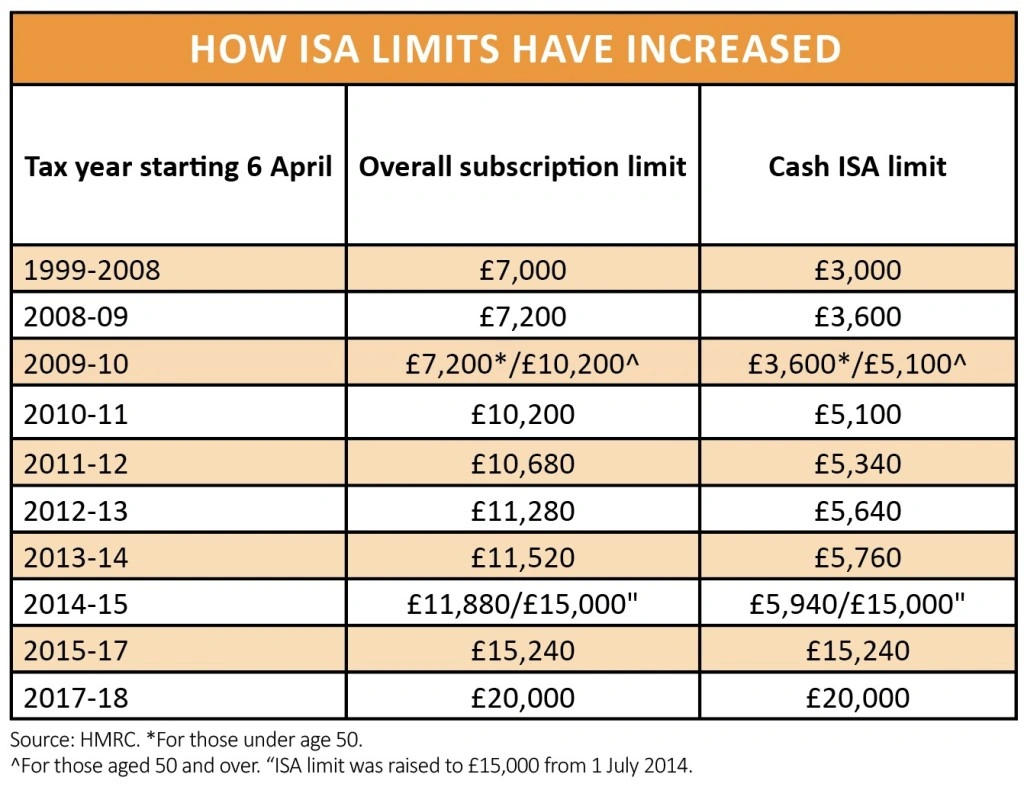

ISA allowances have grown dramatically in recent years, and now every adult has a £20,000 annual limit. But don’t just think of your limit, remember that your spouse or partner gets that same £20,000 limit too. Children get a smaller limit for their Junior ISA, but you can put £4,260 in per child (this will increase to £4,368 from 6 April 2019).

However, there is a great trick that many parents don’t realise – you can get an adult ISA allowance once a child reaches 16. This means that when your child turns 16 you can pay in £20,000 as well as the Junior ISA allowance of £4,260. This continues until they turn 18, when they are no longer eligible for the Junior ISA.

2 – Don’t pay into more than one of the same type of ISA in a year

You’re only allowed to pay into one of each type of ISA each tax year, so make sure you don’t fall foul of the rules. This means that you can pay into a cash ISA and a stocks and shares ISA in one year, but not into two different cash ISAs. It’s tricky though, as you’re allowed to have more than one open, you just can’t pay into two in the same tax year.

If you accidentally pay into more than one in a year, don’t attempt to fix it yourself, as you may close the wrong ISA. Instead, call HMRC’s ISA helpline on 0300 200 3300 to get advice on what to do. There is a similar process if you accidentally paid too much into an ISA (so more than £20,000 for an adult ISA, for example). HMRC will work out which ISA had the payment into it that breached the limit and will reclaim the money (including charging you for any tax owed).

3 – Not putting your income-paying investments in first

The amount of dividend income you could receive tax-free was slashed from £5,000 to £2,000 last April. Any dividend income you get above this amount is taxed at 7.5% for a basic-rate taxpayer, 32.5% for a higher-rate taxpayer or 38.1% for additional-rate taxpayers.

As the tax year ends people should make sure they put as much of their dividend-producing assets in their ISA as possible to avoid getting walloped with a tax bill. In pounds and pence, someone who receives £5,000 in dividends would previously have paid no tax but this year they will be hit with a tax bill of £225 if they are a basic-rate taxpayer, £975 for a higher-rate taxpayer and a whopping £1,143 for an additional-rate taxpayer.

Assuming a 4% income on your investments, anyone who has more than £50,000 invested in dividend-producing assets outside an ISA is likely to be hit by this cut. However, if you have this money in an ISA you won’t be taxed a penny of income tax on this pot.

An investment pot of £100,000 that is yielding around 4% means that the investor will save £150 a year in income tax if they are a basic-rate taxpayer, £650 a year if they are a higher-rate taxpayer and £762 a year if they are an additional-rate taxpayer if this money was in an ISA rather than a normal investment account.

4 – Staying in cash for a long period, for fear of investing

Around 72% of ISA money is in cash, likely earning measly interest rates. Holding cash is smart, if it’s to meet short-term spending needs, as an emergency pot and if you want a low-risk investment. But if you’re willing to dip your toe into the investment markets you could potentially make more money over the long term.

Inflation is currently around 2%, which means you need to make at least 2% on your cash ISA account in order to just keep up with rising prices – and the top easy-access cash ISA account only pays 1.5% at present.

The difference between cash and investment returns adds up over the longer term. Studies of long-term stock market returns show that they average around 5.5%, after inflation, so around 7.5% at the current rate of inflation.

On a £10,000 ISA pot, after 10 years the investment would have grown to £18,771, assuming 7.5% annual return and 1% charges. In that same period the cash account with a £10,000 initial investment would have been turned into £11,605. After 20 years the difference between the two pots would be £21,768.

5 – Thinking too short term

Too often when savers are filling their ISA allowance they think about what is doing well in investment markets now, rather than what will perform well over the long term. Rather than thinking about what assets did well in the past year, think about getting a good spread of investments across different countries and asset classes.

If you’re investing you should be locking money away for at least five years, so think about markets that will do well over the period you’re investing, not just in the next six months.

6 – Forgetting to use Bed & ISA, or Bed & Spouse

Strange name, but a useful tax-planning strategy. Bed & ISA effectively means selling investments that are outside your ISA and rebuying them within the ISA. It means you can use your capital gains tax allowance in a year, which is currently £11,700, and lock your investments into an ISA, where you won’t be charged income tax or capital gains tax.

If you’ve got some investments that have gone up in value a lot, and so have a big capital gain, you can sell enough to realise £11,700 of gains and then rebuy them within an ISA. You won’t be charged tax on the gain, as it’s within your annual allowance, and you protect the investment from future tax.

You can do a similar move but transfer the asset to your spouse instead, who can then put it in their ISA. Just make sure you don’t leave it until the last minute, as it can take a bit longer to execute this move – not one for 11:30pm on 5 April, half an hour before the new tax year begins.

7 – Not using free Government bonuses

With the Lifetime ISA you can get up to £1,000 a year in Government bonus, up until the age of 50. If you opened a Lifetime ISA at age 18, that is a maximum Government bonus of £32,000 (or £33,000 if you’re lucky enough to have your 18th birthday before 6 April).

The Lifetime ISA is open to those aged 18 up to your 40th birthday, and you can save up to £4,000 each year – either in one or more lump sums or as a regular monthly saving. From the age of 50 you no longer get the Government bonus but you can carry on paying into the account. You can withdraw Lifetime ISA money once you’ve reached age 60 or to buy your first property, but be warned that if you take the money for any other reason (excluding terminal illness) you’ll pay a 25% exit penalty.

8 – Failing to reinvest your income

Dividends on investments in ISAs can be withdrawn with no tax liability, but if you don’t need the income, reinvesting them to buy more shares in the same investment can have a dramatic impact on the size of your ISA. This is because when you buy more shares each time you receive a dividend, you then receive more dividends next time there is a payout, which can then be reinvested again and so on.

Let’s take the example of someone investing the full ISA allowance of £20,000 and assuming the FTSE All-Share’s long-term averages of a compound annual growth rate of 5.5% and annual dividend yield of 3.5%.

After subtracting 1% a year for platform administration and fund fees, the initial £20,000 will be worth £47,729 after 20 years. You would have also banked £21,834 in cash dividends to give a total return of £69,563. However, an investor who reinvests the dividends rather than banking them would have £91,678 – more than £22,000 extra.

9 – Forgetting about charges

There can be a wide disparity between the charges levied by investment platforms and asset managers. The differences can appear small in percentage terms but over a long period can have a significant impact. Higher charges are not necessarily bad if they are for a service or investment you value highly, but make sure charges are not eating into your investment returns unnecessarily.

For example, the UK regulator recently said that investment platform fees range from 0.22% to 0.54%. The cheapest active fund in the UK All Companies sector is 7IM UK Equity Value (BWBSHS3) with an ongoing charges figure of 0.35% and the most expensive in the sector is Candriam Equities L UK (QG69) at 2.34%.

Holding the cheapest UK All Companies fund on the cheapest fund platform could cost 0.57% a year, whereas holding the most expensive fund on the most expensive platform could cost 2.88%.

Assuming a gross investment return of 6% a year, on a £20,000 ISA investment, the difference in fund value after 20 years would be a whopping £20,612 (£36,973 compared to £57,586).

10 – Being scared by Brexit or market moves

This year’s ISA season comes at a tricky time – the outcome of Brexit is not yet known, there’s nervousness about ongoing trade wars between the US and China, and worries about the rate at which Europe is growing. All this is making investors nervous.

Since the Brexit vote almost three years ago UK investors have pulled more than £11bn of money from funds focused on the UK stock market, according to the Investment Association. What’s more, in December last year investors withdrew a total of £1.65bn from funds in that month alone. Equity funds saw their highest outflows in more than two years, as investors pulled £875m, with every major equity market seeing outflows.

In this environment it’s easy to be nervous and just stay in cash for a long time, rather than making a decision about where to invest. But this is where you need to go back to the investment basics of thinking about the time period you’re investing over, how much risk you’re willing to take and building a diversified portfolio. It’s notoriously hard to time markets correctly, so instead drip feed money into markets and invest in more defensive assets if you’re cautious.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Could Unilever turn the tables on Kraft Heinz?

- Doubts raised on OneSavings Bank and Charter Court merger

- Superdry, Kier, Domino’s and other news

- What Norway’s oil investment U-turn means for UK investors

- Raft of negative economic data fuels global growth concerns

- Airline sector gets tough on shareholders to keep flying post-Brexit