Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThis investment trust is pinning its hopes on a banking sector rebound

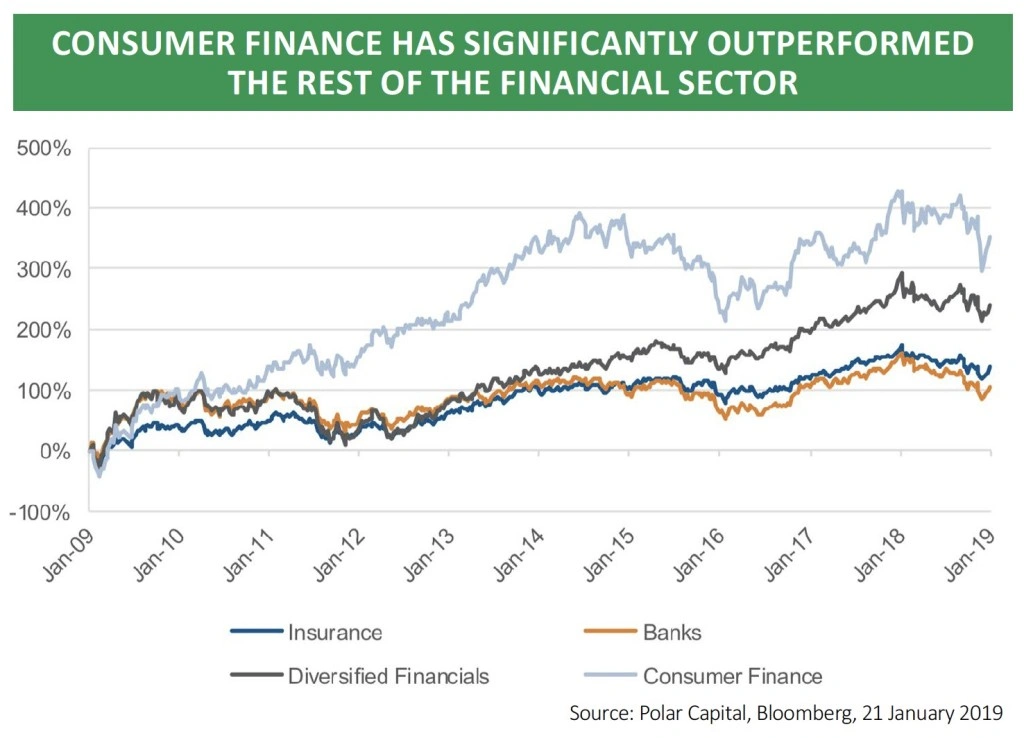

It’s been 10 years since shares started to recover from the global financial crisis-induced market collapse. However, there are pockets of the market still trying to play catch-up including financial stocks like banks which remain ‘unloved, under-owned and misunderstood’, say John Yakas and Nick Brind, managers of investment trust Polar Capital Global Financials (PCFT).

They believe the financial sector offers a buying opportunity for the coming decade. In their opinion, financials are beneficiaries of rising interest rates (which widen their margins), the potential for accelerated loan growth, their balance sheets are strong, emerging markets and fintech are creating opportunities, and stock valuations are low.

POPULAR WITH INCOME SEEKERS

Most investors have historically been drawn to the banking sector for its generous dividends. The shareholder rewards disappeared in the middle of the global financial crisis but dividends now appear to be back on the menu. Sadly a lot of banking stocks are still struggling to deliver decent capital gains as many investors remain cautious towards the broader sector.

Launched in summer 2013, Polar Capital Global Financials Trust has yet to prove its worth as a better vehicle for investors than buying a passive fund tracking a global financial sector index.

Its net asset value total return since launch has been 62.2% which is exactly the same as its benchmark, the MSCI World Financials index (including some adjustments for the real estate sector which used to be part of that index until August 2016).

However, on a share price total return basis the investment trust has lagged its benchmark by a considerable margin, only delivery 46.7% total return since inception. The shares currently trade on a 5.5% discount to net asset value.

‘The trust was launched as a way to play the sector at a point when people had very little confidence in it,’ recounts Yakas. ‘We’re all about risk-adjusted returns. Our aim is to have a relatively quality bias, slightly more cautious vehicle. We also capitalise on the income streams.’

US BIAS

The fund manager says it is a global financials fund with 40% to 50% of investments in the US because that region is home to so many sector constituents.

‘The other thing about financials is you are naturally biased towards banks and they, alongside non-life insurance, are probably Polar Capital’s two specialisms. Ultimately you have to be quite positive on banks if you want to buy the trust.’

In addition to banking the investment trust seeks to generate a growing dividend and capital appreciation via stakes in insurers, property plays, asset managers, specialty lenders and fintech firms.

Its portfolio includes a position in banking group JPMorgan Chase, described by Yakas as the winner of the financial crisis because all of its businesses are performing ‘extremely well’ and it has gained market share.

Other names in the portfolio include banks Wells Fargo, Citigroup, Bank of America, insurance and reinsurance group Chubb and Japanese lender Sumitomo Mitsui Financial.

IS IT DIFFERENT THIS TIME?

Fears of a repeat of the global financial crisis currently weigh on investor sentiment towards financial stocks. However, Yakas insists a lot has changed over the past 10 years.

He stresses that banks’ balance sheets look very different to what they did 10 years ago because the regulators have clamped down on the sector.

‘Our view generally is that you have better quality balance sheets, more capital, better funding structures in place and the fact that you haven’t had much loan demand, you haven’t had that build up in gearing on bank balance sheets.’

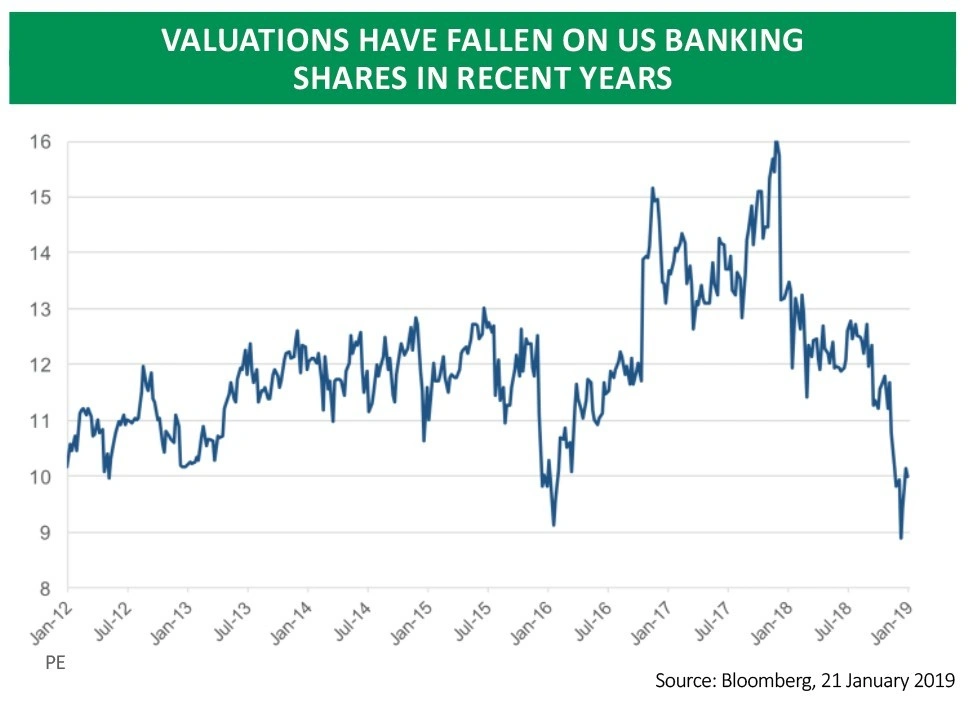

Firmly outside of the camp arguing banks have become over-regulated and thus utility-like, Yakas says it is possible to buy cheap, attractively priced, great income stream banks as well as access to a market undergoing structural change driven by technology which is altering the whole cost structure.

CORPORATE ACTIVITY IS HEATING UP

Other dynamics which could drive higher returns for financial stocks include mergers and acquisitions. In February BB&T announced plans to buy SunTrust Bank, representing the biggest US bank deal in a decade. Yakas believes this deal could put pressure on other regional banks to consider their own mergers.

‘The US has got 5,000 banks. Because of the financial crisis, the Federal Reserve essentially put a stop to big bank mergers because banks had become so big. There was a lot of fear about “too big to fail” etc. I don’t think the regulator in the US will allow someone like JPMorgan to buy a big bank, but further down the list you’ve suddenly seen the thing open up. We invest quite locally in the US, where there are still loads of tiny little banks.’

In the UK, the Polar Capital trust has stakes in both OneSavingsBank (OSB) and Charter Court Financial Services (CCFS) which are in talks over a £1.6bn merger.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Could Unilever turn the tables on Kraft Heinz?

- Doubts raised on OneSavings Bank and Charter Court merger

- Superdry, Kier, Domino’s and other news

- What Norway’s oil investment U-turn means for UK investors

- Raft of negative economic data fuels global growth concerns

- Airline sector gets tough on shareholders to keep flying post-Brexit