Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine‘Can you help me understand the state pension age changes?’

Trevor says:

I’m a bit confused about the state pension. I’ve seen some stories saying it is now 65 and three months – does that mean it won’t be increasing to 66?

Tom Selby, AJ Bell senior analyst says:

Unfortunately no, but it’s not surprising the approach the Government has taken to raising the state pension age has caused a little confusion.

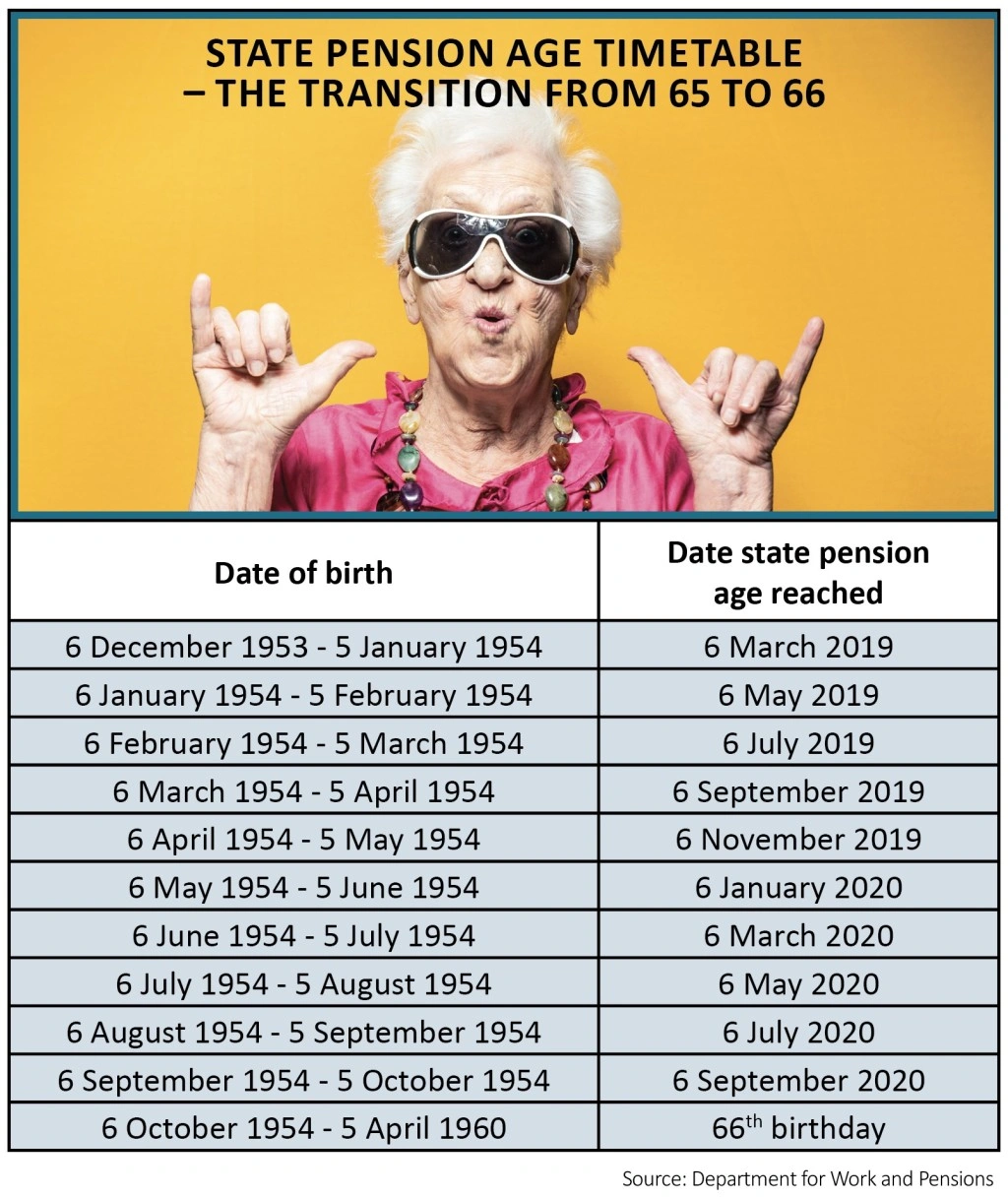

The increase to age 66 is being phased in until October 2020, meaning people reaching their 65th birthday before that date will receive their state pension at different ages. The timetable in this article shows you exactly how it works.

Those first affected were born between 6 December 1953 and 5 January 1954. This group of people had to wait up to three months beyond their 65th birthday to receive the state pension on 6 March 2019.

The next cohort with birthdays between 6 January 1954 and 5 February 1954 will then have a state pension age between 65 and three months and 65 and four months. This pattern continues until October 2020, when the shift to a state pension age of 66 for all will be complete.

Beyond this point, there are plans in place to increase the state pension age to 67 by 2028 and 68 by 2039. It is possible this will be reviewed in light of a growing body of evidence suggesting life expectancy improvements have slowed since 2011, although it’s worth remembering these reforms have been a long time coming.

Male life expectancy at birth has risen from 71 in 1980 to 79 today, while male life expectancy at 65 has increased from 13 years in 1980 to 18.5 years today. This shift has pushed up the cost of the state pension to the Exchequer, expected to reach an eye-watering £96bn in 2018/19. You should therefore factor a rising state pension age into your retirement planning.

Increases to the state pension age will have a significant impact on those affected. The amount of state pension to which you are entitled will depend on whether you built up rights under the old system or the new system introduced from April 2016.

If we use the modern flat-rate state pension as an example, those who have to wait an extra three months to receive it will miss out on over £2,000 in income. A full year delay will cost £8,546.20 in today’s prices, while two extra years will leave a hole of £17,000.

If you still want to stop working at 65, you’ll need to either save a bit more in your private pension or spend less in retirement to fill the gap.

DO YOU HAVE A QUESTION ON RETIREMENT ISSUES?

Send an email to editorial@sharesmagazine.co.uk with the words ‘Retirement question’ in the subject line. We’ll do our best to respond in a future edition of Shares.

Please note, we only provide guidance and we do not provide financial advice. If you’re unsure please consult a suitably qualified financial adviser. We cannot comment on individual investment portfolios.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Could Unilever turn the tables on Kraft Heinz?

- Doubts raised on OneSavings Bank and Charter Court merger

- Superdry, Kier, Domino’s and other news

- What Norway’s oil investment U-turn means for UK investors

- Raft of negative economic data fuels global growth concerns

- Airline sector gets tough on shareholders to keep flying post-Brexit