Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat sort of annual return should you expect from the stock market?

At the end of every year the great and the good of financial markets give their forecasts of where the FTSE 100 and other major indices will be in 12 months’ time.

It’s a fruitless exercise because no-one can consistently forecast how much markets are going to gain or lose.

As the legendary baseball player Yogi Berra said, it’s tough to make predictions, especially about the future.

Not only that, if you could reliably predict exactly what markets were going to do you wouldn’t go round telling everyone else.

HOW MUCH CAN YOU AFFORD TO LOSE?

Not to put too fine a point on it, if you invest in the stock market you have to be prepared to take losses from time to time.

If you don’t like risk, you can leave your money in the bank or you can put it in government bonds.

Neither will generate the kind of long-term returns you can get from the stock market but then you aren’t taking any risk. This is what people mean when they refer to the ‘risk-free rate of return’.

GOVERNMENT BONDS ARE THE SAFEST FORM OF INVESTMENT

UK government bonds, also known as gilts after the gilt edges on the original certificates, have the lowest risk as the government is unlikely to default and not pay back its borrowings.

If it can’t pay you back out of its own pocket, it will issue some more gilts and pay you with those.

As long as nobody questions the government’s ability to repay its debts, it can keep rolling them over indefinitely.

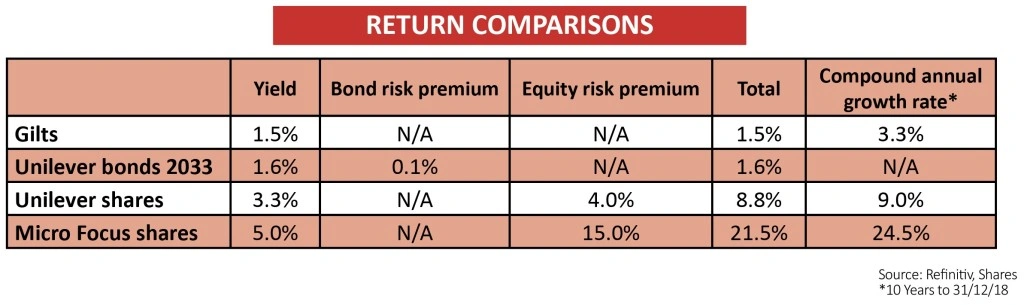

Since the middle of 2016 gilts have yielded between 1% and 1.5% and the current yield on the 15-year gilt is 1.5%, so one can consider this to be our risk-free rate of return.

To invest in anything other than gilts, be it corporate bonds or shares, the returns have to be higher than the risk-free rate. The question is how much higher should the return be to justify the risk?

THE RISK PREMIUM ON SHARES IS HIGHER THAN BONDS

If you buy the corporate bonds of a multi-national company like Unilever (ULVR), there is a small risk that the company might not repay them.

Unilever has the best possible credit rating for a corporate borrower and the outlook is ‘stable’, according to credit agencies, which means it isn’t going to be cut in the near future.

A year ago it issued €800m of bonds with a 15-year maturity and a ‘coupon’ or yield of 1.625%.

That is a very small ‘risk premium’ over gilts but it reflects the fact that making packaged goods is quite a low-risk business and that Unilever has an excellent credit history.

Assuming the bonds never change in price then the yield would stay at 1.625% each year until they expire, which is hardly compelling.

On the other hand Unilever’s shares yield 3.25% and if its

share price stays where it is for 15 years you would get more than double the return on the bonds thanks to compounding. However it is unthinkable that Unilever shares won’t move at all for 15 years.

Therefore, while packaged foods is a fairly low-risk business, investors still have a right to expect a better return than gilts to compensate them for the risk of buying shares.

In the case of Unilever the risk premium doesn’t need to be huge and is likely to be in line with the premium on similar companies such as Proctor & Gamble.

A reasonable guess would be 3% to 4% over the ‘risk-free rate’ so investors ought to think of Unilever in terms of its ability to deliver say a 5% annual return plus dividends of 3% to 4%.

In fact over the 10 years to 31 December 2018 Unilever’s share price had risen at a compound annual growth rate (CAGR) of 9% on average, which is in line with our thinking.

EQUITY RISK DEPENDS ON THE BUSINESS RISK

At the other end of the spectrum is high-growth software business Micro Focus (MCRO) which it could be argued is much riskier than Unilever and therefore deserves a far higher equity risk premium.

Customers could desert, its products and services might be superseded by a bigger rival, or management might execute their strategy poorly.

Although the shares yield close to 5%, to invest in this kind of business investors are going to want a much higher return on their money.

Just how much riskier the business is and therefore how much higher the return should be are impossible to calculate, but if we said an appropriate risk premium for Micro Focus was 15% it wouldn’t be that wide off the mark.

Over the 10 years to 31 December 2018 the share price of Micro Focus had risen at a CAGR of 24.5% which is not that far from our best guess of 15% plus 5% of dividends plus the 1.5% risk-free rate.

There are no hard and fast rules for working out the risk premium but knowing what the business does and what its shares have done is a good starting point.

Generally speaking, the riskier the business the higher return you should expect for investing in it.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.