Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTemple Bar manager makes the case for value

There has been a lot of talk in the market in recent years of value being out of favour and growth stocks firmly in the ascendancy.

Investors have certainly been prepared to pay a premium

price to secure exposure to rapidly expanding companies or at least those who are perceived to be growth stories.

Temple Bar Investment Trust (TMPL) is no follower of fads or fashion. Since August 2002 the portfolio has been run by contrarian investor Alastair Mundy and his team of value investment specialists at Investec Asset Management.

It’s a testament to their skill that despite the widely-reported under-performance of value stocks in the last few years, Temple Bar has beaten the FTSE All-Share over the last decade and by a wide margin.

PROOF THAT VALUE CAN OUTPERFORM GROWTH

Cumulative returns for Temple Bar shares are 182% over the last 10 years while the net asset value has increased by 185% compared with a return of 138% for the FTSE All-Share.

As manager Alastair Mundy says, value investing may be simple but it’s not easy.

‘Investors love stories and are happy to extrapolate trends to excess in preference to assuming facts change. This drives share prices to extremes in both directions’.

With cheap stocks as a group performing poorly last year compared with growth and momentum stocks, aversion to value is widespread.

The investment cycle is now at the point where as a value investor ‘it feels as though people are being exceptionally nice to you as some sort of compensation for your poor career choice’, he adds.

AVOIDING VALUE TRAPS

In order to avoid buying cheap stocks which stay cheap, or ‘value traps’, the team looks closely at capital structure, market position and governance.

It has applied the same process consistently with every investment since 2002.

The team looks for structural risks like hidden liabilities on a firm’s balance sheet, its market position, whether the business is at risk of being made obsolete by some fancy new technology or disruptive newcomer, and its corporate governance.

Assuming there is no structural risk the team will conduct a deep-dive analysis of the business and compare it to its peers.

If it passes muster and meets the value and income criteria, it makes it into the portfolio.

It’s a mark of how tough the due diligence process is that several high-quality stocks with good management and good models trading on cheap ratings still don’t make it into the basket.

FROM FALLEN ANGELS TO CYCLICAL LEADERS

Stocks which have made it into the portfolio typically fall into one of five categories.

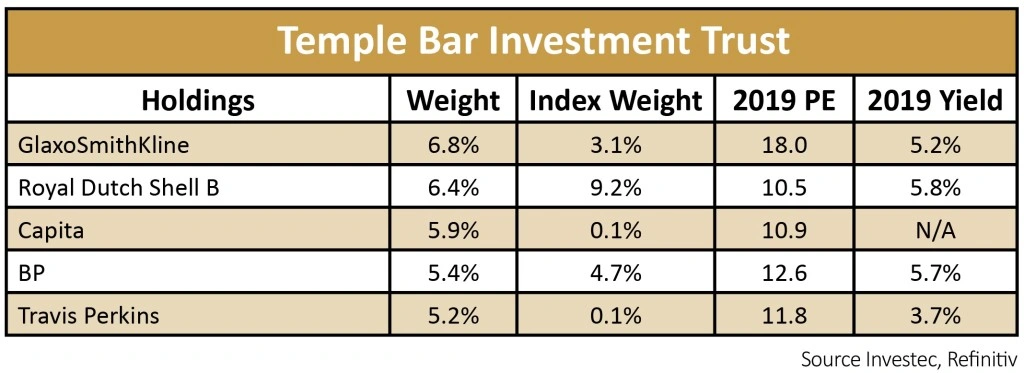

GlaxoSmithKline (GSK), the biggest holding, is a ‘fallen angel’ or former market darling which has fallen out of favour with investors but continues to compound earnings cheaply.

Meanwhile Capita (CPI) is in turnaround mode, and it finds its way into the ‘hidden assets’ category, along with Royal Bank of Scotland (RBS).

INCOME PLAYS ITS PART IN TOTAL RETURNS

The trust’s brief is to provide growth in income and capital to generate a long-term total return greater than the FTSE All-Share index.

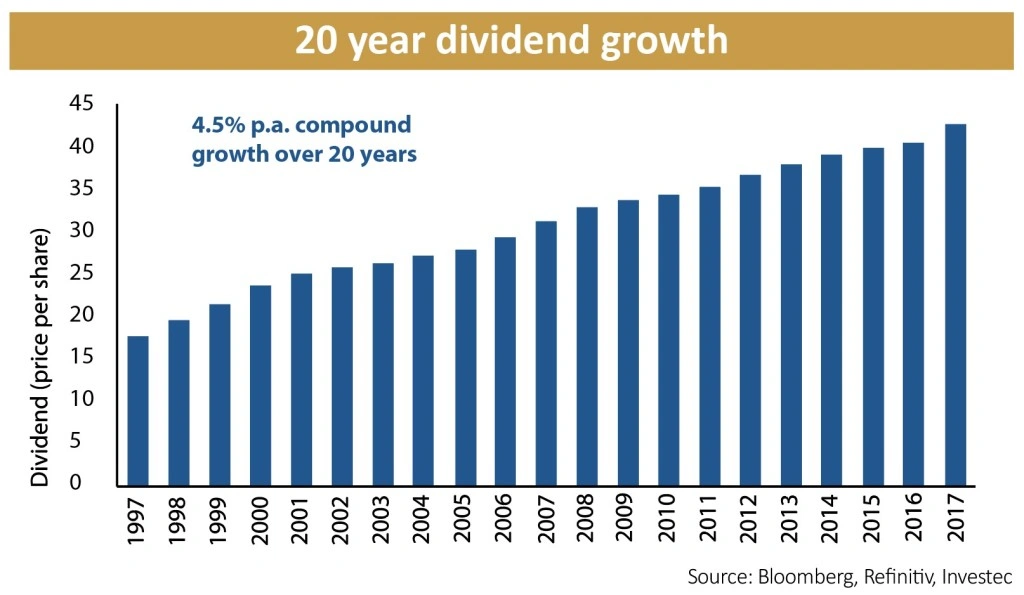

As well as picking cheap stocks with significant potential to re-rate, the trust has an enviable record of dividend growth.

It is one of the Association of Investment Companies’ (AIC) ‘Dividend Heroes’ meaning it is one of a small group of investment trusts which have raised their dividend every year for over 20 years.

Not all of the holdings pay a dividend, as is the case with Capita. However stocks with low or no dividends have to be very cheap to compensate.

All of the holdings must have solid balance sheets too. That doesn’t mean they have to be AAA-rated but they need to be good enough to let management run the business without worrying about financing.

DIVERSIFICATION WITH PRECIOUS METALS

Mundy argues that value stocks are uncorrelated with the wider market to begin with but just for good measure he has 3% of the fund invested in physical gold and silver.

This is very unusual for an investment company but as Mundy says there are ‘significant tail risks’ in today’s markets and if a meltdown occurs precious metals should move up while stocks move down.

The price for this ‘insurance’ is the lack of dividends on metals so the trust’s overall yield is slightly reduced.

OVERWEIGHT UK DOMESTIC STOCKS

Temple Bar has no weighting at all in large internationally-exposed stocks such as British American Tobacco (BATS), Diageo (DGE), Unilever (ULVR) or Vodafone (VOD), which make up

roughly 10% of the All-Share, because they do not fit his investment criteria.

Mundy describes his 60% weighting in UK domestic stocks as ‘the elephant in the room’ but he argues that domestic earners offer the best value on historically depressed earnings.

He also observes that other investors are leaning more towards his position and wonders whether the team should skew the portfolio further towards domestic stocks.

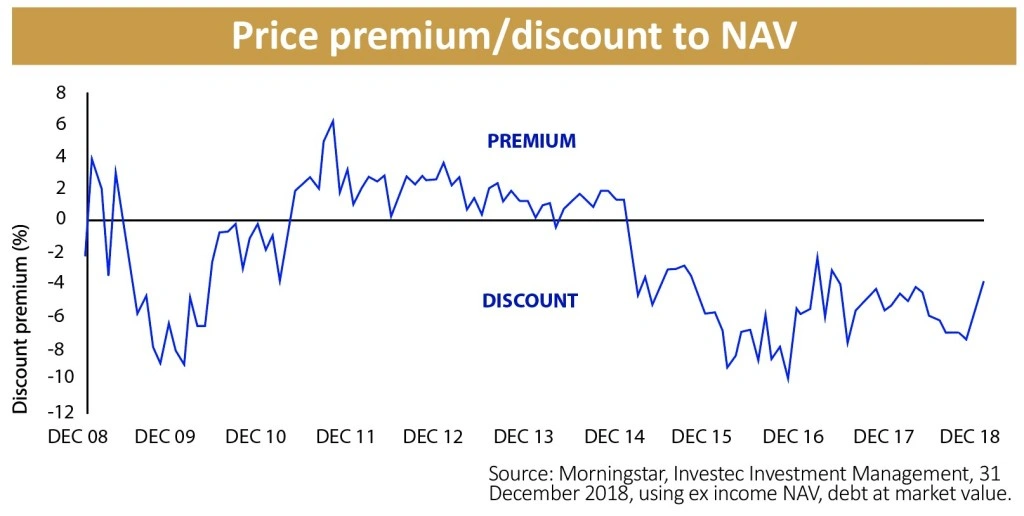

When the board considers the discount to net asset value to be excessive it addresses it by repeated share buybacks.

If the trust trades at an excessive premium the board will authorise repeated share issues, either new shares or treasury shares.

Over the last decade the discount has never been allowed to hit 10% and the premium has only once breached the 5% level. Temple Bar is set to report full year results on 20 February.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.