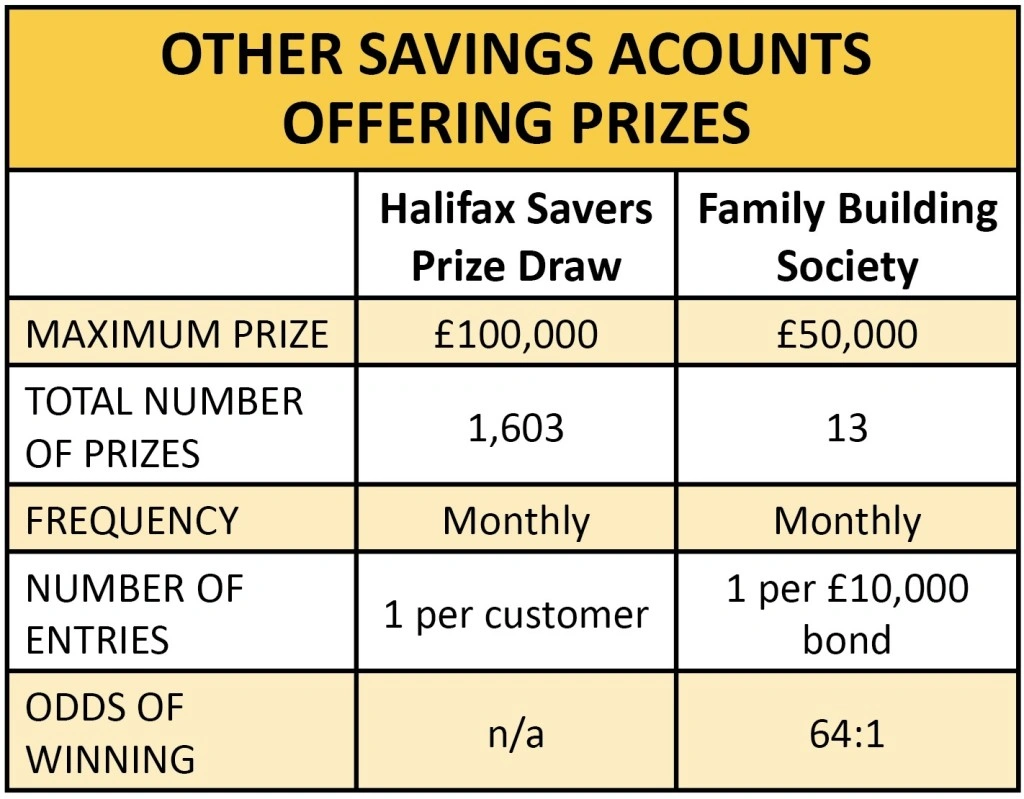

Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazinePremium Bonds: is it time to move on?

National Savings & Investment (NS&I) has just cut the minimum investment into Premium Bonds to encourage more investors to put money into one of the uk’s most popular savings vehicles. It wants to attract £9bn of new investment into its savings products. Are Premium Bonds outdated or a valid investment in the current environment?

Unlike the soda fountains and drive-in movies of the 1950s, Premium Bonds have boasted enduring popularity since their launch in 1956: more than £78bn is held in them today by 21m savers.

But we believe they should largely be left behind like other relics of the past. The long-term returns from other asset classes, as we discuss in this article, have been significantly better.

While there is no harm in holding on to existing Premium Bonds or even buying a few here and there with spare cash, they should definitely not be a mainstay of your investment portfolio.

WHAT ARE PREMIUM BONDS?

Premium Bonds are issued by NS&I and backed by HM Treasury.

You can buy bonds for £1 each, now with the new, lower minimum investment of £25.

An important point to remember is that Premium Bonds are literally a lottery. They don’t earn interest. Instead, each bond has a unique number which is placed into a monthly draw where you can win prizes from £25 to a £1m jackpot.

NS&I says its annual prize fund rate is 1.4%. For every £10 of Premium Bonds sold, it pays out 14p in prizes. The odds of winning a prize for each £1 bond are 24,500:1 but the more you own, the greater your chances.

Prizes are exempt from income tax and capital gains tax. This used to be a big selling point, but it’s less of a draw since the introduction of ISAs and more recently the personal savings allowance.

That’s because the latter allowance lets basic rate taxpayers earn £1,000 of interest tax-free, and for most people – 95% in fact – that’s a generous enough allowance for them not to have to pay any tax on their savings.

The tax-free element of Premium Bonds is really only useful for a small minority with very large savings pots. NS&I says 2.3% of Premium Bond holders have the maximum allowed £50,000 invested in them.

Because Premium Bonds are Government-backed, they are protected, but this isn’t much of a bonus either – the Financial Services Compensation Scheme protects deposits up to £85,000 anyway, more than the maximum you can hold in Premium Bonds.

WHO BUYS THEM?

So, who’s buying them? A lot of us, apparently: NS&I says one in three people in the UK holds Premium Bonds.

They have traditionally been popular among grandparents wanting to gift them to grandchildren, and this is still the case. Previously only available to buy for others via post, NS&I made Premium Bonds available to buy online on behalf of grandchildren in August 2018.

Since then, 44,000 grandparents have bought them, with 26,000 of these buying online. Under-16s own £1.1bn in Premium Bonds, NS&I says. From March, anyone will be able to buy them for children under 16, opening them up to godparents and great aunties as well as parents and grandparents, so this number is set to rise.

HOW DO THE RETURNS STACK UP?

The 1.4% prize fund rate is better than the rate on many cash savings accounts at the moment – the average rate on a one-year fixed ISA reached a three-year high of 1.35% in January, according to Moneyfacts.

The problem is that the Premium Bond rate isn’t guaranteed, you

could be unlucky and win nothing at all. It also lags inflation which is currently running at 2.1%, meaning the real value (or the purchasing power) of your savings would be eroded over time.

Looking back at data since 2000 covering returns from the major asset classes, the best place to put your money would have been in gold, for a compound annual growth rate of 8%. UK gilts would have given you 5% a year, global equities (using the MSCI World with dividends reinvested) would have given you 4.5%, while inflation averaged 2% a year over that time. Meanwhile, your house would have been going up in value at an average rate of 6.4% a year over the same period.

COULD THIS CHANGE?

Cleary, in comparison, Premium Bonds do not offer a great rate, but they could be set to rise. Premium Bonds paid out a record number of times last year, with winnings totalling £1bn, because they attracted a lot of new investment. The prize pot is funded by interest on the bonds, so more prizes are paid out the more bonds are sold.

The Government quietly slipped in some changes to Premium

Bonds in the 2018 Budget. It raised the net financing target from £6bn to £9bn, meaning the amount of money people will be encouraged to put into NS&I products including Premium Bonds.

This means the bonds could start to offer more generous payouts to attract enough investment to meet that target.

Lowland Financial’s managing director Graeme Mitchell says he sometimes recommends Premium Bonds to clients in the place of cash ISAs. He notes there’s a slim chance of winning the £1m jackpot, but even if you win a few small prizes, you could still beat the return available on cash.

‘If you stick £25,000 in you may win a prize, it might just be £25 but it adds up. Say you got £300 over the course of a year, that’s about a 1% return,’ says Mitchell.

‘There is no risk, it is Government-backed, you’ve got absolute safety with the potential and the fun of seeing whether you win each month. You can get your money out within 10 days so it is accessible, and there is a £50,000 limit which should tide most people over in terms of cash reserves.

‘They are a very viable alternative to cash ISAs. If interest rates rise you might find cash ISAs become more appealing but then Premium Bond rates may go up too.’

REMEMBER THE ‘OPPORTUNITY COST’

Neil Liversidge managing director of advice firm West Riding Personal Financial Solutions, says there is an opportunity cost to owning Premium Bonds because the odds of winning are low, and you could instead give your savings a chance of growing much more substantially by investing them in the stock market. ‘Personally, I don’t own any but if I did I wouldn’t hold more than £100 worth. You might get very lucky but, statistically, you won’t, and the opportunity cost for me is unacceptable.’

He says the interest rates on Premium Bonds, cash savings accounts and cash ISAs are generally low so there isn’t much to choose between them. He suggests buying an index fund tracking a major market instead, such as the UK where he says valuations look depressed. Vanguard FTSE 100 (VUKE) (exchange-traded fund) gives you a 3.7% yield – ok, your capital is at risk but that yield is not bad by anyone’s standards these days.

‘If you want to have some fun, put £100 in Premium Bonds for the chance to win the top prize, but would I put the maximum in? Absolutely not because that’s a lot of money to put in for a small chance of winning a substantial prize, and no capital growth.’

FOR FUN, NOT FOR FUNDING INVESTMENT GOALS

Premium Bonds offer an element of fun for ordinary savers who like the idea that they might win a big prize, even if the chance is very small. After all, plenty of people play The National Lottery every week and the chances of winning the jackpot are 45m:1.

They are also an easy way for relatives to give cash gifts to children. For high earners and those with large savings pots who have maxed out their tax-free allowances elsewhere, Premium Bonds could be a useful place to park their excess cash.

For everyone else, there are almost certainly better options to invest your money in – many of which you can read about in Shares.

But if you’ve already got some old Premium Bonds sitting in a drawer somewhere, it’s worth digging them out to see if you’ve won – they don’t expire and there are more than £60m worth of unclaimed prizes.

PREMIUM BONDS - ARE THEY RIGHT FOR YOU?

PROS

– A chance to win tax-free cash prizes in a monthly draw

– All the money you put into a Premium Bond is secure

CONS

– There is a chance you will win nothing

– You won’t earn regular income on your bonds

– Your return is unlikely to beat inflation unless you win one of the bigger prizes

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.