Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat is the pound’s rally saying about investors’ view of Brexit?

Sterling is considered to be the ultimate barometer for Brexit and the currency movement is currently telling us that the market has become more optimistic about how the UK/EU split process will play out.

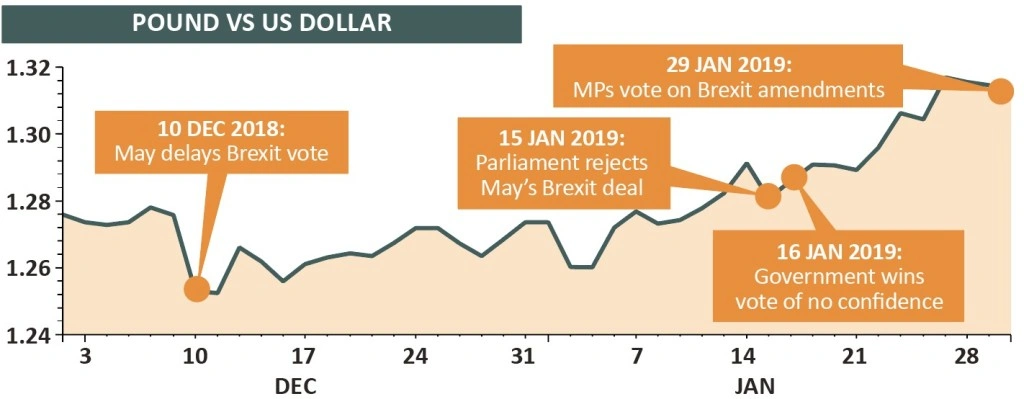

The pound has increased by 4.7% against the US dollar, and by 4.1% against the euro, between 10 December 2018 when UK Prime Minister Theresa May delayed the UK parliament vote on her Brexit deal and 30 January 2019 when markets had time to digest the vote by MPs on Brexit amendments.

Also giving support to the pound has been disappointing economic data from the Eurozone which has weighed on the euro currency.

LOOKING FOR SIGNALS

Investors are watching for any signs that suggest we could get a softer Brexit and positive signals could, in theory, give further support to the pound. Any sign that the UK is not going to crash out of the EU on 29 March without a deal would be favourable for the currency.

That said, you also have to consider that investors could start to panic as the March deadline draws ever closer, so do not think we are in safe territory when it comes to the UK currency or stock market simply because the pound has been strong in recent weeks.

‘Parliament may not get a chance to vote again on May’s deal until mid-February. This is worrisome, to put it mildly,’ says Holger Schmieding, chief economist at investment bank Berenberg. ‘Every day that passes without a resolution is a day closer to a hard Brexit.

‘Still, if markets see that the majority in parliament that opposes a hard Brexit continues to strengthen its influence over Brexit, sterling can edge higher. If and when the UK actually dodges the hard Brexit bullet by agreeing some soft Brexit outcome, or by deciding to remain in the EU, sterling could rise significantly higher.’

BUY UK STOCKS NOW OR WAIT?

Against this backdrop it is worth noting that shares in UK-listed companies are close to the most under-owned by fund managers in history, says Marcus Morris-Eyton, a portfolio manager at Allianz Global Investors.

Citing data from Bank of America Merrill Lynch’s global fund manager survey, he says fund managers were only more pessimistic towards UK equities during the global financial crisis in 2008.

A further rise in sterling would have a positive impact on many UK shares, particularly those which generate earnings domestically.

Investors need to decide whether they want to wait for clarity and reappraise UK shares once the Brexit process is agreed, or buy now while there is still some uncertainty.

Opting for the former could mean you miss out on any market rally the instant the final Brexit process is laid out, assuming the terms are favourable, although you would also avoid the risk of a scenario where Brexit becomes ugly and the market takes another dive.

VALUATION DISCONNECT

‘UK shares are trading at a 30% discount to their global peers.

UK domestic-focused businesses are trading at a 20% discount

to UK global exporters,’ says Morris-Eyton.

The market has been ignoring the fundamentals to focus on the politics, yet the fundamentals have been relatively good. In 2017 UK companies had (nearly) 30% earnings growth; in 2018 it will probably be 10%; and 2019 should again be positive. There are many international companies listed in the UK which should be more resilient than people are valuing them.’

As part of the team who manage Allianz European Equity Growth Fund (B2NLGG1) and Allianz Continental European Fund (B3Q8YX9), Morris-Eyton says he looks for companies that are high quality and capital-light with their production centres very close to where they are selling those goods.

‘That mitigates the risk of tariffs but also gives these companies the necessary pricing power to respond in any given Brexit scenario,’ he explains.

‘The beauty of that investment process for us is that it means we don’t need to be able to call a particular Brexit outcome because we have confidence that the companies we are investing in have the right models to be able to respond in those scenarios.’

Companies in his portfolios include global operators Reckitt Benckiser (RB.), British American Tobacco (BATS) and Unilever (ULVR), plus UK domestic names including Rightmove (RMV), Auto Trader (AUTO) and Howden Joinery (HWDN).

Morris-Eyton suggests some of his investments, by virtue of their qualities, may be positively impacted by Brexit long-term if their weaker competitors struggle.

He also says investors should consider that weak companies may be looking to use Brexit as a cover-up for their own problems. ‘For a company facing cyclical or structural challenges Brexit provides a very convenient excuse for them to explain their own weakness. Part of the challenge for us as stock pickers is to decide what is down to Brexit or what is down to more serious issues that company is facing.’

One area that may have delayed effects is the uncertainty Brexit is creating on business investment plans. The Allianz portfolio manager says his team keep hearing frustrations from companies over the lack of certainty regarding UK Government policies.

‘Very few companies have made decisions with regards to Brexit in terms of moving physical or human capital out of the UK. But you are seeing companies delay investment or moving investment elsewhere,’ explains Morris-Eyton. He says it is very difficult to quantify that impact until 10 or 20 years later.

Investors have a lot of issues to weigh up and may find the best solution is to allocate a portion of their money to UK domestic stocks as part of a broader, diversified portfolio. Don’t bet all your money on a Brexit rally; equally don’t ignore the significant value on offer in UK equities at present.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.