Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThree reasons why you shouldn’t invest in HSBC

Avoiding bad stocks is equally as important as picking good ones. Investing must always involve a detailed research process rather than random selection as prospects which may seem enticing at first glance aren’t always up to scratch when you dig deeper.

In the case of HSBC (HSBA), many investors look at its generous dividend payments and think it is a good business generating millions of dollars in profit. This article will explain why HSBC isn’t as good an investment as you might think.

ASIAN DOMINANCE

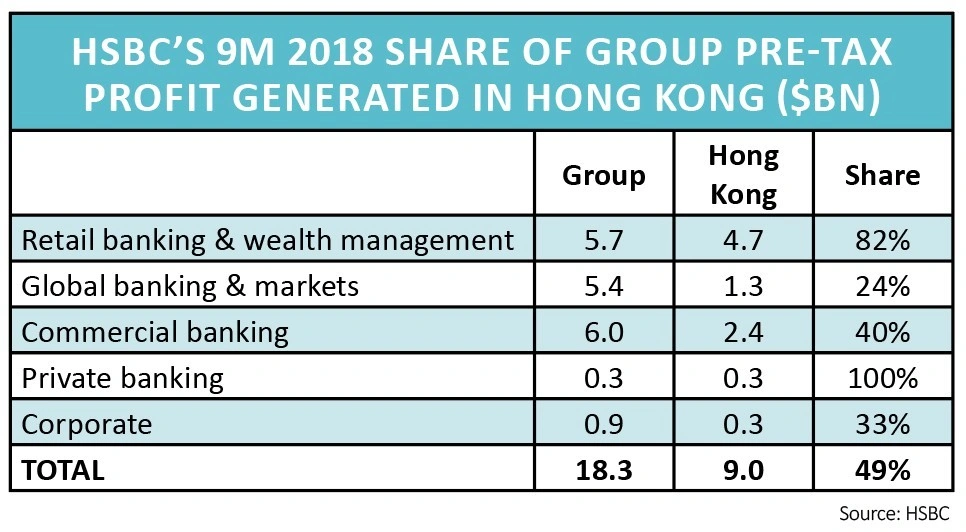

HSBC likes to call itself ‘the world’s local bank’ but the heart of the business remains centred in Asia. Hong Kong accounts for a third of the bank’s revenue and almost half of its pre-tax profit.

The bank has four main businesses: retail banking and wealth management, commercial banking, global banking and markets, and private banking.

It also has a central corporate division which manages the bank’s central costs, balance sheet, joint ventures and interests in other banks.

A BREAKDOWN OF EARNINGS

HSBC’s biggest business is retail banking and wealth management which generated $16.8bn of revenue in the first nine months of 2018 or 40% of the group total.

Pre-tax profit from retail banking and wealth management was $5.7bn in the first nine months of last year, accounting for 31% of total profit.

While HSBC has 37m retail customers spread across the world, Hong Kong still generates over 40% of the company’s retail banking and wealth management revenue and over 80% of profit.

The UK typically generates less than 30% of revenue and 10% of profit in retail banking and wealth management by comparison.

In the UK, HSBC has a network of around 1,100 branches thanks to its takeover of Midland Bank in 1992, plus it owns First Direct which was launched in 1989, and it owns Marks & Spencer’s (MKS) financial services business which it bought in 2004.

FOURTH QUARTER EARNINGS FEAR

The next biggest business is global banking and markets which made $12.4bn of revenue in the first nine months of 2018 or 30% of the group total.

Thanks to strong financial markets, pre-tax profit was up 7% to $5.4bn in the first nine months of last year, accounting for 30% of group profit.

Given the shake-out in bonds and stocks in the final quarter of 2018, investors would be wise not to assume that the picture will remain positive when the bank reports full year earnings on 19 February.

The UK may generate more revenue from global markets than Hong Kong but with all the people it employs in Canary Wharf most of the income gets soaked up before it can reach the bottom line.

In 2017 as a whole the UK arm generated revenue of $4bn or nearly a third of the group total but profit was a miserly $200m, just 4% of the total.

Hong Kong generated $2.4bn of revenue and $1.3bn of profit or 24% of the total in the first nine months of the year, making it significantly more profitable than the UK.

STILL A LEADING PLAYER IN GLOBAL TRADE

Just behind global banking and markets in terms of turnover is commercial banking which generated revenue of $11.2bn in the first nine months of last year or 27% of the total.

The bank’s network covers 66 countries and territories which account for 90% of global GDP and capital flows so it is truly plugged in to world trade.

This is a great business with high margins and is growing fast but again Hong Kong outshines the UK when it comes to returns.

Lastly HSBC has a private banking business for high net worth individuals which brought in revenue of $1.4bn and profit of $300m in the first nine months of 2018.

In terms of margins that was a big improvement on the previous year but in terms of actual profit $300m is still less than 2% of the group total.

STRATEGIC DECISIONS LIE AHEAD

Last October the bank presented its strategic priorities for 2019 and 2020. Top of the list is to grow further in Asia, where it is clearly in a position of strength, and to increase its mortgage and commercial banking market share in the UK.

Growing in Asia makes complete sense and the obvious area to allocate capital is private banking. The business is sub-scale yet HSBC is one of the most trusted names in the region.

Growing its market share in UK commercial banking also makes sense as it is a high-margin business.

Throwing more money at the UK mortgage market makes no sense whatsoever as margins are wafer-thin and falling.

Next on the list is to reboot its US business, which far from being a ‘third leg’ as originally envisaged is sub-scale and underperforming, generating less revenue and profit than its UK business.

The bank made no mention of global banking and markets within its strategic priorities but if as we suspect the fourth quarter shows a big black hole in the markets business there will be more calls for it to rethink its strategy.

Only a small proportion of income seems to trickle down to earnings compared with other regions and other businesses, even when markets are good as they were for much of the first nine months of 2018.

SHARES SAYS:

With a 6% dividend yield, a forward earnings multiple of 12-times and a price-to-book ratio of less than one HSBC may look cheap to value hunters but we think there are three good reasons for the shares to stay cheap:

Revenue and earnings growth are highly dependent on Hong Kong, and the Chinese economy is clearly slowing.

Its UK mortgage business is soaking up capital with minimal returns.

Its investment banking business is doing the same thing but with the additional downside risk that trading global markets entails.

Our conclusion is that you should avoid HSBC’s shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.