Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

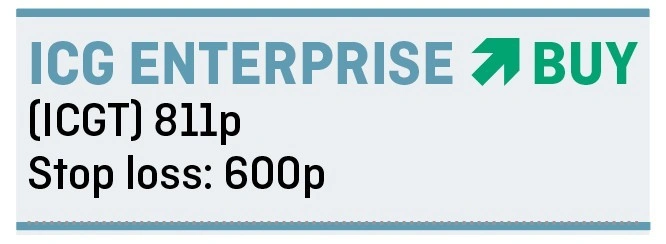

magazineSnap up ICG Enterprise at a big discount while you can

In recent months the discount to net asset value (NAV) at private equity investment trust ICG Enterprise (ICGT) has widened dramatically despite no significant change in the management, strategy or fortunes of the fund.

This has created a compelling value opportunity for investors.

A recently published quarterly NAV update covering the three months to 31 October 2018 brought home the scale of this opportunity.

The shares are currently trading at a 22% discount to the latest NAV of £10.46. To put this in context the same portfolio traded at a 9% discount in May 2018.

The nature of the investments made by the trust means some kind of discount is almost inevitable as unlisted companies are less easy to sell (and to value) than those which trade on a stock market, but the current situation seems anomalous.

It also seems odd when you consider in the nine months to 31 October 2018 the company netted £118.5m from realisations (sales) from its portfolio at a 30% uplift to the value they were marked up on its books. The company says it has continued to achieve realisations at an uplift to carrying value since period end.

The trust has been investing in unquoted businesses for nearly 40 years. In early 2017 the running of the fund was handed to specialist asset manager Intermediate Capital Group which has more than €34bn in assets under management and a footprint in more than 14 countries. According to stockbroker Numis, this has made the trust ‘a far more attractive vehicle’.

Research group Kepler explains the investment criteria applied by fund managers Emma Osborne and Kane Bayliss: ‘The team have been investing in companies which in their view exhibit defensive growth (recurring revenue, quality earnings, barriers to entry), structural downside protection (including investing in the debt and equity of deals), and relative value (where deal dynamics have facilitated investment at very attractive valuations).’

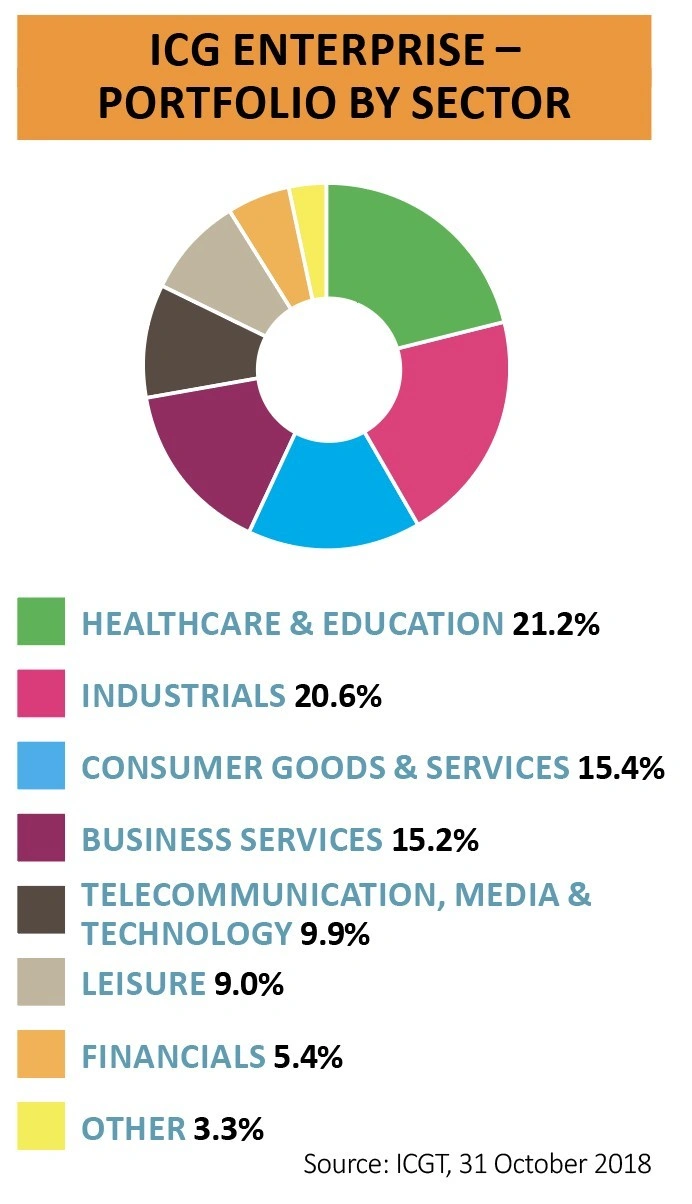

The emphasis is also on firms whose earnings growth is not too closely linked to the business cycle, operating in areas like healthcare and education. This relatively defensive focus should chime with investors at a time when market volatility is increasing.

The group’s top holding, for example, is City & County Healthcare, a provider of home care services.

There is plenty of firepower to invest further, with a cash balance of £62.6m at the last count and access to an undrawn bank facility of £104.7m.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.