Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineJoules proves there is still life in the retail sector

Despite the headwinds facing UK quoted retailers, a rare band of sector constituents are generating robust growth and boast compelling international dimensions to their growth stories.

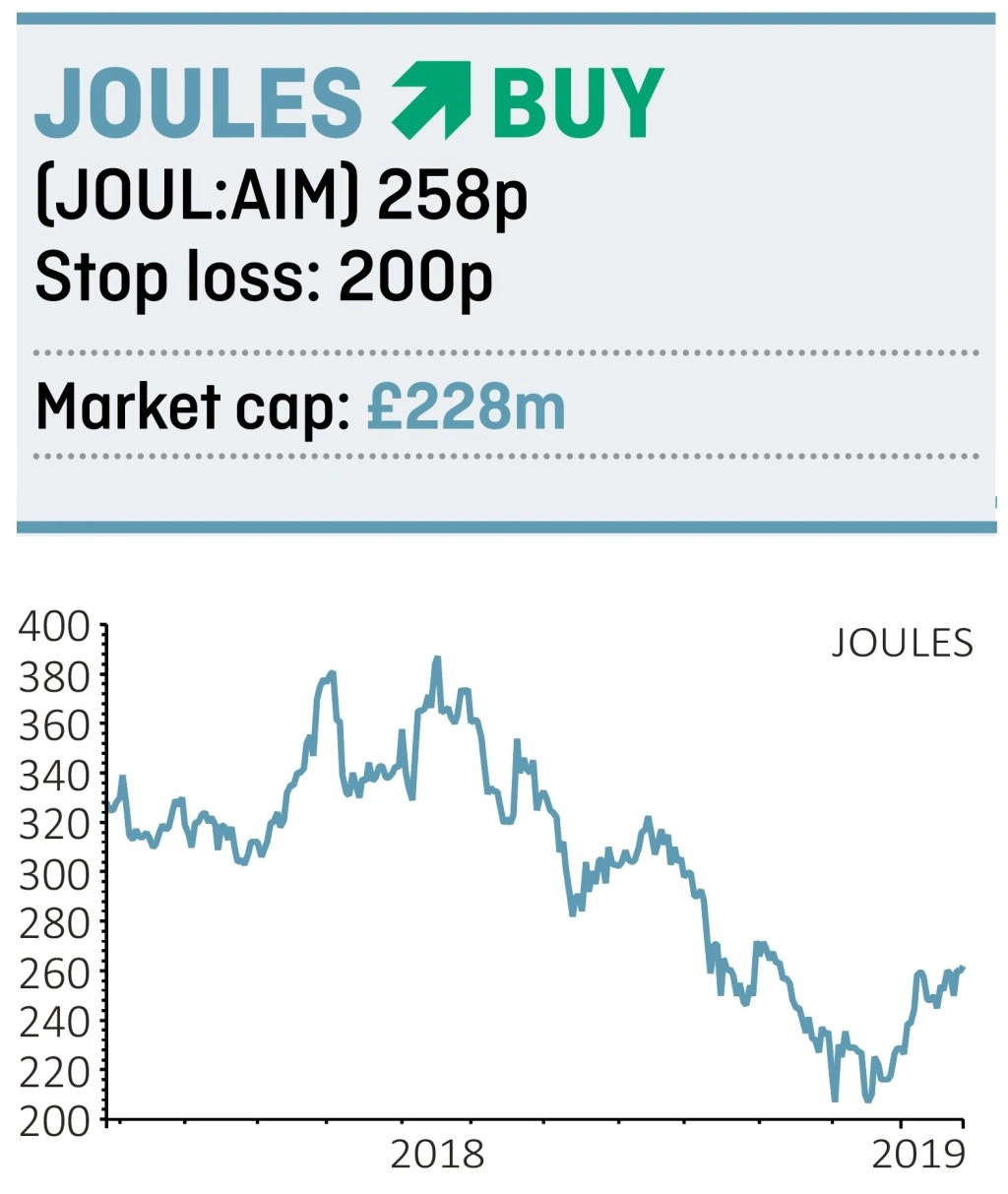

Within this cohort is Joules (JOUL:AIM), a UK premium lifestyle brand that is immature in comparison to peers and whose undemanding valuation is at odds with its stellar trading performance. We think the shares look good value at 258p.

Octopus Investments fund manager Chris McVey says Joules’ share price has been under significant pressure over the last six months as the market became increasingly concerned regarding the high street. However, this is at odds with the figures produced by the company.

Sparkling first half results to 25 November revealed 17.6% sales growth to £113.1m and underlying pre-tax profit up 14.7% to a better-than-expected £10.7m. Net cash of £4.3m was up £1.3m year-on-year.

Importantly, Joules also reported an acceleration in sales growth over the Christmas period.

Founded in 1989, the company is a truly multi-channel lifestyle brand with origins in equestrian and country fairs. One key strength is its flexible ‘total retail’ model, which means Joules is a brand owner first and foremost and therefore ‘agnostic’ as to where customers shop.

McVey says Joules has an increasingly diverse revenue base. As well as trading from over 120 UK stores, Joules is also a top selling wholesale brand in John Lewis and Next Label, online sales are growing rapidly and licensing income is on a growth tear, with a pipeline of licence deals waiting in the wings.

Over half of Joules’ sales come from womenswear, yet the brand’s family appeal has enabled it to expand into menswear, footwear, childrenswear and accessories. Crucially, Joules’ focus on classic styles with a contemporary twist reduces fashion risk.

Joules continues to expand on home turf but also internationally, where half year revenue rocketed 64.2% higher. The overseas focus is on the US, the star of the show where it is seeing good growth with department stores Dillard’s and Nordstrom, as well as in Germany, where Joules’ relationship with retailer Zalando is developing nicely.

For the year to May 2019, Liberum forecasts a pre-tax profit jump from £12.9m to £14.8m ahead of £17.9m in 2020 and £19.5m in 2021.

Based on 2020’s 16.3p earnings per share estimate, progressive dividend payer Joules’ shares are swapping hands for 15.8 times earnings. That isn’t excessive given the globally-derived growth rates Joules is expected to generate for some time to come.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.