Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCan BP beat expectations again with results on 5 February?

Oil major BP (BP.) has a proud track record to uphold when it reports fourth quarter and full year results on 5 February.

Every other set of quarterly figures for 2018 saw the £99bn market cap beat expectations. In the third quarter replacement cost profit, an industry standard measure of income, came in at $3.8bn against the consensus forecast for $2.85bn.

It was also a positive story in the second quarter, with the same measure of profit coming in at $2.8bn against expectations for $2.7bn and the dividend was hiked for the first time in four years. Profit in the first quarter was 17% ahead of consensus.

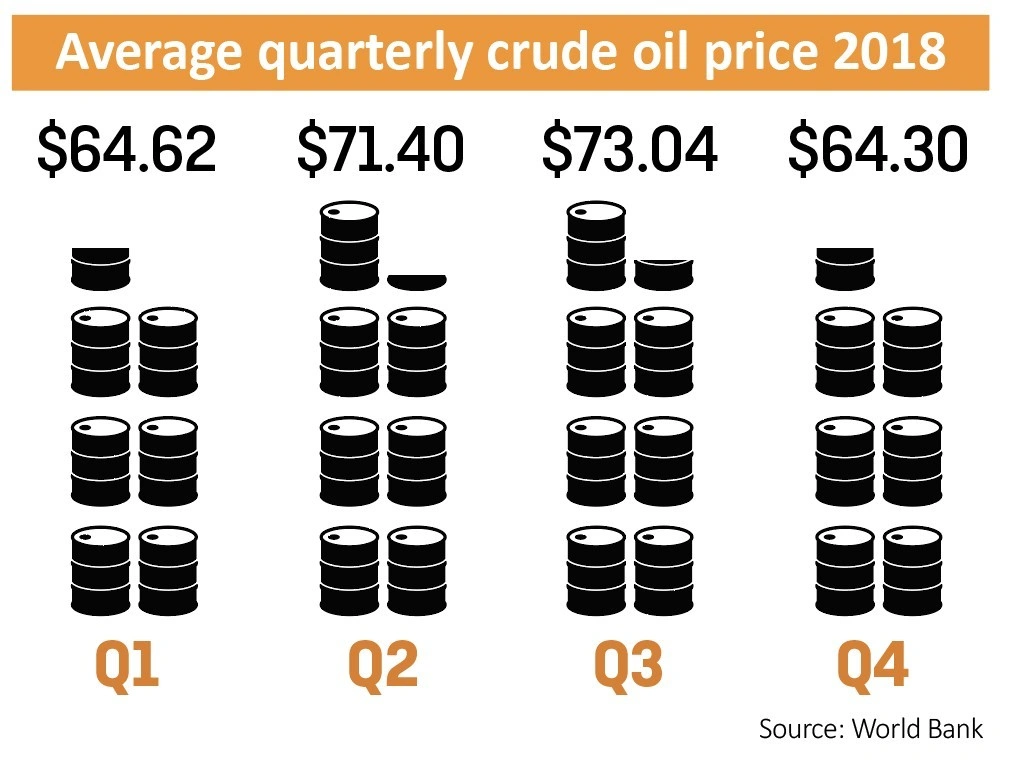

These quarterly results were supported by an improving oil market. Unfortunately the backdrop changed in the fourth quarter.

The graphic shows the average crude price for each quarter of 2018 – the decline in the final three months of the year is notable.

The fourth quarter period will therefore be a test of the more streamlined BP, which has focused on increasing the efficiency of its operations and divested non-core assets in recent years, and whether it can deliver another better-than-expected showing despite the decline in the oil price.

Last October, the company’s strong operational performance had seen the shares almost recover to the highs they reached above 600p prior to the disastrous Gulf of Mexico oil spill in 2010.

At the time of writing the stock had slumped to 495p, reflecting the less buoyant oil price environment.

Analysts are currently forecasting a near-30% decline in fourth quarter earnings per share on the third quarter total. Anything better than this amount could potentially act as a positive catalyst for the share price.

As an integrated oil firm, BP’s operations span everything from exploring, developing and producing deposits of oil and gas right down to refining the crude, marketing it and selling it to motorists at the pump.

It will be worth keeping close tabs on its refining operations which sometimes benefit from lower oil prices as it reduces the cost of the feedstock used to manufacture petroleum products.

In contrast to BP, London-listed rival Royal Dutch Shell (RDSB), which was due to report on 31 January as this issue of Shares was published, missed forecasts with every one of its own quarterly updates in 2018.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.