Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy you should not be blinded by Vodafone’s 9.5% yield

The dividend yield on the FTSE 100 for 2019 is estimated at 5%, according to the latest forecast data from Link Asset Services’ Dividend Monitor.

By contrast Vodafone’s (VOD) forward 12 months income yield stands at around 9.5%, adjusting for its 31 March year end, according to Numis’ calculations. Being so out of kilter with its blue-chip peer average tells investors something important; either the share price is too low, or the dividend forecast is too high.

In our view, though there are routes by which Vodafone could return to a sustainable dividend growth path, there are better supported, perfectly generous yields in the FTSE 100. We also reckon there are serious question marks about the long-term investment case for the business.

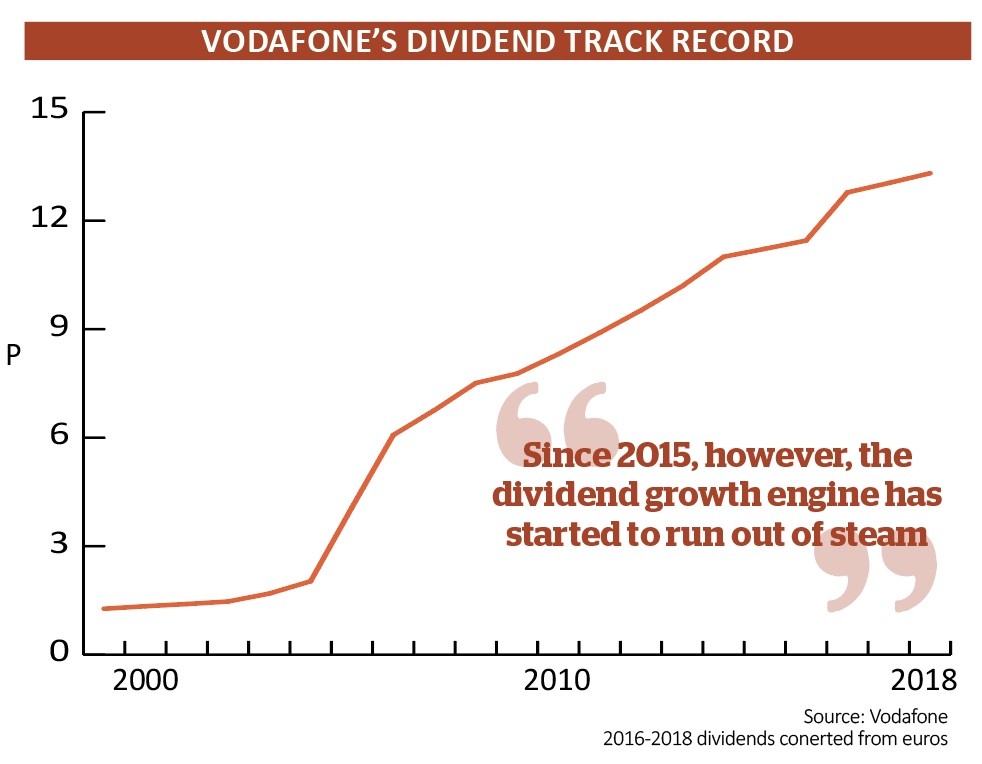

This year to 31 March 2019 the mobile giant is expected to hand shareholders €0.1507 per share. Vodafone switched from reporting in pounds to euros in 2016. If forecasts are right this financial year will be the first in two decades when the payout has been held flat.

Between 2001 and 2014 Vodafone’s dividend growth far outstripped inflation, increasing by more than 5% every year bar one (2009), and showing double-digit increases on several occasions.

Since 2015, however, the dividend growth engine has started to run out of steam. Few analysts feel brave enough to forecast anything other than pedestrian increases in the payout over the next two or three years, if any.

THE CASE FOR A PAYOUT CUT

Question marks over Vodafone’s future dividends centre around huge borrowings, biting competition and potentially significant investment needed in new radio wave spectrum for 5G services, or fifth generation mobile networks that will allow users to send more data far faster over the internet.

These are all valid potential trouble spots, but it may be that investors are over-egging the negative mood.

At the end of this year to March Vodafone is forecast to have net debt of around €32bn sat on the balance sheet. That would imply a net debt to earnings before interest, tax, depreciation and amortisation of 2.2 times based on consensus forecasts.

Typically lenders and bond holders start getting nervous when this metric tips the scales at more than three-times.

On the competition front, it’s been a bit of a blood bath in both Spain and Italy (where roughly 25% of revenue stem from), while the UK has stubbornly refused to growth for a while now. Yet those pressures seem to be abating bit by bit, particularly in Italy where prices are starting to rebound after aggressive promotions by local rival Iliad.

These issues have also masked Vodafone’s success elsewhere in Europe, and in emerging economies in Africa, the Middle East and Asia Pacific (AMAP).

If these trends continue it could relieve substantial pressure on the balance sheet.

GO FASTER INTERNET

The final point is capital expenditure. Multiple 5G spectrum auctions are due over the next couple of years – the UK, Germany, Spain, South Africa the main ones.

Vodafone estimates €1.2bn a year will be needed to fund this investment and while there is the chance that one-off auctions prove more expensive than budgeted, the company’s has gone on record to express its confidence that its crunched numbers are right.

All of this should mean that estimated free cash flow will remain in the €5.1bn to €5.3bn range for the foreseeable future, versus the annual €3.92bn cost of the dividend.

One hint towards a brighter outlook for Vodafone might be the absence of a cut so far despite the glaringly obvious opportunity to do just that.

When Vittorio Colao stood down as chief executive officer (CEO) after 10 years of running the show there was the ready-made replacement of Nick Read to take the top job (since 1 October 2018). He had previously been the chief financial officer so was already well known in City and investment circles.

A change at the top is typically a prime time to rethink strategy and any dividend commitment to investors. Half year results announced on 13 November was that opportunity for Vodafone to rebase its payout promises, yet the company chose not to do so.

Vodafone has even laid out plans for a return to dividend growth, this aim is ambitious but will be aided by a new swathe of operational cost cutting being implemented by new CEO Nick Read, and should also be helped by the cable assets being acquired from Liberty Global in Europe.

If all goes well analysts at Numis predict a steep share price re-rating back to 220p over the next year or so. We’re not so sure.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.