Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy is Germany slowing down?

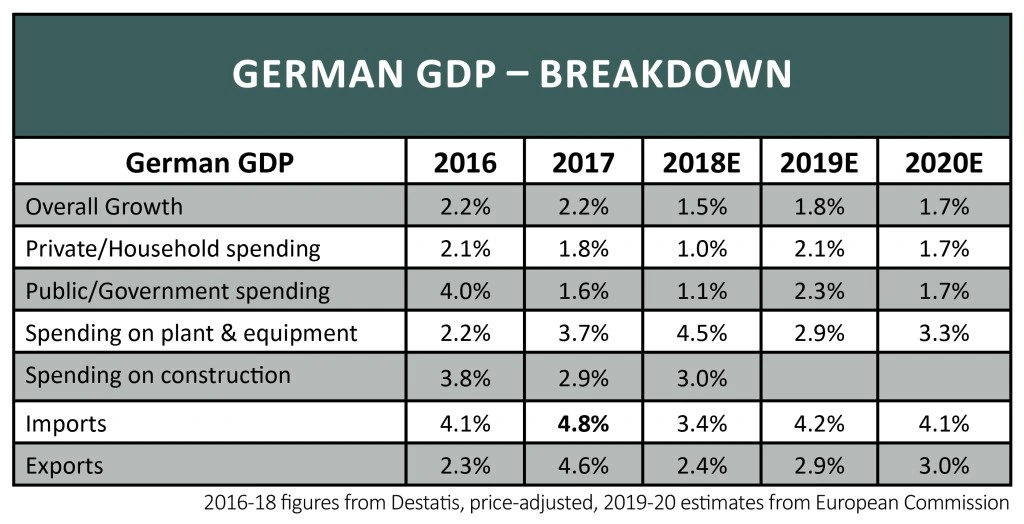

Figures last week from Germany’s Federal Statistical Office showed that gross domestic product (GDP) grew by just 1.5% in 2018, the slowest rate for five years.

That meant that GDP was barely positive in the fourth quarter, up by an estimated 0.1%. If the fourth quarter had been negative like the third quarter, which shrank by 0.2%, Germany would technically

be in recession.

With China slowing, UK growth below its potential due to Brexit worries and the US hamstrung by the government shut-down, the last thing investors needed was bad news from Europe’s largest economy.

PUBLIC SPENDING AND INVESTMENT OFFSET

WEAK EXPORTS

The main areas of growth last year were government spending on big infrastructure projects, which rose by 3%, and company spending on plant and machinery which rose by 4.5%.

By contrast, industrial production, which accounts for around a quarter of the economy, grew by 1% which was below forecasts and below the 2018 average.

Given Germany’s role as a major manufacturer of industrial goods, exports are key to keeping the economy ticking over.

However, exports were also weaker than expected, up 2.4% instead of a forecast 2.8%.

The obvious assumption is that the slowdown was caused by protectionism and weak demand in non-EU markets, but that wasn’t the case.

New manufacturing orders from non-EU countries were marginally lower last year, down 6%, but the big drop was in EU orders which were down 16%.

In other words, the fall in demand for German goods has come from inside the EU not outside.

WEAK CONSUMER SPENDING

Another area of disappointment was household spending which grew by just 1% last year against a forecast of 1.6%.

In terms of big-ticket items, car sales showed a major slowdown in the fourth quarter.

Sales for the first nine months were up 2.4% at 2.7m vehicles, making Germany the biggest market in Europe, but in the final three months they were down 8% or nearly 70,000 units.

Germany is also the largest clothing and footwear market in Europe with estimated annual sales of around €55bn.

However, growth is anaemic with the government forecasting an increase in value of just 1.5% last year. Associated British Foods (ABF) owned Primark recently described the market

as ‘struggling’.

STRONG JOB MARKET NOT BOOSTING CONSUMPTION

Given that unemployment hit a 38-year low in November, similar to the UK, and core inflation is just 1.5%, household spending power is increasing.

In a sign of the tightness of the labour market, the UK recruiters Hays (HAS), PageGroup (PAGE) and Robert Walters (RWA) all saw a big jump in net fee income from Germany in their last quarterly results.

Hays, the biggest recruitment firm in Germany by some margin, saw fees up 15% driven by demand for contract IT and engineering staff.

According to chief executive Paul Venables there are ‘no signs of stress’ in companies’ hiring plans. Also wage pressures are rising as firms compete for qualified staff.

One major reason for consumers being reluctant to spend may be rising rents. Unlike the UK, most people in Germany rent apartments rather than buy houses.

Prices and rents went more or less nowhere from re-unification in 1990 until 2010, but in the last few years they have risen sharply.

It’s not uncommon for a single person to have to spend over 40% of their monthly income on rent and services.

The government has offered tax incentives to increase the quantity of new houses until the end of 2021 but there is no cap on rents or any equivalent of the UK’s Help To Buy scheme.

GERMAN STOCKS PERFORMED POORLY LAST YEAR

Investors in German stocks got a poor deal last year with the Dax index losing 18% of its value while the benchmark MSCI Europe index excluding the UK lost just 10%.

Germany’s weighting in the MSCI Europe ex-UK index was 19.4% in December, so being overweight or underweight the country could make a big difference to fund performance.

The £5bn Jupiter European Fund (B5STJW8) has 33% of its investments in Germany, more than half as much again as the benchmark. The top two holdings are Adidas and Wirecard with a combined weighting of nearly 17% and a combined value of £850m.

In contrast the £1bn Janus Henderson European Growth Fund (3061769) has an 11% weighting in German stocks with only pharmaceutical firm Merck making it into the top 10 (at number 9, with a 2.6% weighting worth £26m).

The £1.1bn Schroder European Alpha Income Fund (B8VX2T6) has just a 7% weighting in Germany or less than half that of the index with no German stocks among the

top 10 holdings.

MILD RECESSION ON THE CARDS?

Given that the official GDP forecast for 2018 was too optimistic, we would expect forecasts for this year and next year to be cut.

The outlook for private spending and exports looks too high given what we now know.

Also, after strong growth in 2017 and 2018, spending on plant and equipment could fall short of estimates.

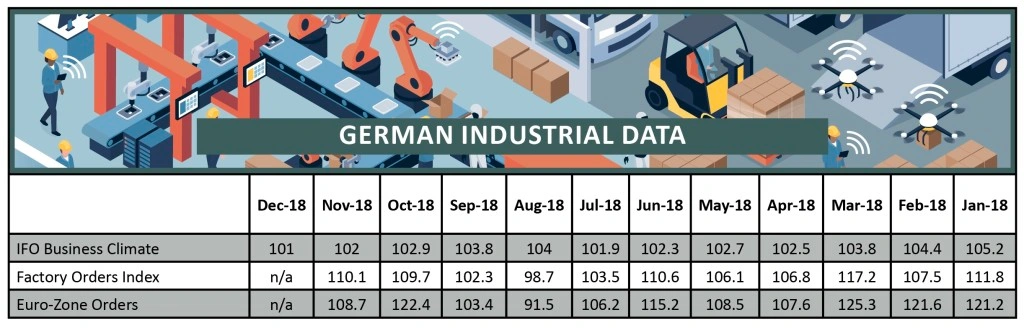

Concerns over the economy have been growing among German businesses according to the highly-regarded IFO survey.

Its Business Climate index fell to an 18-month low in December with manufacturers’ and service providers’ future expectations showing a sharp fall.

The IFO survey is often seen a lead indicator on businesses’ spending plans and can be a good guide to industrial production figures.

It looks likely therefore that Germany could experience a ‘mild recession’ in the next 12 months, so we need to watch the economic data for signs of either a further slowdown or of a recovery in European demand.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.