Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSDL has recovery play credentials

This is a technology company that has been on the UK stock market for close on two decades, yet we wouldn’t be at all surprised to find most investors asking… SDL (SDL) who?

The Maidenhead-based business is a content management and language translation software and services specialist. It helps typically large multi-national clients manage their content across multiple platforms (web, mobile, print etc) in a multitude of languages and dialects.

For example, SDL has more than 3,300 enterprise customers, including 88 of the top 100 global brands in the world, according to analysts at Numis, and operates in 39 countries, de-risking to some extent its exposure to any single region or industry segment.

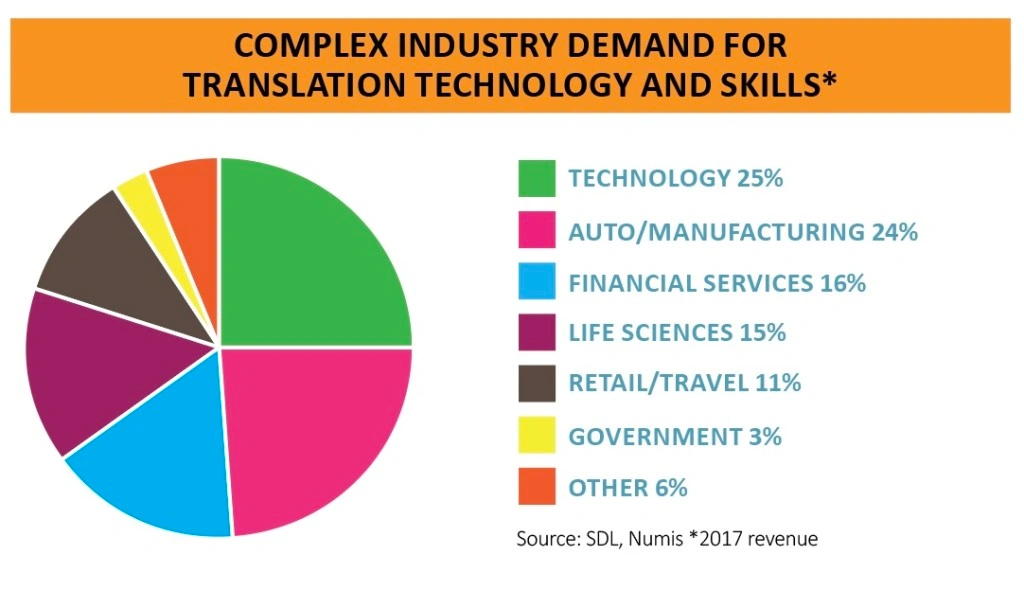

According to research, an organisation needs about 14 separate languages to reach about 75% of internet users worldwide. But accessing the other 25% means adapting an extra 40-plus languages.

That requires real specialisation of the sort provided by SDL. It helps clients really reach out to the limits of a geographic or cultural market by tailoring content in a way that is accurate, efficient and cost-effective.

Most investors will have an obvious objection at this point. Doesn’t Google Translate, Apple’s Siri or Alexa by Amazon do this?

Frankly, no. SDL meets far more complex requirements, such as intricate and nuanced advertising campaigns, detailed legal papers, scientific and medical research and other confidential, sensitive and complex documentation.

That’s what differentiates it from the impressive but fairly mainstream translation engines.

SDL does this either through its automated platform, Helix (the Language Technology division) or through its 1,200-strong team of in-house specialist translators (Language Services), supported by an army of 15,000-odd freelancers that can be called upon when needed.

SELF-INFLICTED WOUNDS

Several years of weak end markets, poor execution and a handful of self-inflicted wounds saw SDL fall off the radar for most investors.

But the arrival in 2016 of current chief executive Adolfo Hernandez saw a root and branch rethink.

This, in turn, sparked a three year turnaround programme that would see SDL return to its translation roots, drive higher value revenues and invest in innovation.

Most of the heavy lifting of that plan has now been actioned and the results are starting to show through in operational and financial performance.

In its recent year end (to 31 December 2018) trading update the company was able to confirm revenue somewhere in the £323m to £325m range (marginally better than £322m consensus expectations) and underlying operating profit of no less than £28.5m, about £1m more than expected.

This should inspire increased confidence in mid-teens revenue growth this year and next that implies £399m of top line income in 2020, according to latest Numis estimates.

SCOPE FOR OUTPERFORMANCE

There may also be scope for outperformance as SDL extracts extra value from July’s acquisition of DLS, a translation specialist to financial and life sciences clients where there is clear scope for operational improvement.

That would tally with underlying operational improvements still be made in the core SDL business, such as bringing around 80% of clients to its automated Helix Platform (lowering costs), streamlining the sales processes and using neural network machine learning and artificial intelligence linguistics.

If all goes well it could have a big impact on profit beyond underlying growth. For example, Peel Hunt estimates that 2017’s operating profit margins of 7.7% will be closer to 8.5% for 2018, and could hit close to 10% by 2020, implying something like 50% operating profit growth over the next couple of years, to around £43m to £44m.

WHAT’S REQUIRED TO ACHIEVE GROWTH

This sort of outcome will clearly rely on no serious deterioration in end market demand for its services. How a global recession might impact business is difficult to predict given the internationalisation of so much commerce these days.

It also requires management to deliver on the implied benefits from DLS (and any future acquisitions), getting integration right and extracting extra value. And the pressure will remain on to carefully balance nearer-term benefits for shareholders with longer-term investment in innovation.

Recent improvements in cash flow metrics are an encouraging development, another step along the road to rebuilding previously damaged investor sentiment. A 2019 price to earnings multiple below 20 (19.6) could re-rate rapidly if signs emerge that SDL is pulling off its return to quality growth status.

SDL is a higher risk investment but an ongoing commitment to a regular and growing dividend, albeit offering a modest 1.3% yield, demonstrates rediscovered financial discipline that some investors will welcome.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.