Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSafety net

When investors buy shares in quoted companies they know that their capital is at risk and that the companies they own could underperform or in the worst-case scenario go bust.

If a stock underperforms the market for a long period of time, sometimes a big activist investor will step in and demand changes in order to raise the value of the business and the shares.

Edward Bramson took a stake in Barclays (BARC) to push for changes and try to increase the share price, while the most famous activist investor is Paul Singer whose Elliott hedge fund has built stakes in dozens of companies.

In the case of investment trusts, if an activist investor doesn’t ride to the rescue there are measures which the managers and the shareholders themselves can use to try to limit the underperformance or if necessary to wind up the trust altogether. This offers a potential safety net for anyone who buys shares in an investment trust.

BUYBACKS AND TENDER OFFERS

One of the key features of an investment trust is its closed-end structure which means that the number of shares issued is fixed at inception.

If the investment trust’s shares are underperforming and the discount to the net asset value (NAV) of its holdings can’t be kept ‘within reasonable bounds’, the number of shares in issue can be reduced through buybacks and tender offers.

A buyback allows the company to reduce the number of shares in issue which normally prevents the discount from widening and can increase the value of the remaining shares.

As Annabel Brodie-Smith, Director of Communications at the Association of Investment Companies (AIC), explains:

‘This can provide an exit for uncommitted shareholders, adds value for existing shareholders and is comforting for investors as in many cases it proves an effective tool for the management of discounts.’

Shareholder approval is normally needed for a buyback and most investment trusts routinely ask their investors each year for approval to buy back up to 15% of their shares to ‘manage’ the discount to NAV.

This is the maximum amount generally allowed by investment trust rules without having to get further shareholder approval.

Purchases of more than 15% of the shares are normally made by way of partial or tender offers.

HOW ARE BUYBACKS FUNDED?

An investment trust has to have enough cash and ‘distributable reserves’ to buy back its own shares.

If an investment trust has been trading for many years it is likely to have built up a level of retained profits or ‘capital reserves’ which it can use to buy back its shares.

However newly-listed trusts or those whose assets have gone down since launch won’t have any capital reserves so their only route to buying back shares is to use the ‘share premium account’.

The share premium account is created when new shares are issued at a premium to their par value.

Since this is how most new shares are issued investment trusts should usually have enough in their share premium account if they need to fund a buyback.

THE PROS AND CONS OF BUYBACKS

When a buyback is used to purchase shares at a discount to NAV and cancel them, the NAV per remaining share increases.

This can also reduce the volatility of the shares and the volatility of the discount although it means there is less liquidity as there are fewer shares in issue.

It also means that ongoing charges increase as the investment trust’s fixed costs are spread over a smaller number of shares.

As William Heathcoat Amory, head of investment trust research at Kepler Trust Intelligence points out, this combination is actually counter-productive: ‘As the trust becomes smaller and the charges become larger the discount may widen further as the shares are considered less attractive’

If a buyback is used to try to reduce the influence of large and potentially hostile shareholders, there is a risk that those shareholders refuse to take part in the buyback and their share in the investment trust increases.

‘Share buybacks are not a panacea for all of investment companies’ problems and will not work if there is no demand for a company due to sustained poor performance or other concerns. They also do not work when an investment company is invested in illiquid assets,’ adds Brodie-Smith.

TENDERS AND PARTIAL OFFERS

If an investment company wants to buy back between 15% and 30% of its shares then it needs to make a tender offer.

These can be at a fixed price or a maximum price but either way they must be in cash and must be available to all shareholders.

Offers must be advertised in two national newspapers for at least seven days and all need approval from the Takeover Panel which rules on takeovers and mergers to ensure fair treatment for shareholders.

Partial offers are similar to tender offers but they can be for more than 30% of the company’s shares and they are not limited to cash.

LIQUIDATION AND CONTINUATION VOTES

In extreme situations where the discount to NAV can’t be reduced sufficiently, the running costs are disproportionately high or the investment trust has ceased to serve its purpose, the board could decide to liquidate the company.

For many small funds with large discounts to NAV and high costs, buybacks and tenders are no help as they will just increase their costs per share so liquidation may be the best option.

At the same time investment trusts usually have a provision which allows shareholders a say in whether the trust should continue trading. This is known as a ‘continuation vote’ and is normally triggered after a certain period of time, for example three years or five years after the fund is launched.

From this point shareholders are able to vote regularly on whether or not the trust should be wound up, the assets sold and the cash returned to them.

‘Continuation votes are useful in more specialist or esoteric asset classes which may move in and out of favour and suffer prolonged periods of poor performance,’ explains Brodie-Smith.

EXAMPLES OF TENDER OFFERS

One investment company which regularly buys back its own shares is Aberdeen Emerging Markets (AEMC).

In February 2018 it announced its fourth tender offer in five years for up to 10% of its shares at a discount of 3.5% of NAV to narrow the discount which at the time was above 10%.

In the event over 80% of the shares were tendered so it had no problem buying back what it wanted.

Edinburgh Dragon Trust (EFM), also part of the Aberdeen stable, plans to tender for up to 30% of its shares at a 2% discount to NAV before the end of January 2019. The tender could be popular as the current discount is also in the region of 10%.

GOING, GOING, GONE

Despite raising the dividend by 80% last year in the hope of surviving a continuation vote, the board of Lazard World Trust Fund (WTR) got a resounding thumbs down from shareholders in September as they voted to liquidate the trust.

Last month Lazard announced that it would effect ‘a managed wind-down of the company’ so as to ‘realise its assets in a controlled and orderly manner’.

In an unusual turn of events, the boards of two smaller investment companies, Establishment (ET.) and Juridica Investments, recently recommended that shareholders vote to wind them up.

Establishment, whose market value had shrunk to just £40m in mid-November, blamed its decline on its large exposure to Asia and admitted that keeping the trust going was ‘not an attractive option for shareholders’.

Analysts at stockbroker Numis says ‘performance has been poor, with the NAV up just 20% over the past five years versus 65% for the MSCI World Index’. They believe Establishment may seek to appoint a new manager to grow the fund via a different mandate, rather than disappear altogether.

Juridica, which invested in corporate claims litigation, recommended liquidation as ‘the costs to shareholders of continuing the company in operation’ were ‘outweighed by the benefits of winding up’. It delisted from AIM in December.

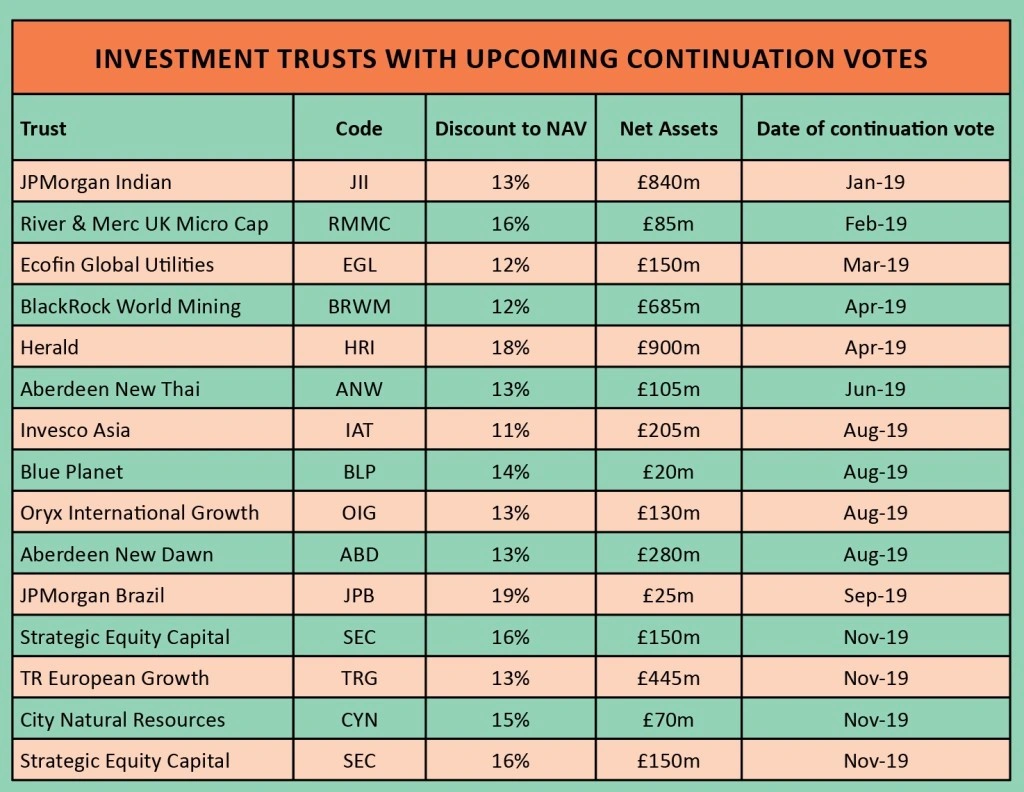

TROUBLE AHEAD?

Research house Numis has compiled a table of investment companies with sizeable discounts to NAV where continuation votes are due this year. We publish the list in full in this article.

Many are below £100m in value, which is increasingly considered sub-scale these days, and may come under pressure from their shareholders.

Numis flags Aberdeen Frontier Markets (AFMC), Aberdeen Latin American Income (ALAI), Baring Emerging Europe (BEE), Jupiter Green (JGC) and Jupiter UK Growth (JUKG) as looking vulnerable.

Even some larger funds which suffer persistent discounts or long-term under-performance could come under pressure according to Numis.

Edinburgh Investment Trust (EDIN), which has a market value of £1.25bn and takes a ‘value’ approach to investing, has posted negative share price and NAV returns over the past year and faces ‘a crucial year in terms of maintaining investor confidence’.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.