Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineChanges at Tracsis but the growth story remains the same

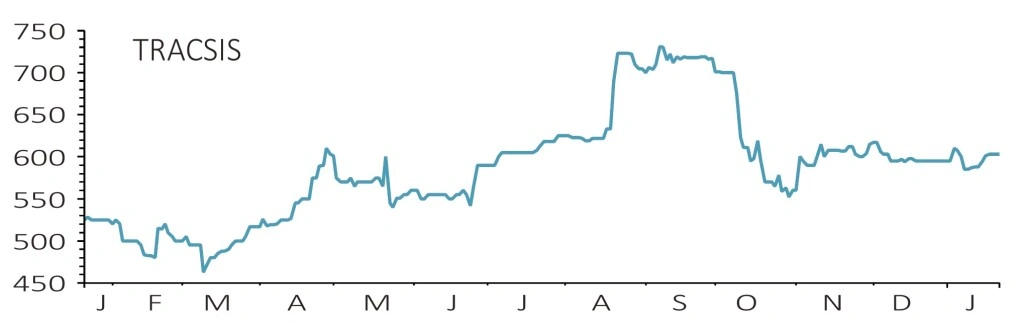

TRACSIS (TRCS:AIM) 603p

Gain to date: 17.1%

Original entry point: Buy at 515p, 22 February 2018

Quite a bit has happened since the start of the new year at Tracsis (TRCS:AIM) with the acquisitions of Compass Informatics and event traffic planning provider Cash & Traffic Management recently signed off.

These will bolster the Traffic and Data Services (TDS) part of the transport technology and analytics company, bringing extra scale, some new clients and offering good cross-selling opportunities. Both are classic Tracsis buys, relatively inexpensive, with solid profitable growth and recurring revenue.

This is important since TDS is the lower margin bit of the company, with earnings before interest, tax, depreciation and amortisation (EBITDA) margins of 12.5% last year. That compares to roughly 36% margins earned on Rail Technology and Services (RTS), the other part of the company.

But trumping that was news earlier in January that chief executive John McArthur is standing down. This is undoubtedly a blow since he has created huge value for shareholders in the 10-plus years on the stock market. The stock floated at 40p.

Ricardo (RCDO) executive Chris Barnes will take the company forward from 4 February, with a suitable handover period planned.

That McArthur will still be around in a consultancy capacity to help on future acquisitions is highly reassuringly that despite the management change, Tracsis will be sticking very much to its growth knitting.

SHARES SAYS: Still a long-term buying opportunity.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.