Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe importance of investment style when picking funds

When it comes to choosing an investment fund there are a number of things to take into account: fees, track record and the assets and regions it invests in, to name just a few. But also worth bearing in mind is the investment style that a manager uses.

Investment style determines which assets are most likely to make it into a fund’s portfolio and influences when it is likely to outperform and to underperform.

GROWTH AND VALUE

Investors tend to follow two main camps: growth and value. Growth stocks are those which are those which are growing. Value stocks are those which look to be good value, often because they are out of favour with other investors, sometimes for good reason.

Some funds do not have a distinct style but often a manager will favour one of these approaches. In some cases, entire investment houses have a bias towards a particular strategy.

WHEN DOES GROWTH DO WELL?

Growth investors tend to thrive in a bull run, when markets are rising and share prices are going up.

The danger here is that an investor may overpay for a stock in the belief it will continue on its upward trajectory, only for there to be a market correction or for the share to plunge.

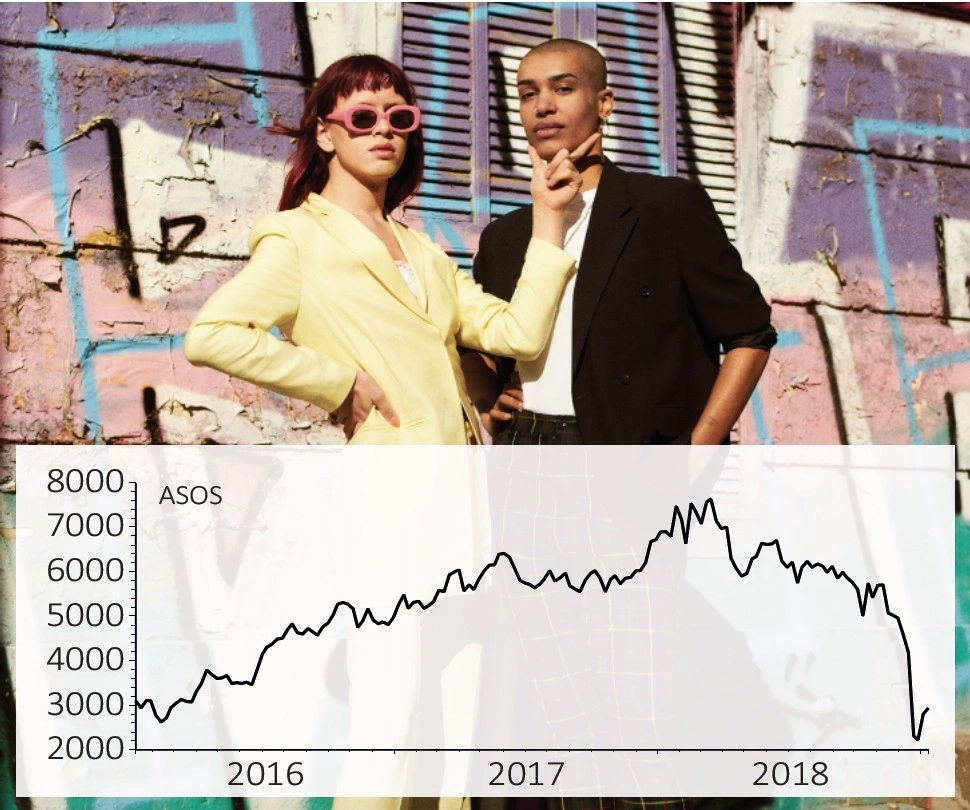

One recent example is online fashion retailer ASOS (ASC:AIM), whose shares had soared for years until a slip in growth forecasts in December saw the stock plunge by 40%.

Thomas MacMahon, senior analyst at Kepler Partners, says: ‘Ultimately, growth investing makes sense if you believe you can identify which companies can generate the highest growth rates on their earnings.

‘If this is the case, a fund should outperform as the value of stocks it invests in should rise at a faster rate than the value of the stock market as a whole.’

He says Jupiter European Opportunities Trust (JEO) is an example of growth investing. The fund invests in names such as sportswear brand Adidas and German stock exchange Deutsche Boerse, and has returned 27% over three years.

OTHER INVESTMENT STYLES

Under the heading of growth, there are some more specific styles as well. For example, ‘growth at a reasonable price’ is a more price-sensitive version of growth investing. MacMahon explains: ‘Managers aim to pick the stocks with the best growth prospects, but are stricter about the valuations at which they will buy and sell.’

Fund Expert managing director Brian Dennehy likes momentum investing. This follows the idea that investments which have done well for a while should continue to do well in the future.

He says: ‘Applying this process to pick funds in the UK All Companies sector since 1994 has generated an extra return of 6% a year. You didn’t do anything clever to achieve that, you just had to have a clear process for selecting funds and do it consistently.’

Nothing keeps going up forever and this style may suffer when the momentum stops. MacMahon adds: ‘Growth investing involves forecasting future demand and developments, which is difficult to do well consistently.’

Fund managers who adopt momentum techniques in their investing include Austin Forey, manager of investment trust JPMorgan Emerging Markets (JMG), and Harry Nimmo, manager of Standard Life UK Smaller Companies Trust (SLS).

MacMahon says: ‘Nimmo won’t buy into his picks when they sell off; he waits for the dust to settle and for some upward momentum to begin before adding to a position. Both managers are essentially growth investors with momentum being a secondary element to their style.’ The funds have returned 74% and 12.6% over three years respectively.

WHAT DO VALUE INVESTORS LOOK FOR?

Value investors look to take advantage of mispriced stocks. Within this camp, some managers take a recovery approach, picking out those stocks which look to be on the brink of a turnaround, while special situation investors look for one-off events which have adversely affected sentiment towards a stock.

Value investing doesn’t have to mean picking out future winners but can simply be a case of finding instances where the market is being too gloomy about a company’s prospects, or perhaps an entire sector is suffering because of one firm’s failings. You buy with the hope that the shares re-rate to a higher valuation.

Dennehy adds: ‘This isn’t about simply buying what is cheap, but buying what is unjustifiably cheap. This requires a manager to have the skill to analyse financial accounts, the patience to wait until the market reflects your analysis, and the discipline to not get distracted by market woes along the way.’

EXAMPLES OF VALUE INVESTING FUNDS

Value investing styles are central to such open-ended funds as M&G Recovery (B4X1L37) and Schroder Recovery (B3VVG60), which have returned 16.9% and 35.6% respectively over the past three years, according to Morningstar data.

In the investment trust universe, MacMahon likes Keystone Investment Trust (KIT), run by James Goldstone, who is currently finding opportunities in unloved UK banks and insurers. He thinks investors are irrationally negative about the short-term risk of Brexit to the sector. The fund is down 2.3% over three years, highlighting how choosing out of favour stocks can result in periods of underperformance.

The value investing strategy has a number of risks; sectors or stocks can remain cheap for a long time, or they may turn out to be so-called value traps, whereby the stock was cheap for good reason but an investor has been lured in by its cheap price.

MacMahon says: ‘Ultimately both growth and value investment styles include the same element – analysing the valuation of an investment and making a judgment about its growth prospects – but they weight those elements differently.’

EXAMPLES OF INVESTING STYLES FOUND IN FUNDS AND INVESTMENT TRUSTS

Growth

Growth at a reasonable price

Value

Momentum

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.