Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBuy BAE Systems for steady growth and tasty dividends at an attractive price

Shares in defence firm BAE Systems (BA.) have fallen by 25% over the past six months, creating an attractive buying opportunity. We think some of the concerns which have weighed on the share price are overdone and would look to full year results on 21 February as an early catalyst for the stock to recover. Buy ahead of that event.

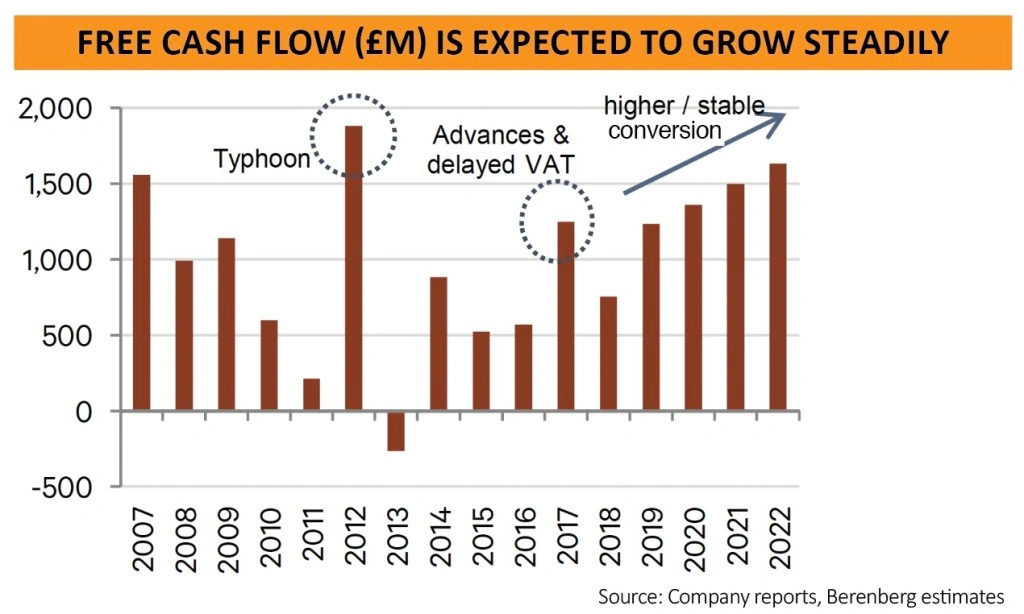

The weakness in the shares has left them trading on a 2019 price-to-earnings ratio of 11.2-times, below the 20-year average of 11.5-times. They also offer a prospective dividend yield of 4.6% backed by robust and improving cash generation.

Investment bank Berenberg says: ‘BAE is entering a period of low but steady growth underpinned by long-term programmes. Favourable mix from higher-growth US activities should drive growth in earnings per share of around 6% a year.’

We think this ‘steady growth’ at an undemanding valuation is likely to prove attractive to investors, particularly given the company’s relative insulation from Brexit.

It has very limited direct trade with countries in the European Union and as a low volume producer of expensive and high-tech kit for the defence industry, it is not as reliant on just-in-time supply chains as other industrial firms.

WHAT DOES IT DO?

BAE Systems was formed in November 1999 by a combination of British Aerospace and Marconi Electronic Systems.

British Aerospace itself came into being through the nationalisation and merger of several UK aerospace and defence firms in 1977 while Marconi Electronic Systems was spun out of UK industrial conglomerate GEC.

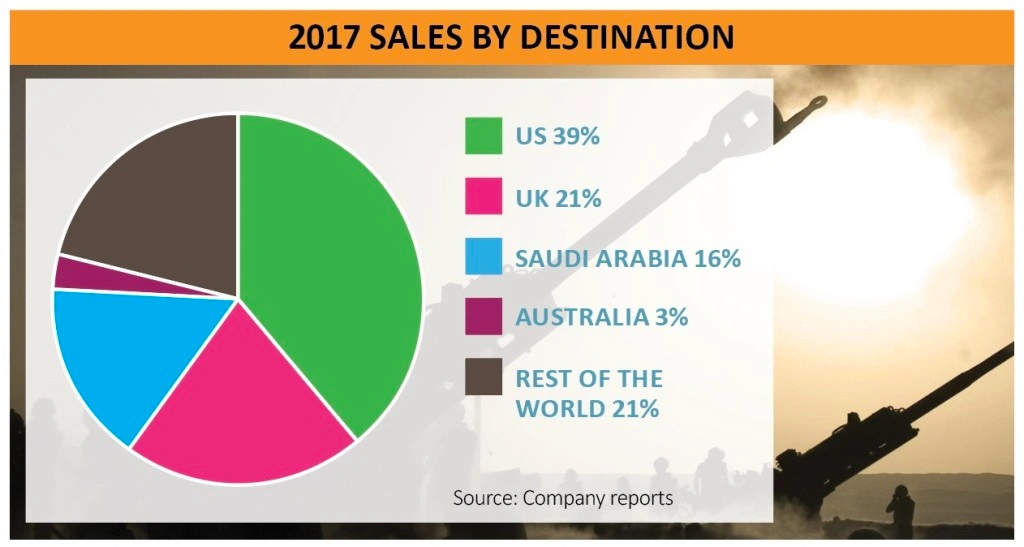

Despite this strong British heritage and a still-dominant position in the UK, today the company has a truly global horizon. It is a top-six supplier to the US Department of Defense and has a big footprint in several international defence markets including Saudi Arabia, Australia and India.

The company’s operations span the defence sector and include the design, manufacture, upgrade and support of combat aircraft, land vehicles and ships as well as offering engineering, commercial, financial and human resource services, electronics and, increasingly, cyber security.

The company secured several significant new orders in 2018 which should support sales over the long-term. These included a £5bn order from Qatar for 24 Typhoon fighter jets and nine Hawk advanced jet trainers.

BAE was selected to deliver Australia’s nine-ship SEA 5000 programme based on its anti-submarine Type 26 frigate, which was also chosen for the Canadian Surface Combatant programme.

It was picked by the US Marine Corps to deliver its amphibious combat vehicle, in a contract initially worth a relatively modest $198m but with options which could increase the size of the opportunity materially over time.

In the UK, in addition to ongoing funding for the Astute submarine programmes, BAE received around £600m for continuing design and development work on the nuclear successor submarine programme.

With several of these awards linked to major programmes, which are less likely to be cut, delayed or cancelled, and around 45% of the company’s sales derived from services and support work, we think there is decent visibility on future revenue growth.

WHAT ARE THE MAIN RISKS FACING THE COMPANY?

A key area of uncertainty lies around the £10bn follow-on order of 48 new Typhoon jets from Saudi Arabia. The deal was green-lit in March but has not been finalised. The spotlight is currently on Saudi Arabia over the killing of journalist Jamal Khashoggi in October 2018, and this may delay progress here.

The company’s other support and maintenance work in the country, though it is fairly entrenched, could be threatened if there is a change of government in the UK given Labour leader Jeremy Corbyn’s call for a suspension of Saudi Arabian arms sales.

These are some of the risks prospective investors in the company need to weigh. Another one is pressure on defence spending in the US and UK. However, the company looks relatively well positioned thanks to a focus on major equipment orders in the UK where the Ministry of Defence has limited scope to bin contracts, and areas of potentially significant growth in the US, including in weapons systems and electronic warfare.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.