Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBig deals mean gold may still have lustre

The investment decisions that generate the best returns are rarely the most comfortable or easy ones, and few asset classes generate such strong feelings as gold.

Some investors will be inclined to share the view of economist John Maynard Keynes that the precious metal is a barbarous relic. Others will warm to legendary investor Warren Buffett’s view that gold has no intrinsic value, on the grounds it has no practical use and generates neither yield nor cash.

Some will warm to it as a potential port in a storm, remembering how well it performed during the economic downturns of the 1970s, early 2000s and 2007-09.

One thing that no-one can deny is that gold – along with German government bonds – was just one of two major asset classes that generated positive total returns in sterling terms in 2018. Since the FTSE All World index peaked in September, that stock index has lost 11% while gold has risen by $90 an ounce, or 7%.

This begs the questions of whether the positive run can continue and whether investors need to be pondering once more whether gold can be a useful provider of portfolio diversification.

THE CASE FOR GOLD

Two factors may speak in gold’s favour. The first is that it seems unloved.

Anecdotally, this column never gets a question about it. (Compare that to say bitcoin a year ago).

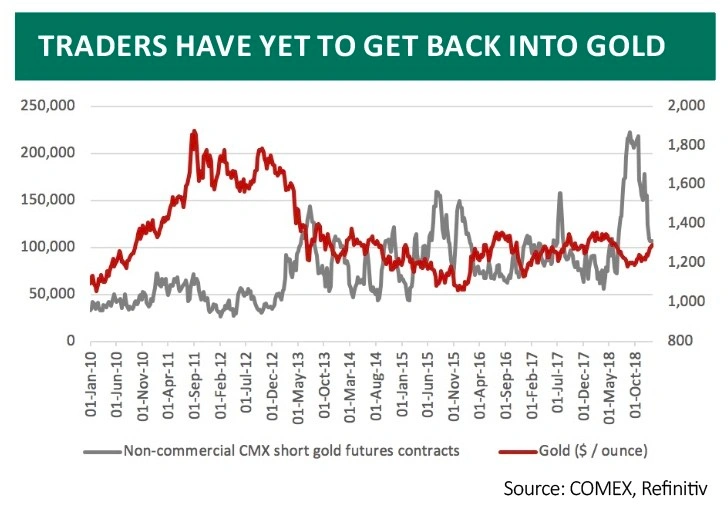

More tangibly, figures from CME show that non-commercial futures positions on its derivatives marketplace in the US still mean traders have a net short position.

While the number of shorts has dropped from a high of 222,210 contracts in August to 106,028 in December (the last number released before the US government shutdown) this suggests that sentiment is still washed out, something that makes gold’s recent advances back toward $1,300 an ounce all the more intriguing.

The second is that while stock market investors do not seem interested in gold or shares in gold miners, the miners themselves are becoming active.

No sooner had America’s Barrick Gold merged with former FTSE 100 member Randgold Resources in a $6bn all-stock deal, this week (14 Jan) Newmont Mining has swooped for GoldCorp in a $10bn cash-and-stock deal.

The timing is interesting. A comparison of America’s HUI Gold Bugs index relative to the gold price suggest that gold miners look cheap relative to the metal.

THE CASE AGAINST GOLD

Two factors still speak against exposure to gold. The first is Buffett’s argument about its lack of yield or cash-generative capabilities. It remains a play on market psychology and many investors will conclude that trying to second-guess that is a mug’s game.

The second is the US Federal Reserve. Gold soared between 2009 and 2012 because the central bank had embarked upon quantitative easing (QE) and markets feared it had lost control. That does not seem to be the case right now.

The Fed has raised interest rates nine times to 2.5%, which makes gold’s lack of yield seem even more of an issue, and embarked upon quantitative tightening. Under such circumstances, it seems like the Fed is in control.

POTENTIAL CATALYSTS

Two swing factors may decide where gold (and thus gold mining stocks) go from here.

The first is central bank policy. There is no indication that the Fed is considering a cut to interest rates or a return to quantitative easing. If prevailing fears over economic weakness or policy becoming too tight then gold will doubtless be cast aside as a ‘barbarous relic’

once again.

But if the Fed does turn tail, cut rates or even sanction a return to QE then the precedent of 2009-2012, after the launches of the first two rounds of QE, would suggest that investors could look to gold as a haven and store of value in the face of yet another round of ultra-loose, unorthodox monetary policy.

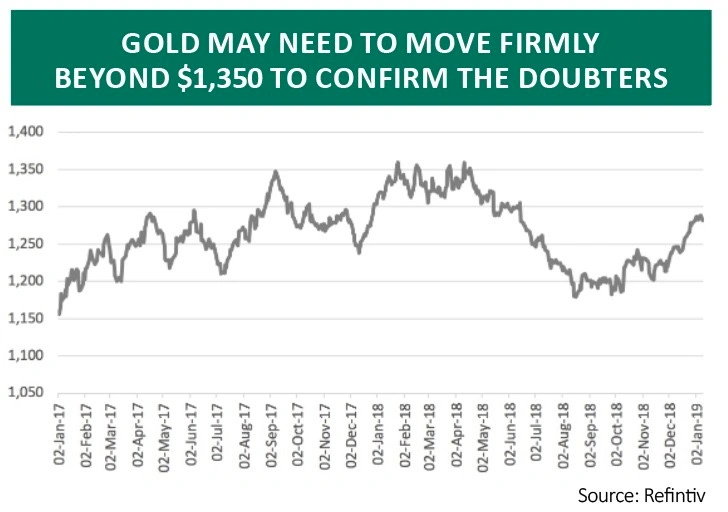

The second is technical. A move above the $1,350 to $1,400 an ounce level, which the metal has failed to crack on five occasions since the start of 2017, would really encourage gold bugs. Equally, any failure to make a sustained breakthrough would challenge the bull case

for the precious metal.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.