Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineUse Keystone Investment Trust to make the switch to value investing

Experts increasingly believe value investing will come back into fashion and Keystone Investment Trust (KIT) looks an excellent product to buy ahead of the anticipated trend switch.

Don’t put be off by its past performance – the trust has fallen in value in the past year – as buying Keystone is a bet on the market looking for different things in 2019.

Investing in growth companies, even some on very high valuations, has been the winning strategy for a considerable number of years.

This year we’ve seen many of these growth stories start to de-rate which means they trade on lower price-to-earnings multiples. This is partly down to rising bond yields which tend to depress the multiple investors are willing to prescribe to corporate earnings.

It therefore seems logical that value investing could start to become more fashionable. This is buying companies that trade below their intrinsic value.

Analysts at Morgan Stanley, in particular, say they have a strong preference for value over growth going into the New Year ‘as we think that we are only at the start of a long-term style trend reversal’.

A DOUBLE HIT OF CHEAPNESS

Invesco-run Keystone is currently trading 11.3% below its net asset value (NAV) which means you buy access to a portfolio for less than the value of its underlying holdings – many of which are also considered to be trading too cheaply.

Investors must appreciate there is no guarantee that value investing will be a winning strategy in 2019 and therefore buying Keystone won’t necessarily result in near-term gains. You also have to consider that parts of its portfolio are UK domestic earners which

have been out of favour due to concerns on how Brexit will play out.

However, if we are right that value investing will win in 2019, you may see a rise in the share price driven by investors bidding up value strategies, plus a narrowing of the investment trust’s discount to NAV.

There is also a potential extra kicker if there is a positive resolution to Brexit and investors around the world start to have renewed faith in UK equities, which is Keystone’s focus.

WHAT IS KEYSTONE’S APPROACH?

James Goldstone took over the running of Keystone from highly-respected Invesco fund manager Mark Barnett in April 2017. The investment trust aims to maximise total return through a value-based strategy focused on cash flow and dividends, which results in a higher yield than a typical growth fund. At the moment it is yielding 3.8% according to Morningstar data.

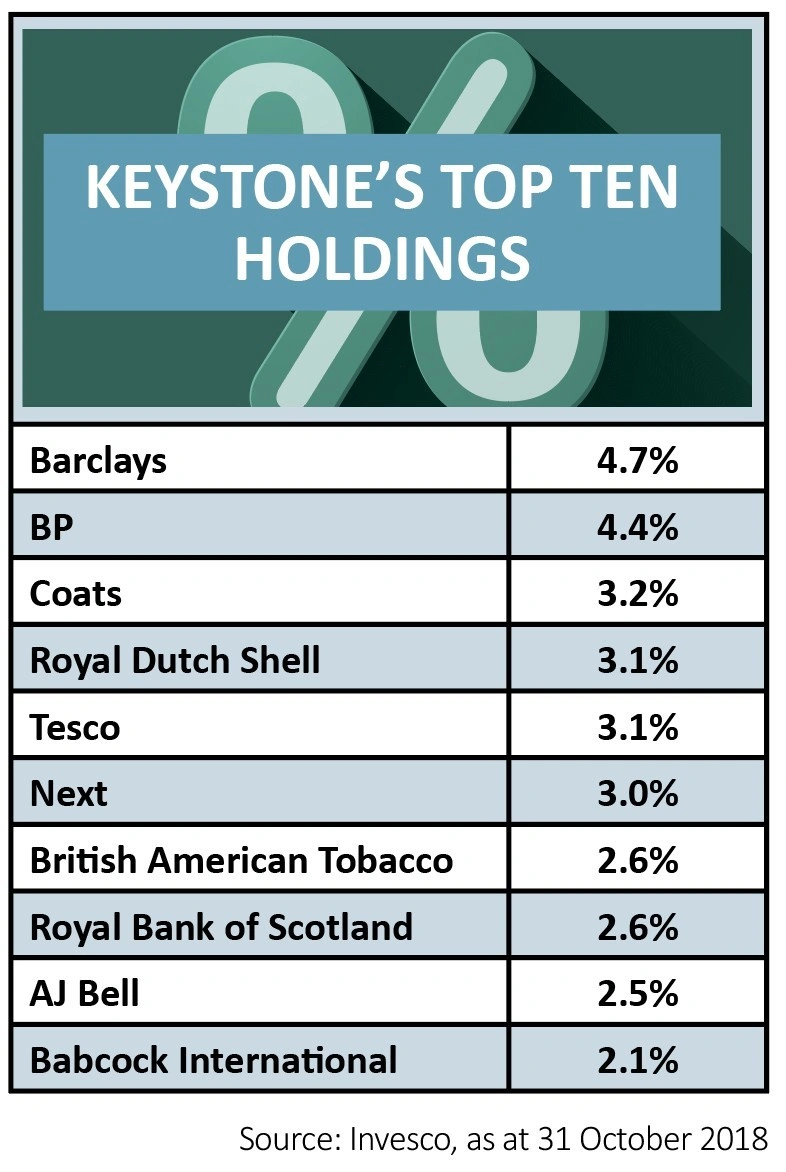

Goldstone seeks to provide shareholders with long-term capital growth from a diversified portfolio of between 50 and 80 investments. Holdings include oil producer BP (BP.), information and analytics company RELX (REL), carpet manufacturer Victoria (VCP:AIM) and retailer JD Sports (JD.).

The fund manager favours companies with strong balance sheets, high barriers to entry and the ability to expand market share, traits he believes help to underpin long-term capital and income growth.

HOW THE PORTFOLIO HAS CHANGED

‘I’ve made some significant changes (since inheriting the trust in 2017),’ says Goldstone. ‘The main things I’ve done are to reduce tobacco and healthcare and I’ve used that to fund a move into financials including banks and more recently, some domestic cyclicals,’ he informs Shares.

‘The portfolio has moved further towards value and if I think about my approach to investment, it is very valuation focused. I try to be contrarian on the basis that if you are going against the flow, the chances are you are going to pick up something on a more attractive valuation than when everybody thinks this is great. And then beyond that it is really about risk/reward,’ he adds.

Goldstone will pay up for quality companies with strong track records, sustainable growth, cash generative business models and progressive dividends, and ‘the right balance sheet’ where the valuation is attractive.

HOW KEYSTONE GETS AN EDGE

Keystone investors benefit from the fund manager’s regular interaction with the people running companies, spanning from small caps to FTSE 100 behemoths.

‘The most interesting five minutes of a meeting are where you are getting into their capital allocation framework,’ explains Goldstone.

‘Retailer Next (NXT), bought on a free cash flow yield of over 10% in early 2017, is the poster child for capital allocation in the FTSE 100. It has been extremely cash generative for the last 20 years and rather than waste that on vanity projects or M&A and not allocate capital properly, it has consistently returned that capital to shareholders over time both through dividends and share buybacks.’

Given myriad macro uncertainties, Goldstone hopes the modest average valuation of the bulk of the holdings and the defensive characteristics of gold – 5.5% of the portfolio is exposed to the precious metal – will combine to produce a portfolio with compelling risk/reward characteristics in the years ahead.

The trust has positions in five profitable, cash-generative gold miners including Randgold Resources (RRS) – which

is about to merge with Barrick and together will be the world’s largest gold miner – Newmont Mining, Endeavour Mining, Acacia Mining (ACA) and Agnico Eagle.

Investment bank UBS forecasts that gold will rise to an average of $1,300 per ounce in 2019 (2018 forecast: $1,270) before moving even higher to $1,325 in 2020.

DISCLAIMER: Keystone Investment Trust has a holding in AJ Bell which is the owner of Shares magazine. The author of this article also holds shares in AJ Bell.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.