Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe best performing shares of 2018: quantifying the reasons behind their success

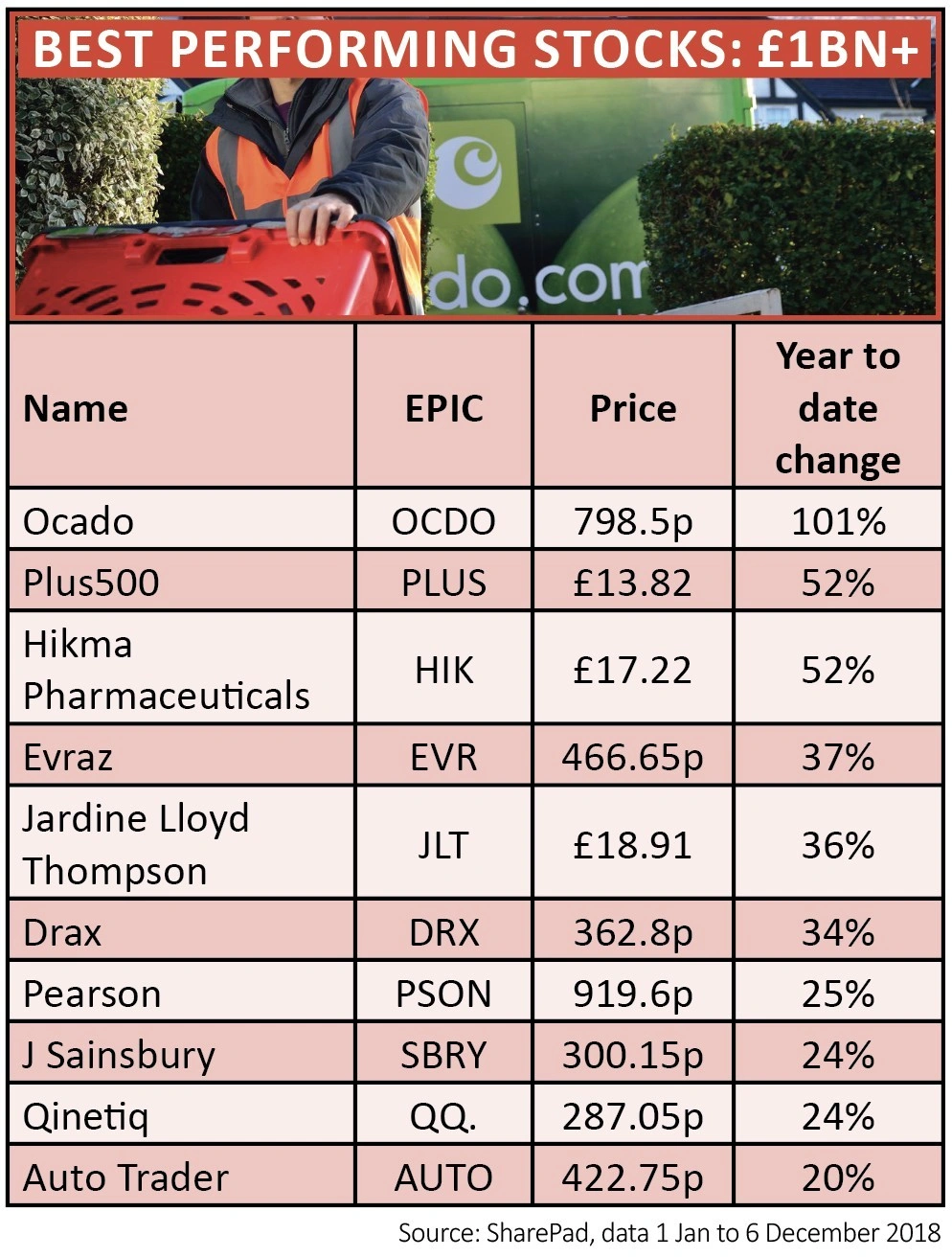

MARKET CAP: £1BN & ABOVE

OCADO +101%

Shares in Ocado (OCDO) have doubled in value in 2018 as the company made progress with signing international contracts where it sets up large distribution centres to enable online grocery services.

Building on a 2017 tie-up with France’s Groupe Casino, Ocado has this year signed deals with Canada’s Sobeys, Sweden’s ICA and most significant of all, with US groceries giant Kroger, which could transform the US food retail market.

Bulls believe Ocado’s end-to-end solution for operating online grocery businesses has the potential to become the standard platform for international retail logistics.

For all the hype, Ocado remains in a growth phase requiring heavy investment spend and it still doesn’t generate material earnings. Shore Capital says: ‘Ocado’s stock has been a bit of a rollercoaster to date with risible capital returns. We know that the capital continues to be expended; as for the returns, well who knows.’

PLUS500 +52%

it would have been a bold move to buy shares in Plus500 (PLUS) at the start of this year considering that UK and European regulators at the end of 2017 vowed to crack down on derivative platforms marketing to retail investors.

The fact that the shares had already gained 160% last year, ranking second in our ‘Best Performers of 2017’, makes this year’s returns even more surprising.

Yet just as last year, the company has raised guidance with each earnings update helped by an increase in higher lifetime-value customers and a backdrop of heightened market volatility which encourages them to trade more.

The firm even cautioned at the half year stage that it wouldn’t be able to sustain its run of form to the end of the year, but in mid-October it admitted it would probably beat expectations.

It seems unlikely that Plus500 can repeat the trick for a third year given that the new rules are clearly impacting revenue growth so despite its high operational gearing profit growth will inevitably slow in 2019.

HIKMA PHARMACEUTICALS +52%

Pharmaceutical company Hikma (HIK) saw its shares rise in 2018 as its strategy to boost sales paid off.

It is fair to say that 2017 was a disappointing year for the drug developer after it was forced to cut sales guidance three times amid challenging conditions in the US.

Hikma subsequently revived trading in 2018 thanks to strong product demand and its extensive pipeline, prompting it to hike earnings guidance for its generic and injectables businesses in August.

Cantor Fitzgerald analyst Brian White notes that pressure in the generics business has persisted, but pricing in the US is stabilising. ‘We expect Hikma to focus on margin delivery and the potential for bolstering the pipeline through acquisition and collaboration’, he adds.

PEARSON +25%

The recovery in 2018 from publishing firm Pearson (PSON) followed a tricky run for the share price which fell from highs of around £15 in 2015 to a trough a little over 550p a year ago.

The company has faced structural headwinds as demand for the expensive academic textbooks it sells has fallen away in a more digital world, contributing to a string of profit alerts.

Signs that the company is beginning to face up to this transition while keeping a tight control on costs excited the market this year.

Contrarian investor Alex Wright, who steers Fidelity Special Values (FSV), has previously said that in time Pearson will be viewed as a tech company, not a text book company.

A third quarter trading update (17 Oct) confirmed the company was on track to deliver £300m of annualised cost savings, with the full benefit felt from the end of 2019 onwards, and full year profit guidance was reaffirmed.

MARKET CAP: £500M TO £1bn

CRANEWARE +83%

If you believed the mass media you might think California’s Silicon Valley and the FAANG stocks had the exclusive right to technology growth excellence. You would be wrong.

Craneware (CRW:AIM) is a made-in-Britain company that dominates its niche, earns only recurring revenues, on average five-year contracts, and enjoys an entrenched competitive position at the top of its industry.

It provides billing and healthcare analytics software to almost a third of the hospitals in the US. The company estimates it can help an average 350-bed hospital tap an extra $22m a year of revenue currently missed out on.

It uses automation to identify new income opportunities to healthcare management as well has highlight operational and financial risks.

There is no single reason behind the shares’ 2018 performance, but Berenberg analysts say about Craneware: ‘Few companies can combine software which generates significant value for its customers, an addressable market in the hundreds of billions, excellent revenue visibility and a growing annuity base of high margin, cash-generative software-as-a-service contracts.’

GENEL ENERGY +71%

In recent years oil play Genel Energy (GENL) has been beset by reserve downgrades, geopolitical issues and management changes. Life was more stable in 2018 as the company focused on delivering cash flow from its fields in Kurdistan, a semi-autonomous region of northern Iraq.

The company achieved free cash flow of $119m in the first nine months of 2018 and has moved from a substantial net debt to a positive net cash position.

A better-than-expected contribution from its Peshkabir field has been a significant factor. The company is also advancing plans to develop its other assets in Kurdistan, including the Miran natural gas field, while making tentative moves with its exploration portfolio in Africa.

The company has displayed good discipline with operating expenditure guidance recently trimmed from $30m to $25m and capital expenditure at the lower end of the expected range in 2018.

At 181.8p its shares are still a long way from the highs above £11 seen in early 2014.

HURRICANE ENERGY +34%

Everybody was excited when Hurricane Energy (HUR:AIM) made one of the largest recent discoveries in the North Sea with its Lancaster find in 2014, particularly after its potential was proved up by follow-on drilling.

The subsequent questions were all centred on how the development of this prized asset and the drilling of other targets in the group’s portfolio would be funded.

These questions are now some way to being addressed with the company moving closer to first cash flow from an early production system on the Lancaster field. This milestone is expected in the first half of 2019.

Hurricane Energy’s plans to advance the Greater Warwick Area were aided by a $387m farm-out agreement with Spirit Energy with drilling expected to commence in the first quarter of 2019.

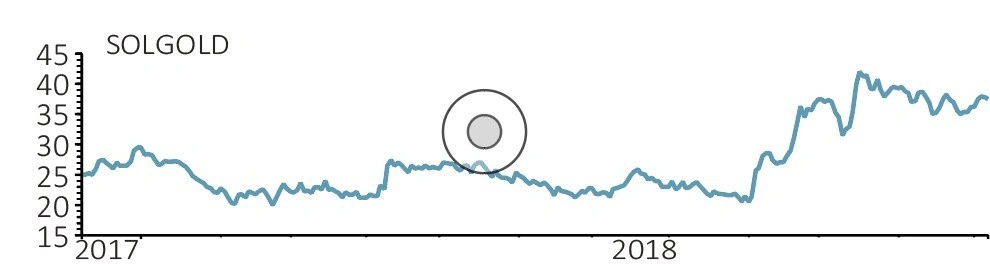

SOLGOLD +28%

Shares in copper explorer SolGold (SOLG) were looking a bit sleepy for the first nine months of the year as it ploughed on with drilling at its Alpala prospect in Northern Ecuador. The share price burst to life in September when FTSE 100 miner BHP (BHP) acquired a 6.1% stake in the business, picking up the shares from Guyana Goldfields which sold out completely. A month later BHP invested £45m for more shares, taking its stake to 11.18%.

In 2017 BHP tried to cosy up to SolGold by proposing to invest money to earn up to a 70% stake at the project level and on its own terms. SolGold rejected the proposal as it didn’t want to give away that sort of upside.

The two companies are now getting on famously as BHP has invested at the plc level, at a premium to the market price, and on agreed preferable terms to SolGold.

While the miner is years away from thinking about developing the project into a commercial entity, there is ongoing speculation that BHP will ultimately be the owner and operator, assuming SolGold continues to prove up large amounts of copper.

EI GROUP +27%

The UK’s largest pub company EI Group (EIG) has ramped up progress with its transformational strategy and its share price has done very well given a challenging backdrop for consumer-facing companies.

EI has been reaping the benefits of people opting to drink rather than dine out as its pubs are generally wet-led.

The company is finally finding its feet again after struggling with huge amounts of debt during and after the global financial crisis.

A possible catalyst in 2019 is the potential sale of its Commercial Properties portfolio for an estimated £300m, which may leave the company in healthier shape by further cutting debt.

Canaccord Genuity analyst Nigel Parson says the sale could lead to a special dividend for shareholders.

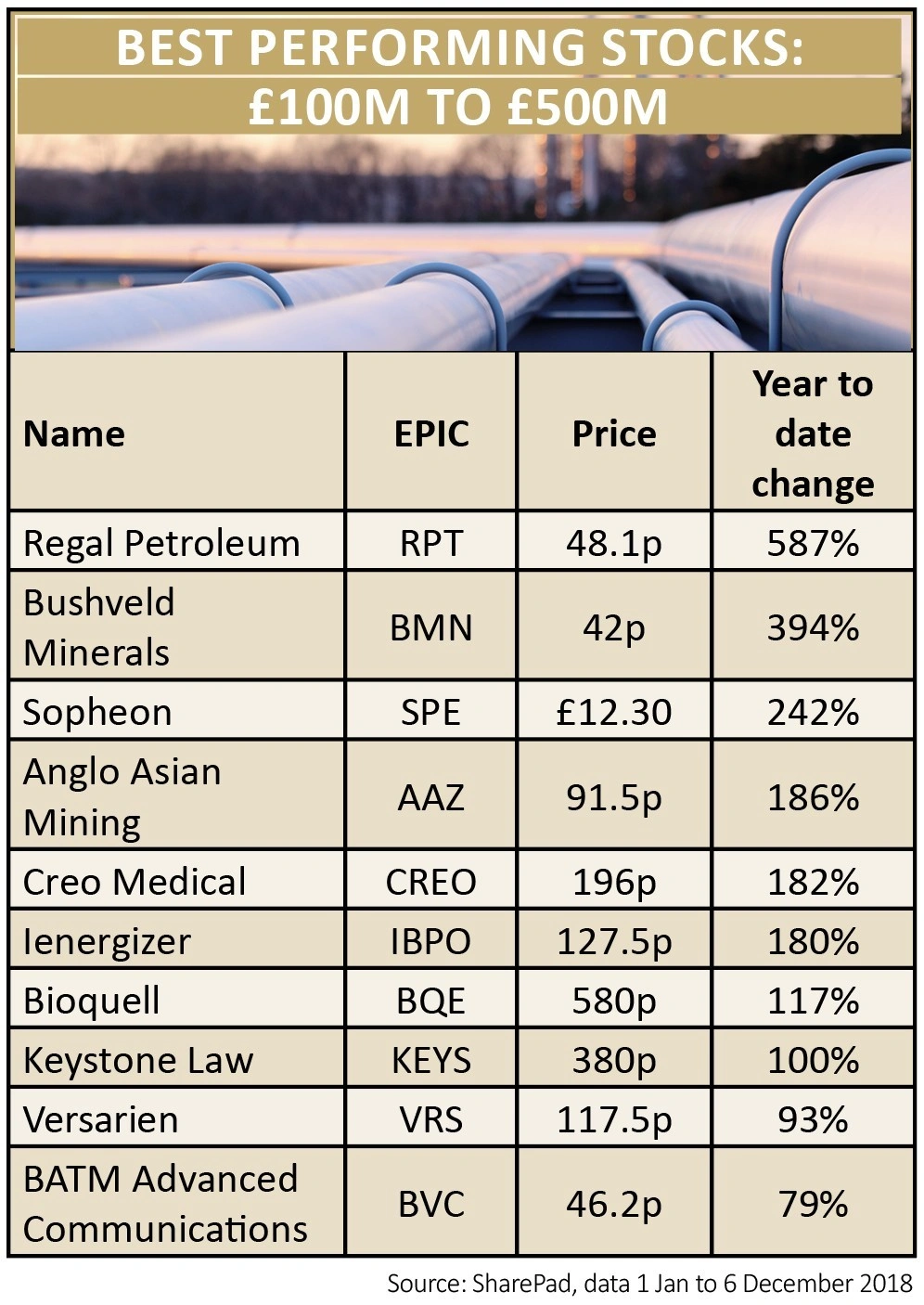

MARKET CAP: £100M TO £500M

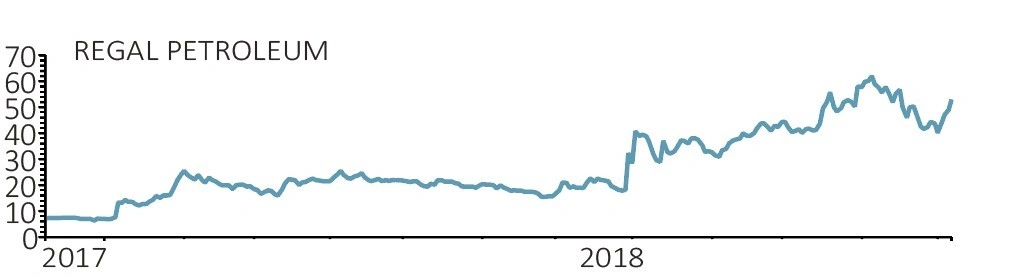

REGAL PETROLEUM +587%

Ukrainian natural gas producer Regal Petroleum (RPT:AIM) surged higher in 2018 after a period of stasis with new and supportive legislation in the country relating to the oil and gas sector providing a catalyst.

The company’s financial performance improved with first half revenue doubling and the business swinging from a loss to a net profit year-on-year.

This was underpinned by increasing production and the company says it is now in a position to fund its development plans from cash flow and existing cash resources which totalled $40m at the last count.

The shares have also been supported by speculation over corporate activity with a vehicle apparently owned by Ukrainian billionaire Victor Pinchuk buying 24% of the company.

Pinchuk was behind a failed bid in 2011 when he lost out to Regal’s current shareholders Vadim Novinsky and Andrei Klyamko who gained control of the business and still hold a 52% stake.

As a natural gas focused producer, the company has been largely insulated from the recent volatility in the oil price which has seen a fall from $85 per barrel to less than $60 per barrel in a matter of weeks.

BUSHVELD MINERALS +394%

Talk about a radical transformation. For years Bushveld Minerals (BMN:AIM) was a bewildered multi-commodity business dabbling in vanadium, titanium, tin and coal. Investors weren’t really interested as many of the relevant commodity prices were in the doldrums and exploration projects were completely out of fashion.

Fast forward to the end of 2017 and everything changed. Bushveld went from being a minority shareholder in the Vametco vanadium mining operation to a 59.1% owner (since increased to 74%). That meant Bushveld was seen as a proper operating business rather than an explorer and investor.

All this happened against a backdrop of soaring vanadium prices, helping to explain why its share price has done so well.

Bushveld believes it can improve productivity to further enhance earmings.

SOPHEON +242%

Companies that develop a habit of beating expectations will sooner or later start seeing that reflected in a rising share price, and this trend certainly applies to research, development and product lifecycle tools designer Sopheon (SPE:AIM).

This is the second time Sopheon stock has put up eye-popping performance, having shot from 63p to 352p in 2016.

Success in 2018 really stems from the broader industry segment appeal for its Accolade platform, plus the way it has improved visibility despite still largely selling licences.

This was topped off with a strong third quarter to 30 September that ‘normally involves a pause for breath before a busy fourth quarter, a trend which has been bucked this year with two material contracts booked during the final days of the quarter,’ explain analysts at stockbroker FinnCap.

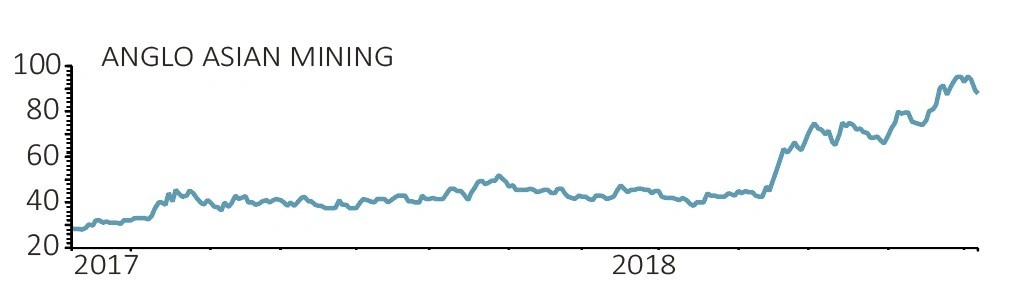

ANGLO ASIAN MINING +186%

Azerbaijan-based Anglo Asian Mining (AAZ:AIM) saw its share price perk up in September when it reported drill results indicating its Gedabek project contained a lot more gold and copper, thereby extending its mine life.

It then treated shareholders with news of a maiden dividend, having moved into a net cash position earlier in the year.

The shares kept on rising as more effort was made by the company into studying the wider Gedabek area, plus the head of geology buying shares which sent a vote of confidence in the business.

Analysts expect the company’s gold and copper production to grow in 2019 and they note all-in costs are among the lowest in the mining sector.

MARKET CAP: LESS THAN £100M

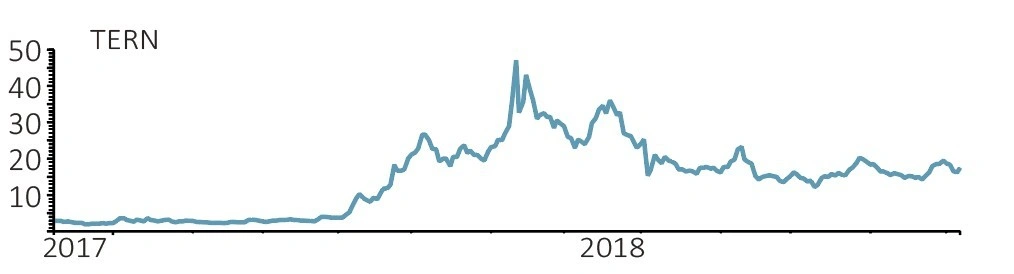

TERN +633%

Tern (TERN:AIM) is little-known technology investment firm whose focus on connectivity-related internet of things (IoT) really started to pay off in 2018.

The balance sheet has been cleaned up of convertible loan notes while fresh growth funding was successfully raised, but the real kicker for the stock was success for Device Authority, a specialist in secure IoT authentication in which Tern owns a 56.8% stake.

Strategic alliances with Intel, Dell, Amazon Web Services and others have put the promise of rapid growth on the horizon, while those sort of industry names do wonders in validating Device Authority’s password management tool KeyScaler.

ROCKROSE ENERGY +386%

Rockrose Energy (RRE) has enjoyed something of a break-out year in 2018. It is a buy-and-build effort in the oil and gas sector which floated in 2016 with a plan to capitalise on the oil price crash.

The company has been generating significant amounts of cash flow from its acquired portfolio of assets in the UK and the Netherlands. It was even in a position to launch a £16.4m tender offer to clear out any potential sellers of the stock.

Rockrose enjoyed significant advances in May when it announced the acquisition of Dutch assets which effectively doubled its output. October saw the Arran project in the North Sea, acquired from Korean-owned Dana Petroleum in August, green-lit for development by operator Royal Dutch Shell (RDSB).

By Daniel Coatsworth, Tom Sieber, Steven Frazer, Ian Conway, Lisa-Marie Janes

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.