Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHot investment topics for 2019

Investor sentiment is fragile amid a very difficult period for stock markets around the world. The FTSE 100 has hit a two-year low and numerous market experts say we are at a major turning point

for investments.

Against this backdrop it is no wonder that investors have so many questions about what’s going on, and what could happen next.

We’ve distilled all the key issues into this article and attempted to make sense of the current state of affairs, as well as drawing upon the expertise of analysts and strategists from across the investment community for guidance.

The best advice we can give is not to panic. Long-term investors should take advantage of market weakness to buy high quality companies or funds run by best-in-class managers.

Investing on a monthly basis means you buy more shares or fund units when markets are down, and less when they are up. It’s this

steady drip-feeding which ensures you a) continue with a saving habit and do not attempt the devilishly tricky task of timing the market and b) effectively pay the average price over a longer period

which can help smooth out market volatility.

WHAT ARE THE EXPERTS SAYING?

Bank of America Merrill Lynch, an investment bank, predicts

the long bull market for stocks and bonds will finally wind

down in 2019 ‘but not before one last hurrah’.

Asset manager Unigestion believes expected returns from stocks and risky assets overall will remain positive, though at lower levels.

UBS, also an investment bank, says slower US growth is ‘unlikely to bring equities down, but likely to drive volatility up’. It says history suggests equity returns can remain strong even if corporate earnings growth slows.

‘For 2019 we expect solid but decelerating global earnings growth and potential challenges from higher oil prices, rising benchmark yields and a weaker dollar. Altogether, that implies single-digit returns for the MSCI All Country World Index,’ adds UBS. This index includes large and mid-cap stocks across 23 developed markets and 24 emerging markets countries.

YIELD CURVES, INTEREST RATES AND RECESSION FEARS

Investors need to watch events in the US very closely as this country has a major influence on markets in other parts of the world. There is a phrase that says ‘when America sneezes, the world catches a cold’.

The big story going into 2019 is whether the US economy has reached its peak and could be headed into recession over the next few years. Market experts are watching the US yield curve very closely, namely the difference between short and long-dated yields on US government bonds (also known as Treasuries).

Theoretically investors want a higher yield for longer-dated bonds because there is a risk for holding something for longer. Therefore the yield curve should ordinarily show an upwards pattern if

you were looking at a single graph covering the different maturities.

The difference between the 2-year and 10-year US government bond yields was more than 290 basis points in 2010. It fell below 10 basis points at the start of December this year, causing investors to ponder what this signals.

History suggests an inverted yield curve happens in the run-up to a recession. Inversion means when the yield curve ceases to be upward sloping and shorter-dated yields are higher than longer-dated ones. This has now happened, with yields on five-year bonds (2.74%) dropping below the two-year ones (2.754%).

Analysis by Deutsche Bank suggests the average time lag between the yield curve inverting and an economy falling into recession is nearly two years (21 months). Investors must remember that the stock market is forward-looking, and 21 months is too close for investors to ignore.

WHAT COULD HAPPEN TO INTEREST RATES?

The US economy grew at an annualised rate of 3.5% in the most recent quarter and the Federal Reserve has raised interest rates eight times since 2015, currently standing at a range of 2% to 2.25%. Arguably the central bank needs to have much higher rates to provide a cushion should the economy start to decline, requiring rates to be cut.

Fed Reserve chairman Jerome Powell last month hinted at fewer interest rate rises which went down well with investors, temporarily acting as support for the stock market. The general consensus at present is for three quarter point rate hikes in 2019.

Investment bank Morgan Stanley believes US economic growth will decelerate sharply in 2019 with the third quarter potentially showing just 1% annualised growth.

WHAT COULD HAPPEN TO THE US DOLLAR?

Bank of America Merrill Lynch believes the US dollar will weaken in the coming year which is good for emerging markets and for commodity producers, in particular.

In fact, the bank’s top sector pick for 2019 is metals and mining where it says the industry has attractive equity valuations and a greater emphasis on dividends and share buybacks. A weaker

dollar makes it cheaper for foreign companies to buy dollar-denominated commodities.

WHAT COULD HAPPEN TO US GOVERNMENT BONDS?

The investment bank forecasts rising US government bond yields next year with the 10-year bond rising to 3.25% by the end of the year. At the time of writing they stood at 2.877%.

Higher bond yields are bad for equities because they tend to depress the multiple investors are willing to prescribe to earnings. In essence, companies which used to trade on high price-to-earnings (PE) ratios may de-rate, if they haven’t already done so, to trade on much lower PEs.

Second, higher bond yields put pressure on companies with stretched balance sheets. We suggest investors be very wary of highly--‑indebted businesses, particularly if interest rates are expected to keep going up.

The cost of debt will be higher to service which would put pressure on profit margins. The market may be more averse to businesses with large borrowings, potentially resulting in widespread share price declines for debt-heavy stocks.

WHERE NEXT WITH BREXIT AND HOW WILL MARKETS REACT?

We write in the immediate fall-out of Theresa May delaying the parliamentary Brexit vote. Sterling and the UK-focused FTSE 250 index both took a hit amid renewed uncertainty over how Brexit will play out.

WHAT COULD HAPPEN IN A NO-DEAL SCENARIO?

The situation likely to see the biggest devaluation in the pound is a disorderly no-deal Brexit which sees some flights grounded, provision of food and medicines put under threat and queues of trucks at Dover and Calais.

There would likely be degrees of disruption from a no-deal situation with the possibility of a so-called ‘negotiated no-deal’ to prevent such issues.

Both the Treasury and the Bank of England would probably look to shore up the economy with financial stimulus and the continuation of low interest rates or even a cut, although a spike in inflation from weaker sterling could make this problematic.

THERESA MAY TRIES AGAIN?

At the time of writing Theresa May faced a vote of no confidence from Tory MPs. The result hadn’t been released as this edition of Shares went to press.

Assuming no change at top, it is possible Theresa May will return to MPs for the Brexit vote very soon, perhaps having secured some sort of concession from the EU (although most expect this to be cosmetic

at best).

Her hope would be that the prospect of a no-deal Brexit is sufficiently scary to bring parliament in line. If she is successful you should expect a big recovery in UK-focused assets.

IS THERE A PLAN B (OR C)?

This could take several different forms. Either a parliamentary consensus forms around an alternative such as ‘Norway-plus’

which effectively means staying in the customs union and the single market. Assuming the EU was amenable this would likely boost UK assets.

Alternatively, a new government is formed, Brexit is delayed, and a fresh set of negotiations take place, or a second referendum is called with ‘Remain’ on the ballot paper.

These situations would likely lead to renewed pressure on domestic stocks and sterling as uncertainty is prolonged, with the possibility of a big recovery if a softer Brexit or even no Brexit emerged as the outcome.

Crucially, a European ruling on 10 December suggested the mechanism through which the UK is exiting the EU (Article 50) can be unilaterally revoked.

VALUE INVESTING TO COME BACK INTO FASHION?

Growth companies have been the best performers for numerous years on the market with value investing very much out of favour. There are suggestions that this situation could now change.

Analysts at Morgan Stanley say they have a strong preference for value over growth ‘as we think that we are only at the start of a long-term style trend reversal’.

Geir Lode, head of global equities at asset manager Hermes, adds: ‘After a long period of low real interest rates resulting in growth outperforming value stocks we believe value is inexpensive versus growth.

‘For example, we are seeing attractive investment opportunities in the oil services sector and US regional banks. In Japan we are also finding stocks with strong fundamentals at attractive prices.’

WILL TRADE WARS ESCALATE IN 2019?

UK investors may find it difficult not to view everything through the prism of Brexit yet trade tensions between the US and China have the scope to exert significant influence on financial markets around the world, including the UK.

This was beautifully illustrated when a short-term truce was struck between Donald Trump and China’s President Xi Jinping during talks in Argentina at the recent G20 summit. That sparked a widespread rally in global equities, only for financial markets to fall sharply again as economic growth, inflation and recession fears came back to haunt investors, plus Trump reminding the world that he is ‘Tariff Man’. The furore over the arrest of Huawei executive Meng Wanzhou in a spying row hiked the pressure further.

So far the US has slapped tariffs on $250bn worth of Chinese imports with the threat of more to come if the current truce fails to hold, while China has responded in kind with $160bn of its own taxes on US products.

These are trade tensions that extend far beyond the simple cross-border exchange of goods and services. ‘It is primarily a national security dispute where the key ingredients are technology leadership; laws, regulations, and behaviours; an overarching accusation of state interference; and ideological differences,’ says Jay Roberts of RBC Wealth Management.

Accusations of intellectual property theft by Chinese agencies remains one of the US’s chief bugbears.

Ramping up hostilities in 2019 would undoubtedly have significant ramifications for economic growth in a year when inflation and interest rate pressures are already building.

The re-emergence of a strain between the US and European Union would add to financial market risk.

The hope is that diplomacy, and common sense, will prevail on all sides during 2019 but as we have seen with his frequent loose cannon Twitter tirades, President Trump remains an unpredictable powder keg for financial markets.

WHERE NEXT FOR THE US STOCK MARKET?

To quote the chairman of the US Federal Reserve, 2018 has been an ‘extraordinary time’ for the US economy.

The combination of a boost to corporate profits from Trump’s tax cuts, steady growth in consumer spending and an almost 50-year low in unemployment means that economic growth will surpass 3%

this year.

Even with interest rates rising and more increases to come growth should remain healthy into the middle of 2019 before slowing.

The US stock market has had a much bumpier ride with the S&P 500 index twice making all-time highs this year only to suffer sudden reversals, the most recent of which wiped over 10% off stock prices leaving the index flat for the year.

Looking ahead, although tax rates will remain favourable, companies won’t see a repeat of the ‘bump’ in profits which they enjoyed this year.

According to data provider FactSet, aggregate earnings per share for the S&P 500 index have grown by 25% each quarter so far this year with every sector showing an increase. The outlook for 2019 is a much more measured 8% increase.

Meanwhile the tightness of the labour market is slowly pushing up wage costs and while the trade war with China hasn’t yet had a notable effect on US companies if it escalates it could begin to impact sales and profits.

The combination of higher interest rates and slower earnings growth isn’t great for the stock market and investors are going to have to be more selective if they want to make money next year.

Mike Thompson, who as managing director of S&P Investment Advisory Services oversees and advises on the allocation of over $37bn of assets, remains bullish on the US over Europe and emerging markets but cautions that investors need to look beyond the so-called FAANG stocks.

‘People have bought stocks like Facebook, Apple and Netflix because they engage with them on a personal level and because the media is constantly hyping them,’ says Thompson.

‘There’s now a huge “goodwill premium” between the book value of these businesses and their market value,’ he adds.

PREDICTIONS FOR THE S&P 500

S&P Investment Advisory Services forecasts that the S&P 500 index will hit 3,100 points by the end of July 2019, 13% above its current level.

In contrast analysts are erring on the side of caution with strategists at investment bank Goldman Sachs seeing a 1-in-2 chance that stocks will gain 5% next year and a 1-in-3 chance that they will lose 7%.

Goldman is advising clients to sell some of their stocks and increase their allocations to cash. With interest rates rising, short-term dollar deposits and Treasury bills now look more attractive than they have done for many years.

WHAT IS THE ECONOMIC OUTLOOK FOR KEY GLOBAL REGIONS?

The global economy is likely to slow back to trend in 2019 after two years of above-trend growth, according to Bank of America Merrill Lynch.

It says the divergence between the Federal Reserve and other major central banks is likely to surprise markets. ‘Risks are skewed to the

downside’, argues the bank. ‘The US-China trade war, Brexit and “Quitaly” loom large with a wide range of possible outcomes.’ Quitaly is the fear that Italy might withdraw from the eurozone.

US – America’s economy is going gangbusters, no doubt boosted by President Trump’s late 2017 tax cuts, although whether

the globe’s biggest economy can keep growing so rapidly when its trading partners are not remains to be seen.

Trade could become an even more acute issue in 2019 as the White House steps up the pressure on China, Canada, Mexico and the EU.

Bank of America Merrill Lynch’s 2019 GDP growth forecast of 2.7% appears strong, although it masks a predicted second half slowdown.

Invesco’s chief economist John Greenwood argues that despite low unemployment and Trump’s fiscal stimulus, the course of the US economy will remain broadly consistent with the Fed’s mandate to

achieve full employment with 2% inflation.

‘This, in turn, should limit the upside risk for interest rates and inflation. By the same token, it should limit the downside risk for the stock market and the bond market,’ he explains.

Greenwood points out tariffs are potentially damaging to trade volumes and will raise the cost of imports for US businesses and consumers. ‘But the important thing to remember is that if domestic spending on consumption and investment is maintained, the damage from these trade measures should be minor.’

JAPAN – Japan continues to experience sub-par growth and below-target inflation. Next year sees it welcome both a G20 summit and the Rugby World Cup, but investors will be watching the Shinzo Abe government and the Bank of Japan to see if they can boost growth on a sustainable basis and prove the country’s punchy public-debt-to-GDP ratio is manageable.

Despite five years of aggressive quantitative and qualitative easing, scant progress has been made in restoring growth and inflation to normality, with Japan hamstrung by an ageing population.

CHINA & SMALLER EAST ASIAN ECONOMIES – A trade war and deleveraging are taking their toll on China, which is confronting the challenge of deleveraging while attempting to maintain growth by intermittent easing of monetary policy.

Real GDP has slowed and is likely to slow further in 2019 as tariffs impact export growth. Next year, Invesco’s Greenwood expects only single-digit growth of exports in US dollar terms.

Elsewhere in East Asia, domestic spending has been subdued while export growth has slowed. In 2019, smaller, low-cost economies such as Thailand and Vietnam may benefit from some re-allocation of Chinese manufacturing, but the overall outlook will be subject to trade tensions.

EUROPE – America’s tough stance on tariffs and trade, Brexit and Italy’s fractious new coalition government were all pressure points for Western Europe in 2018, and are likely to have a huge influence in 2019.

Facing the demographic challenge of a receding working age population in most EU member states, unemployment remains higher than ideal at 8.2% across the eurozone, albeit this is the best figure since the summer of 2008.

AFRICA & THE MIDDLE EAST – Population growth, strong demographic trends driving private consumption and increased urbanisation are potential catalysts for positive economic progress, although 2018 proved a damp squib amid the region’s political and economic challenges.

In the New Year, a weaker dollar and stronger commodity prices could help sentiment, while the economic outlook could be affected by elections in Nigeria, South Africa and also Israel.

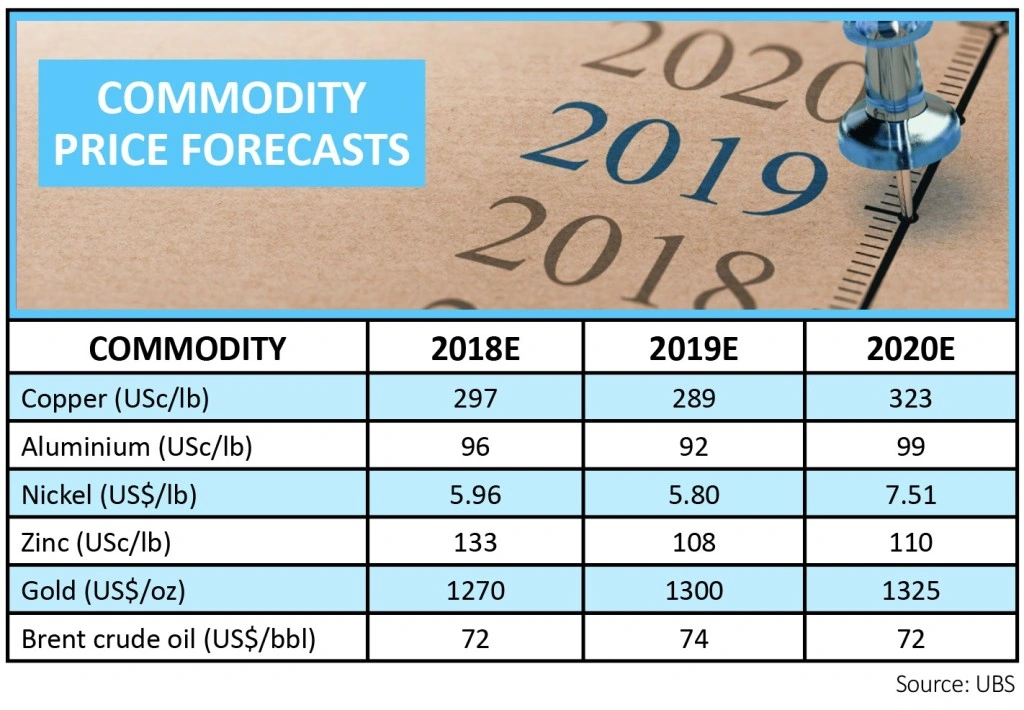

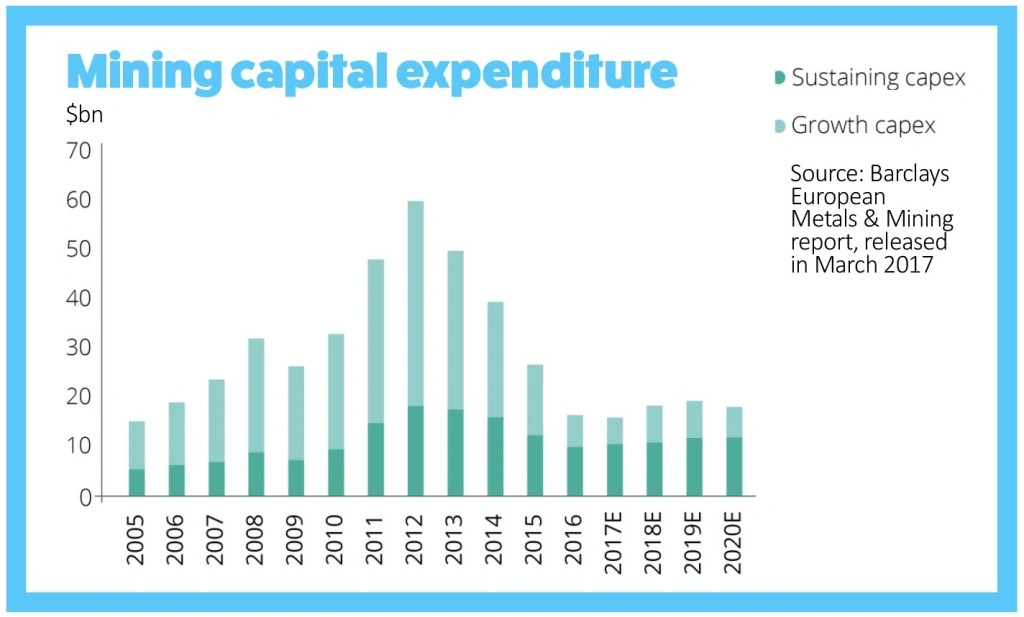

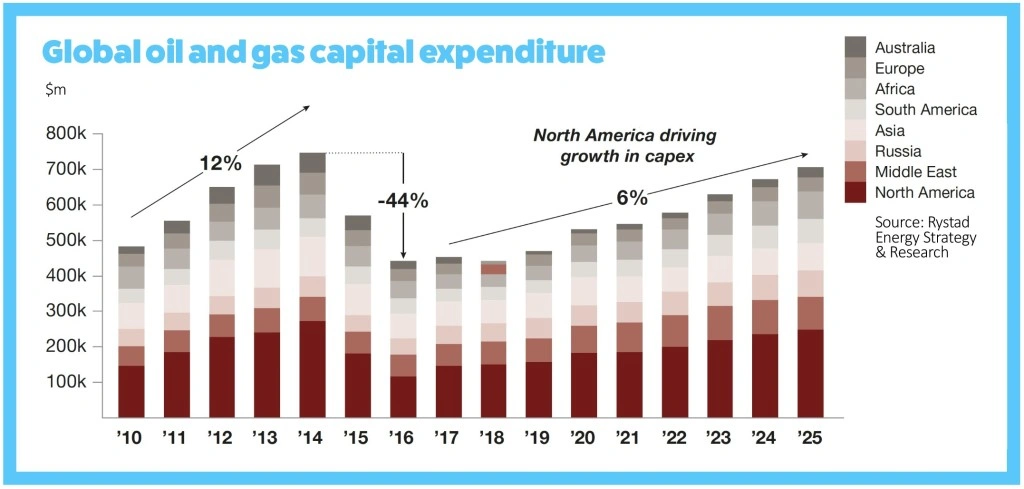

WHAT ARE THE IMPLICATIONS OF UNDERINVESTMENT IN THE RESOURCES SECTOR?

The commodities crash which took place four-to-five years ago forced a rethink in the mining, oil and gas industries as companies were faced with dwindling cash flow.

On the mining side some of the pain was endured directly by shareholders as dividends were cut and capital losses were incurred.

However, for the most part and particularly in the oil and gas space, capital spending took the brunt of firms’ straitened financial circumstances.

If companies are not spending cash on developing new assets then output will eventually fall. Next year could be when this impact becomes apparent given the multi-year timelines associated with bringing a new mine or oil field into production.

And if output falls faster than demand then prices will go up, leading to increased energy and raw material costs for the corporate world and, among other things, a higher price at the pump for consumers.

BAD TIMING FOR BUDGET SETTING

The longer-term picture could also be affected by the recent renewed correction in commodities markets with management teams currently in the process of finalising budgets for the coming 12 months.

It will therefore be worth watching first quarter updates from the likes of BHP (BHP), BP (BP.) and Royal Dutch Shell (RDSB) for guidance on capital expenditure.

On oil, Canadian investment bank BMO says: ‘The drop in crude oil prices comes as oil companies are setting capital budgets for 2019. This could translate to lower spending assuming that most companies will incorporate a conservative oil price outlook of roughly $50 per barrel into their capital spending plans. More worrisome, this could exacerbate the possible supply shortfall after 2020.’

On mining, in a report published earlier this year Deloitte noted: ‘Still burdened with high debt loads and rising price-to-earnings (PE) multiples, mining companies are struggling to free up the exploration and development budgets required to exploit new resources. At the same time, they remain extremely hesitant to engage in acquisitions to feed the exploration pipeline.’

MAJOR POLITICAL DEVELOPMENTS IN 2019

South Africa recently emerged from its recession but faces high unemployment and low investment. The country also struggled with corruption in the upper ranks under Jacob Zuma.

Successor Cyril Ramaphosa wants to get rid of corruption and is targeting $100bn in investment, although he will have to face off against the Democratic Alliance and Economic Freedom Fighters in the 2019 election to maintain power. The election could happen in May.

India has a general election in April/May where Prime Minister Narendra Modi hopes to stay in power. The election may be a tough battleground as Modi has already been forced to fight off a no-confidence motion.

There have been protests from farmers amid a backtrack on planned reforms and concerns about increasing inequality.

Back in 2014, Modi’s party was able to form a government despite gaining 31% of overall votes, the lowest figure for a party in power since 1947.

Since the UK voted to leave the EU there have been questions over whether others will follow. The outcome of Greece’s general election, which will be held by 20 October, will shed light on whether the public are satisfied with its leadership and the EU.

Greece was hit hard by the 2008 financial crash, resulting in a bailout to the tune of nearly €300bn and drastic austerity measures.

PICTET'S PREDICTIONS FOR 2019:

–Slowing economic growth and a squeeze on corporate profit margins would be bad for equities.

–Growing wages are feeding through to inflation which is bad for bonds. Investment and speculative-grade credit look vulnerable to a correction.

–A weaker US economy could be good for long-dated and index-linked US Treasuries and gold

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.