Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineAre UK stocks a value trap or a screaming buy?

December’s failure (so far) to deliver a Santa rally means the FTSE 100 is trading at a two-year low and now also stands below the 6,930 level at which it peaked on 31 December 1999, just before the technology, media and telecoms bubble burst.

This means investors are now left to decide whether this is a chance to buy on what is now becoming a big dip in the UK’s premier index, which topped out for the year, on a closing basis, at 7,877 on 22 May.

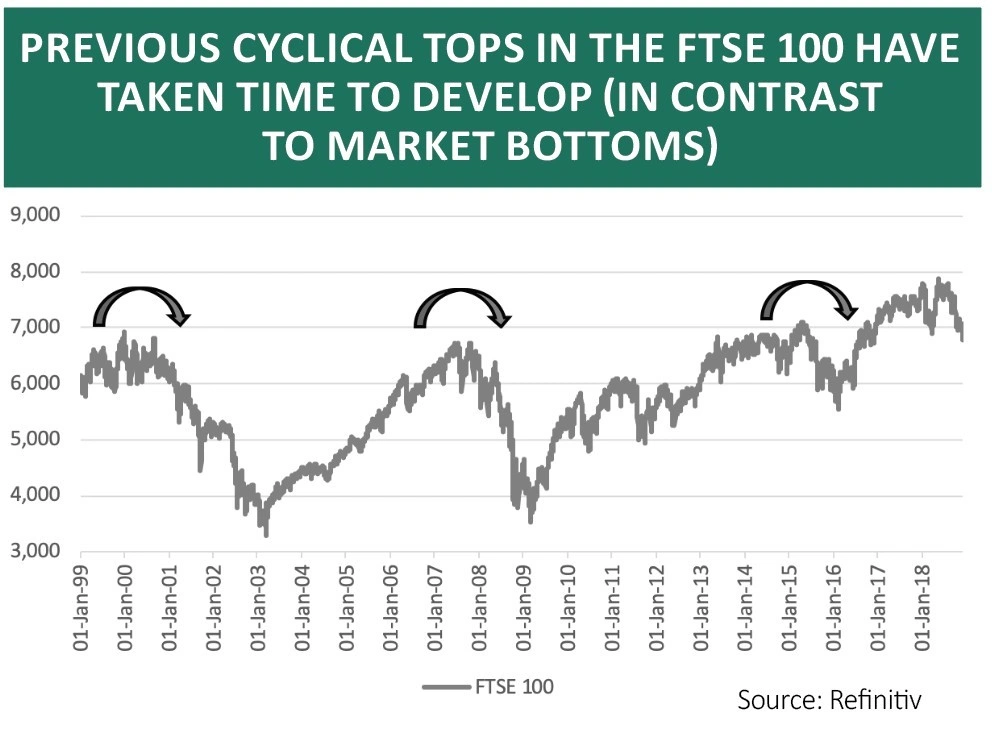

TOPS AND BOTTOMS

Technical analysts, who look for signals from charts and market price action, may well be sceptical, especially if they are adherents to the old saying that ‘market tops are a process, while market bottoms are an event’.

This can be seen from the FTSE 100 chart going back to the start of 1999.

The three tops that are clearly visible, in 1999, 2007 and 2015, were all preceded by a series of minor peaks, with each upward move less convincing before the last, as dip-buyers were lured to what proved to be their doom.

Chartists may see worrying echoes of that pattern now. By contrast, the second half of the adage rests upon how the bottoms of 2003, 2009 and 2016 were sudden as the FTSE 100 moved into recovery mode very quickly.

PRICES AND PESSIMISM

Investors who prefer to focus on fundamentals such as profit, cash flow, dividend yield and valuation may take a different view, especially if they have a long-term time horizon and are able (and willing) to sit out what could prove to be further Brexit-related volatility in UK equities.

They may argue that UK stocks are cheap, because of the gloom which currently surrounds the Brexit process, Sino-US trade relations and the prospect of yet more interest rate increases in the US.

As master investor Warren Buffett once put it: ‘The most common cause of low prices is pessimism – sometimes pervasive, sometimes specific to a company or industry. We want to do business in such an environment, not because we like pessimism but because we like the prices it produces. It is optimism that is the enemy of the rational investor.’

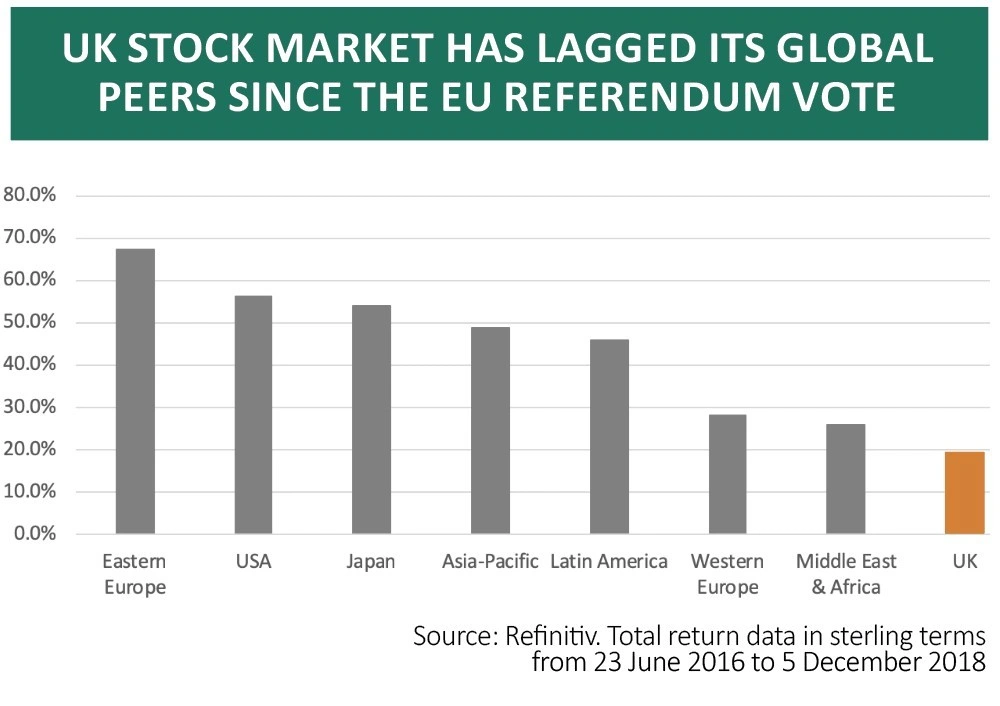

There does not look to be too much optimism surrounding the UK economy at the moment, or its stock market, which has been the worst performer (in sterling, total-return terms) among the eight major geographic options available to investors since 23 June 2016, when the British electorate voted to leave the European Union.

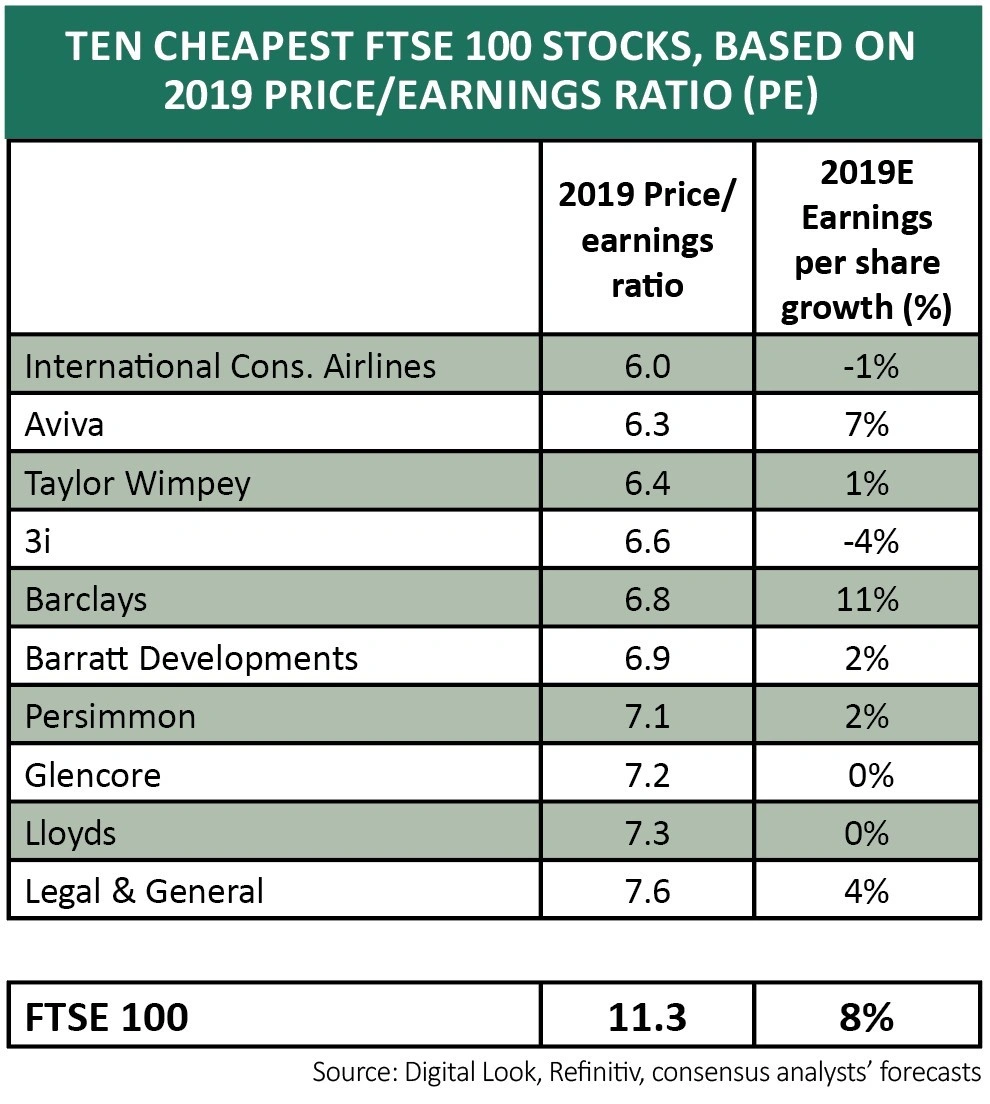

That begs the question of whether value is emerging from the UK stock market – and some investors may be tempted to think so. Thirty one FTSE 100 firms are trading on a forward price-to-earnings ratio for 2019 of less than 10-times, and 38 of the index’s members offer a dividend yield of more than 5% for next year, according to analysts’ consensus forecasts.

That leaves two issues for value-seeking investors to address, whether they are selecting their own stocks or paying a fund manager to do the donkey work for them.

The first is whether analysts’ forecasts are reliable. Estimates of 8% growth in earnings and 4% in dividends across the whole of the FTSE 100 might not sound like much, but if the UK economy slips into an unexpected recession, and is joined there by say the US, then such figures are likely to prove wildly optimistic.

Equally, the numbers could prove to be too low if the British and global economies prove more resilient than the current consensus amongst analysts and economists would have us believe.

The second is what could be the catalyst to persuade money, be it from domestic or overseas sources, to revisit UK stocks once more. Even if they are unloved, have underperformed and could be undervalued, you could have said the same a year ago, to no particular effect, as it turned out.

Any visibility on what Brexit will look like and what it may mean could be one possible answer.

Once investors know what they are dealing with, whatever it may be, then they have a chance to rationally assess earnings and dividend forecasts and thus valuations.

Any would-be dip-buyers may have to be brave and patient – but then the darkest hour always comes before the dawn.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.